Meituan Reports Q1 Topline Growth at a Price, Week in Review

4 Min. Read Time

Week in Review

- Short video platform Kuaishou Technology reported Q1 results Monday. Revenues increased 36.6% year-over-year to RMB 17B from RMB 12.5B, which was in line with analyst expectations. However, the company’s expenses and cost of revenues both increased significantly, which drove losses.

- China’s currency appreciated to its three-year high against the US dollar this week as gains in the currency continued into Friday. The current exchange rate is 6.37 RMB per USD.

- E-Commerce company Pinduoduo (PDD US) announced Q1 2021 financial results before the US market open. Topline growth was amazing, growing more than 3X from a year ago. Although expenses increased, the company was able to cut its losses significantly.

- MSCI’s latest index rebalance took effect on Thursday, leading to high volumes in Mainland and Hong Kong markets. Major changes surrounding China included the replacement of Alibaba shares listed in the US with the company’s Hong Kong-listed shares across all MSCI indexes and the addition of China stocks listed in both Hong Kong and the Mainland.

Key News

Asian equities had a strong day on a quiet night though China was hit with profit-taking. There was some chatter about US-China political rhetoric as Congress looks to fund technology R&D. However, initial trade talks between the US and China yesterday appear to have gone well.

Following yesterday’s MSCI index rebalance, the largest EM ETFs no longer hold Alibaba’s US share class following an index-driven move the Hong Kong share class. It is remarkable how little is being written on this.

JD Logistics’ (2618 HK) IPO gained only +3.32% despite the retail allocation being oversubscribed by 700X.

Mainland China electric vehicle (EV) focused plays including battery, cobalt, copper, rare earth metals and lithium sub-sectors all had a strong day following chatter the US may provide an EV tax credit. Mainland-listed battery maker CATL was the most heavily traded stock in Hong Kong today, gaining +6.67%.

Yesterday, Gree Electric Appliances (000651 CH) announced a stock buyback worth RMB 7.5 billion to 15 billion, which is a rare event in China.

CNY rose slightly versus the US dollar overnight to 6.37 from yesterday’s 6.38 as Mainland financial media noted an opinion piece in the People’s Daily titled “Should the Renmibi Exchange Rate Appreciate?”. The opinion piece states that renminbi’s appreciation versus the US dollar is not an attempt to curtail commodity prices but only the result of market dynamics. Meituan was sold prior to releasing earnings after the market’s close.

Value sectors outperformed in Hong Kong growth names as internet and health care plays were off.

