Mainland Markets Shrug Off Global Inflation Fears

4 Min. Read Time

Upcoming Event

Join us on Tuesday, May 25th at 8:20 am for our virtual mid-year conference:

Innovation: The Next Phase of China’s Secular Growth

Featuring the CFO of NIO Steven Feng, CFO of Lufax James Zheng, and Former US Ambassador to China Max Baucus.

Click here to register.

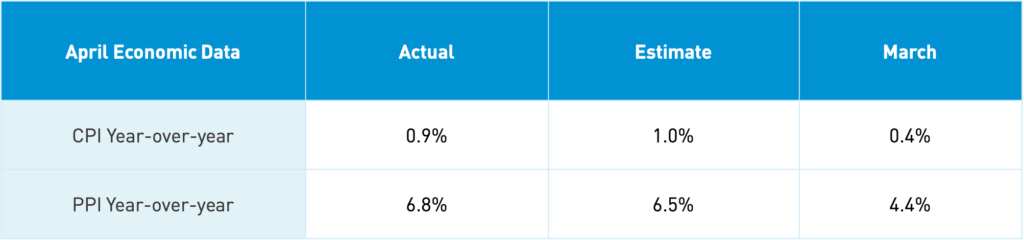

Takeaway: The release at the market’s open was not a significant factor as China’s bond market was unchanged. However, the higher PPI numbers, driven by rising commodity prices, added to higher global inflation concerns. The demand for commodities as global economies come back online is outstripping supply raising prices. Mining, raw materials, and manufacturing producer goods saw prices rise +24.9%, +15.2%, and +5.4% respectively year-over-year. The muted manufacturing price move indicates that higher commodity prices are being passed along to end buyers. The numbers are a simple reflection of higher prices, which are apt to cool in the future, likely because we have suddenly become more aware of the issue. CPI declined -0.3% month-over-month as food prices (i.e pork prices) fell -0.7% year-over-year while transportation prices rose +4.9% year-over-year, indicating more domestic travel. Not all bad!

Key News

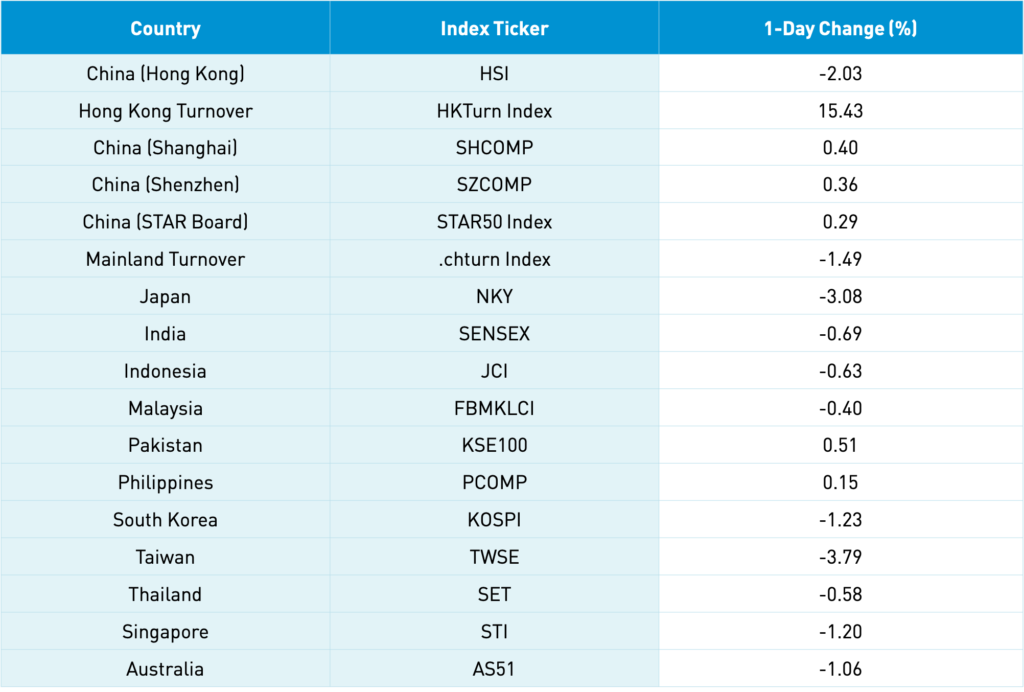

Asian equities were off though Mainland China was an oasis of diversification, rising today while Japan and Taiwan were off more than -3% as yesterday’s US tech wreck went global on rising inflation fears. Not helping the US markets this morning are legendary investor Stanley Druckenmiller’s WSJ editorial and Former NY Federal Reserve Bank President Bill Dudley’s Bloomberg Editorial on the specter of higher US interest rates.

