Shanghai Auto Show Leads Fast & Furious Rally

2 Min. Read Time

Key News

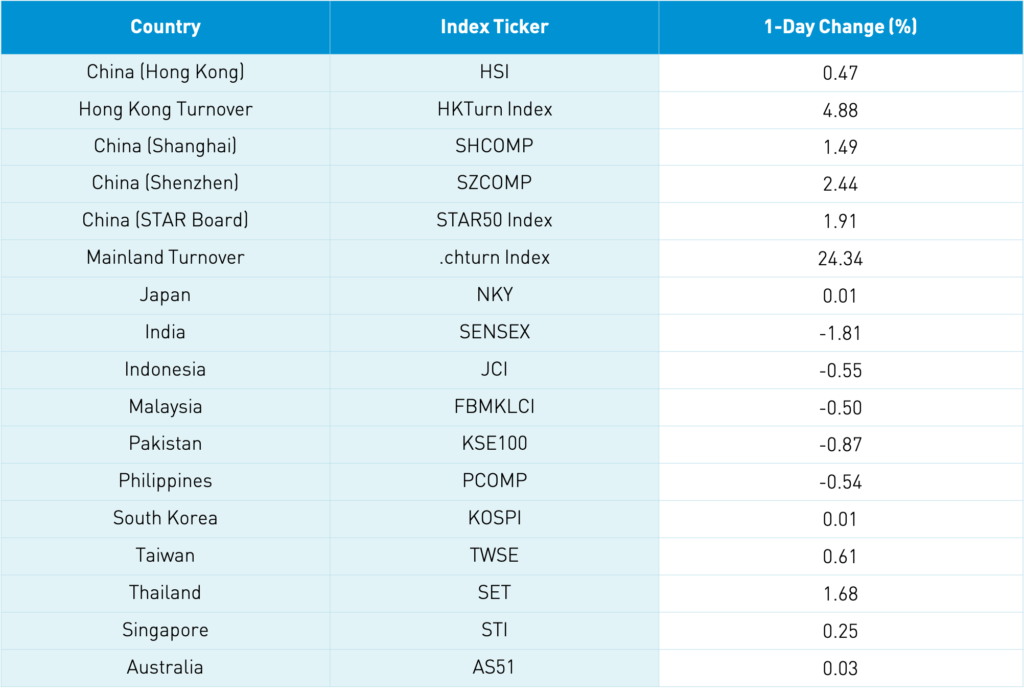

Asia had a mixed start to the week as China outperformed and India underperformed.

Reuters reported over the weekend that Jack Ma could sell his ownership in Ant Group. The article insinuated that if Jack Ma were to give up control of the company it would help remove regulatory scrutiny. The veracity of the article has been denied by the company but weighed on internet investor sentiment in Hong Kong.

The STAR Board announced it will not allow real estate and financial companies to list, which removes the feasibility of an Ant Group IPO on the exchange. This is not a big deal. However, considering Mainland investors’ enthusiasm for the company, the announcement could weigh on Ant’s valuation.

After the close, Meituan announced the sale of 187 million shares to institutional investors at a discount to the current price, selling $400 million of stock to Tencent and $3 billion in convertible notes, which should raise a total of approximately $10 billion. Based on the weakness of Meituan during Hong Kong trading overnight, there may have been some information leakage. However, Tencent’s investment is a strong endorsement.

Helping Mainland sentiment was both the start of the Shanghai Auto Show, which led to the strong performance of autos, electric vehicles, and battery-related stocks and positive words from regulators on distressed manager Huarong Asset Management. It is amazing to see how little media coverage John Kerry’s visit to Shanghai received as I believe a US-China climate deal could be in the works. Apparently, if it isn’t negative, it isn’t fit to print. Also receiving no media attention is the annual meeting of twenty-nine Asian countries at the Boao Forum For Asia in Boao, Hainan.

The Loan Prime Rates will be released tomorrow and most expect them to be unchanged.