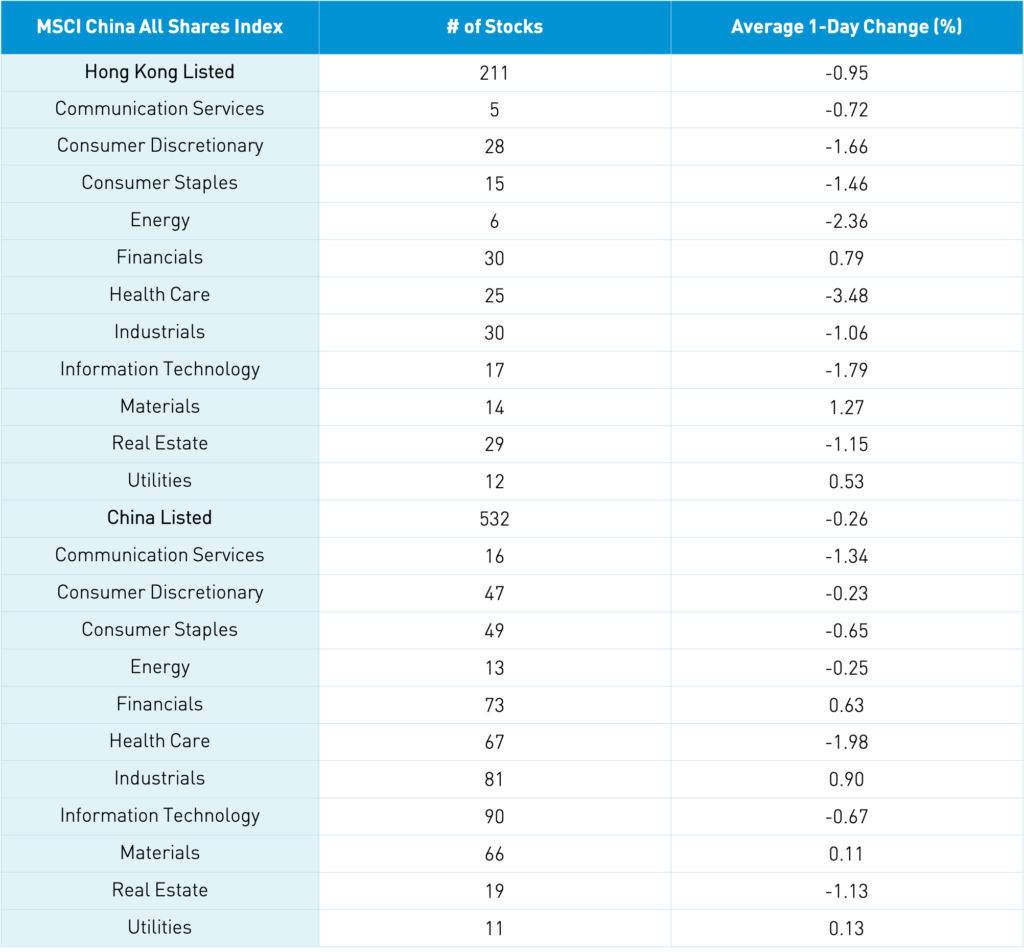

I like the MSCI China All Shares Index as it includes the full allocation of Chinese A shares (both Shanghai & Shenzhen stocks). After MSCI’s index rebalance, the number of Hong Kong stocks in the index increased from 200 to 211 and the number of Mainland stocks increased from 517 to 532.

I mentioned Beike (BEKE US) as a beneficiary of MSCI’s index rebalance yesterday. BEKE’s volume was 38mm shares/$1.952B versus Thursday’s 6.9mm/$358mm and a 1-year average of 4.4mm/$249mm. The power of passive was on full display!

Meituan announced Q1 2021 results after the Hong Kong close overnight and before the US market open. Similar to Bilibili and Pinduoduo, topline growth was simply outstanding, but the company’s losses expanded. Investors currently favor quality companies with revenue growth along with positive free cash flow and net income versus hyper revenue growth with no profit. Regardless of investors’ short-term attention deficit, Meituan had a heck of a quarter. Under “new initiatives” was a push into e-commerce via its “Food+Platform strategy”, Meituan Grocery, and “Instashopping” which is the “on-demand delivery of local goods and products”. The company noted “Roses, watches, and iPhones were all popular gifts sold” during the week leading up to Valentine’s Day.

- Revenues increased 120.9% to RMB 37.016B versus analyst expectations of RMB 35B and Q1 2020’s RMB 16.753B

- Revenues by segment: Food delivery +116% to RMB 20.575B, In-store/hotel/travel +112% to RMB 6.584B and New initiatives +136% to RMB 9.856B

- Transacting Users increased 26.9% to 569.3mm from Q1 2020’s 448.6mm

- Selling and marketing expenses nearly doubled to RMB 7.206B from Q1 2020’s RMB 3.199B

- Total operating loss increased +177.9% to RMB 4.767B from Q1 2020’s RMB 1.715B and analyst expectations of RMB -5.538B