Hong Kong-listed technology stocks were off on regulatory concerns as Meituan and Pinduoduo met with Shanghai officials to discuss the wages of their delivery drivers. There is no greater example than Weibo’s strong earnings release yesterday, which promptly saw the stock fall -8% intraday though it managed to rebound closing at +1.59%. Did regulation hurt Weibo? Nothing in their earnings showed that it did.

China’s census was released after the market close, showing that China’s population increased by only 70 million since 2010 to 1.41 billion. Policymakers worry over the recent drop in births over the last several years along with the average number of babies per female, 1.3. In addition, 18.7% of the population are over the age of 60 versus 17.95% below the age of 14. The culprit is urbanization. 63.89% of China’s population now lives in cities. Living in cities is expensive while most apartments don’t accommodate families easily. In my opinion, the solution should be more family-friendly apartment buildings.

Healthcare was an outperformer in both Hong Kong and China on the news that the elderly need more medical attention.

Multiple Chinese commodities futures exchanges implemented higher margin levels in an attempt to cool high prices, which led to profit-taking in commodity-related equity plays in Hong Kong and Mainland China. After the close, April auto sales were announced to have gained +12.4% year over year.

Today at 5 pm EST, MSCI will release its Pro-forma for its end-of-month Semi-Annual Index Review. One very significant event we flagged was the likelihood MSCI would announce that their indexes would use Alibaba’s Hong Kong listing going forward instead of the US listing. MSCI benchmarked ETFs, index funds, and active mutual funds would need to convert their existing BABA US shares to 9988 HK. This has nothing to do with the ongoing PCAOB issue with US-listed Chinese companies, but simply that the US listing is considered a foreign holding while the Hong Kong listing is considered a local listing.

After yesterday’s close, MSCI announced a one-day consultation with their clients for their opinion. There are pros/cons to the move. The US listing offers superior liquidity and is cheaper to trade in the US due to Hong Kong’s stamp tax of 10bps on buys and sells, which will be raised to 13 bps on August 1st. In the bigger picture, it could affect US exchanges, trading desks, and investment banks as more companies move to Hong Kong over the US.

US and Hong Kong-listed e-commerce and marketing firm Baozun released its first Environmental, Social, and Governance report, highlighting “the Company’s efforts and accomplishments in environmental sustainability, social responsibility, and corporate governance in 2020.” The 46-page report is a highly detailed report on the company’s extensive efforts. The report highlights the efforts by Chinese companies to meet global standards.

Alibaba and Bilibili will both report Q1 2021 results on Thursday morning before the US market opens.