H-Share Update

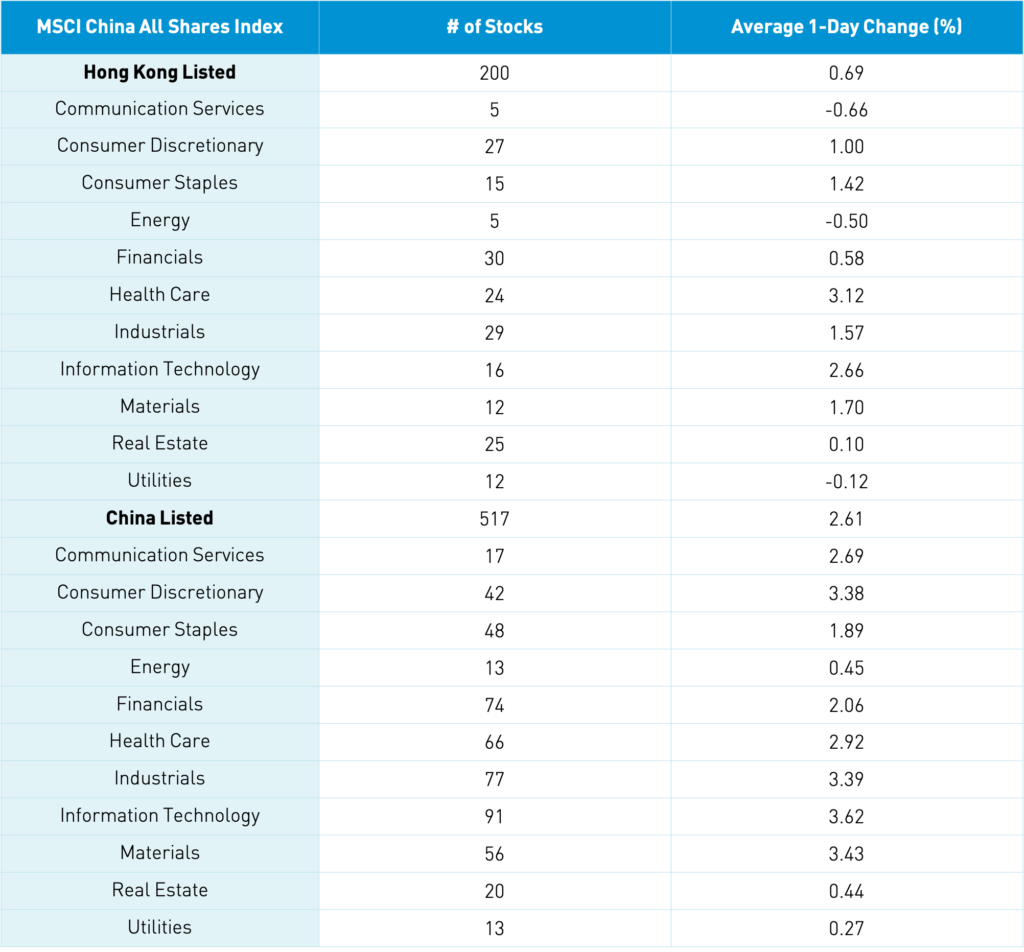

The Hang Seng opened lower but quickly rebounded to close +0.47% with volume +4.92% from Friday, which is only 95% of the 1-year average. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.71% led by healthcare +3.13%, tech +2.67%, materials +1.71%, industrials +1.59%, and staples +1.43%. Meanwhile, communication -0.65%, energy -0.49% and utilities -0.1%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.79%, Meituan, which fell -0.34%, Alibaba HK, which fell -1.53%, Xiaomi, which gained +2.11%, HK Exchanges, which gained +2.7%, Geely Auto, which gained +4.82%, BYD, which gained +4.77%, China Mobile, which gained +1.76%, Sunny Optical, which gained +5.19%, and JD.com HK, which fell -0.53%. Trip.com listed in Hong Kong today and gained +4.55%. Southbound Stock Connect volumes were up from last week though still light as Mainland investors bought $658 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 13.6% of Hong Kong turnover. Tencent saw significant inflows today.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +1.49%, +2.44%, and +1.91%, respectively, as volume surged +24% from Friday to 98% of the 1-year average. Breadth was positive with 2,803 advancers and 993 decliners. The Mainland stocks within the MSCI China All Shares Index gained +2.54% led by tech +3.54%, materials +3.35%, industrials +3.31%, discretionary +3.3% healthcare +2.84%, communication +2.62%, and financials +1.98% as all sectors were in the green. Auto, electric vehicles, and auto-related names outperformed today along with tourism-related stocks in advance of the May Labor Day holiday in China. The Mainland’s most heavily traded stocks by value traded were BYD, which gained +6.5%, broker East Money, which gained +5.43%, BOE Tech, which gained +1.44%, CATL, which gained +9.03%, and Luxshare Precision, which gained +9.86%. Foreign investors bought $2.506 billion worth of Mainland stocks today as Northbound Stock Connect accounted for 7.5% of Mainland turnover. CNY appreciated versus the US dollar, bonds gained, and copper was off a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.52 versus 6.52 yesterday

- CNY/EUR 7.82 versus 7.82 yesterday

- Yield on 1-Day Government Bond 1.72% versus 1.58% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.17% yesterday

- Yield on 10-Year China Development Bank Bond 3.57% versus 3.57% yesterday

- China’s Copper Price -0.15%