- Adjusted EPS was

- Cash on the books increased slightly to RMB 17.792B from Q4 2020’s RMB 17.093B

H-Share Update

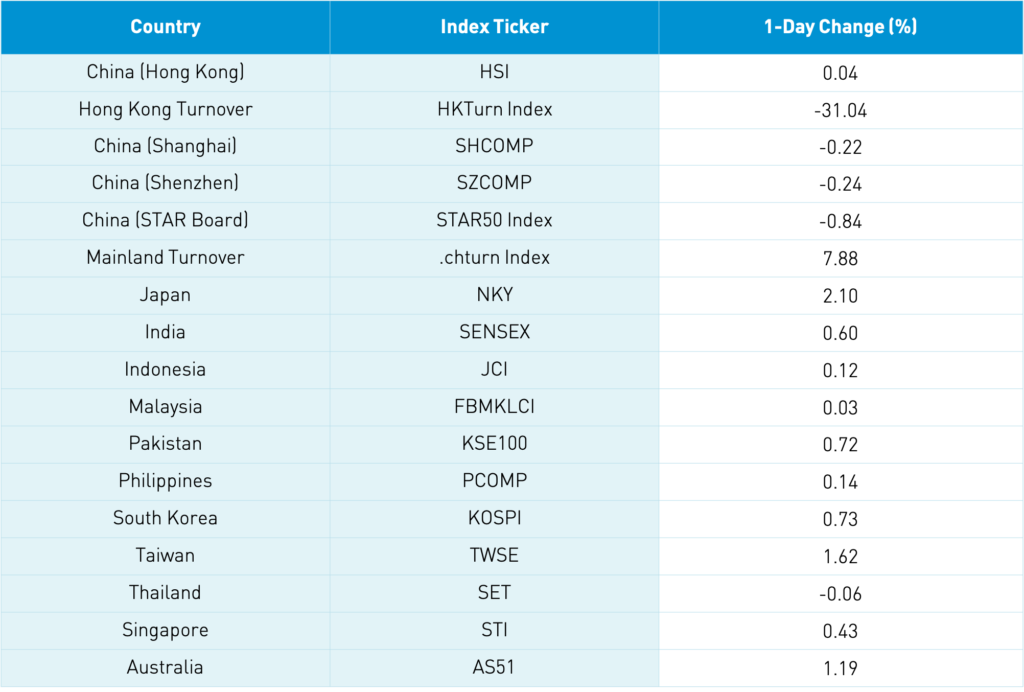

The Hang Seng eased in the afternoon to close +0.04% at 29,124 as volume slumped -31% from yesterday’s hyper-trading driven by the MSCI rebalance. Today’s volume was 106% of the 1-year average. The 211 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -0.95% with materials +1.28%, financials +0.8%, and utilities +0.53% while healthcare -3.47%, energy -2.35%, tech -1.78%, discretionary -1.65%, staples -1.46%, real estate -1.05%, and industrials -1.05%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.66%, JD Logistics, which gained +3.32%, Xiaomi, which fell -1.55%, Alibaba HK, which fell -0.67%, Meituan, which fell -2.43%, HSBC, which gained +3.78%, Wuxi Biologics, which fell -5.03%, AIA, which gained +0.98%, Ping An Insurance, which gained +0.12%, and China Construction Bank, which gained +1.75%. Southbound Connect volumes were moderate as Mainland investors sold a net $237 million worth of Hong Kong stocks today as Southbound trading accounted for 11.7% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were hit with profit taking to close off by -0.22%, -0.24%, and -0.84%, respectively, as volume increased +7.88% from yesterday, which is 111% of the 1-year average. 1,164 stocks advanced while 2,707 stocks declined. The 532 Mainland stocks within the MSCI China All Shares Index eased -0.18% with industrials +0.97%, financials +0.7%, and utilities +0.2%. Meanwhile, healthcare -1.91%, communication -1.26%, real estate -1.06% and tech -0.59%. The Mainland’s most heavily traded stocks by value were CATL, which gained +6.67%, broker East Money, which fell -0.35%, BOE Tech, which fell -2.63%, BYD, which gained +2.38%, Changan Auto, which gained +5.88%, Everdisplay Optronics IPO, which gained +58.49%, Longi Green Energy, which gained +2.24%, Industrial Securities, which gained +8.33%, Changchun High & New Tech, which fell -3.96%, and GEM, which gained +1.87%. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$82 million worth of Mainland stocks. CNY appreciated versus the US dollar, bonds eased, and copper rallied +2.19%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.38 yesterday

- CNY/EUR 7.76 versus 7.78 yesterday

- Yield on 1-Day Government 1.66% versus 1.61% yesterday

- Yield on 10-Year Government Bond 3.08% versus 3.07% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price +2.19%