H-Share Update

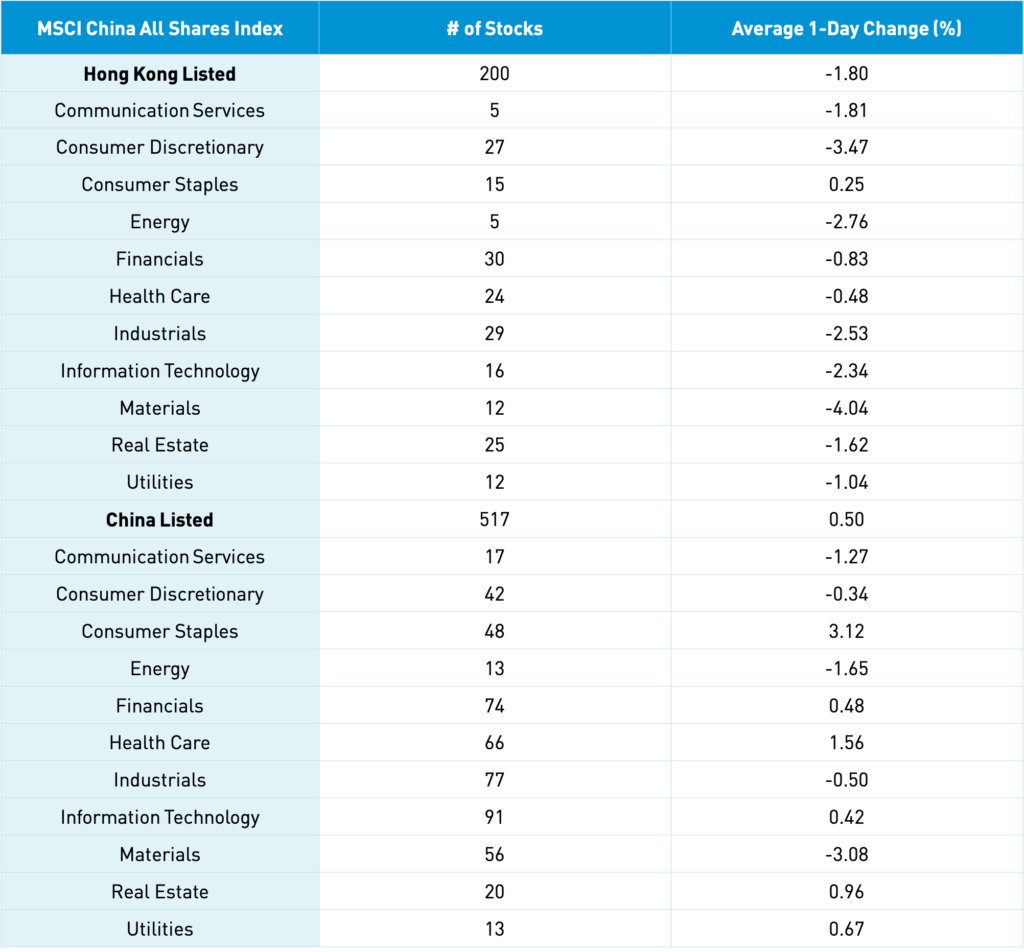

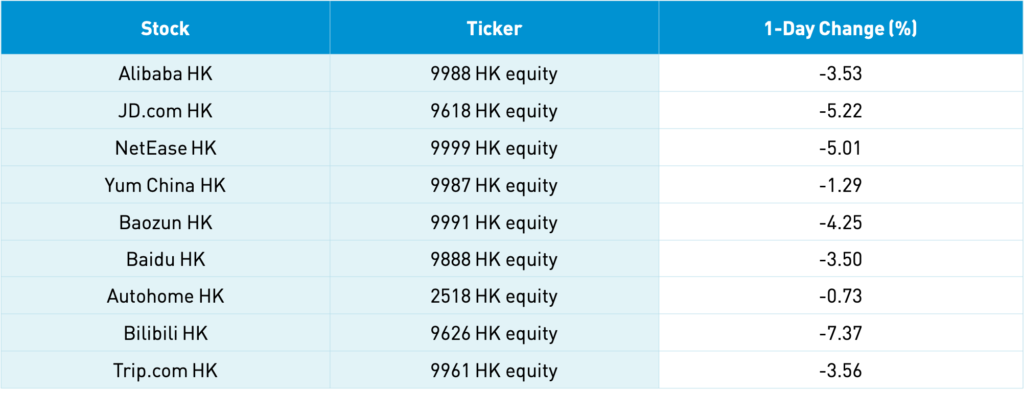

The Hang Seng Index went down in the first round and stayed down, closing -2.03% as volume increased 15%, which is 118% of the 1-year average. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index lost -1.8% as staples gained +0.25% while materials fell -4.04%, discretionary -3.47%, energy -2.76%, industrials -2.53%, tech -2.34%, and communication -1.82%. Hong Kong’s most heavily traded by value were Tencent, which fell -1.76%, Meituan, which fell -5.26%, Alibaba Hong Kong, which fell -3.53%, Xiaomi, which fell -2.38%, Ping An, which fell -0.18%, Hong Kong Exchanges, which fell -2.59%, JD.com Hong Kong, which fell -5.22%, AIA, which fell -3.14%, Kuaishou Tech, which fell -5.25%, SMIC, which fell -4.37%, and Zijin Mining, which fell -7.67%. Southbound Stock Connect volumes were moderate as Mainland investors bought $635mm led by buying in Xiaomi, Tencent, and Meituan. Southbound Connect trading accounted for 12.6% of Hong Kong turnover

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +0.4%, +0.36%, and +0.29% respectively while volume was off -1.49% from yesterday, which is 95% of the 1-year average. There were 1,306 advancing stocks and 1,546 declining stocks. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.5%, led by staples +3.03%, healthcare +1.48%, and real estate +0.87%, while materials -3.16%, energy -1.73%, and communication -1.35%. The Mainland’s most heavily traded by value were Fosun Pharma, which gained +5.02%, Kweichow Moutai, which gained +4.26%, Chongqing Changan Auto, which gained +6.09%, COSCO Shipping, which fell -8.9%, Zijin Mining, which fell -6.23%, Chongqing Sokon, which gained +0.21%, Wuliangye Yibin +4.34%, broker East Money, which gained +2.23% on earnings, Sany Heavy Industry, which fell -2.32%, and GEM, which fell -5.73%. Northbound Stock Connect volumes were moderate as foreign investors sold -$743mm of Mainland stocks as BOE Tech and CATL were sold while Wuliangye Yibin, Mindray, and Midea were bought as Northbound trading accounted for 6% of Mainland turnover. CNY was off a touch to 6.43, bonds were flat, and copper was off.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.43 versus 6.42 yesterday

- CNY/EUR 7.82 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.32% versus 1.27% yesterday

- Yield on 10-Year Government Bond 3.14% versus 3.15% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% Yesterday

- Copper Price -1.15% overnight