Mainland Active Managers Seek To Increase Holdings of China Internet Stocks, Week in Review

5 Min. Read Time

Week in Review

- The official PMI and Caixin PMI data for May were released Monday. Business activity expectations for both “official” PMIs were strong, indicating that China and the global economy’s rebound is apt to continue.

- The PBOC will raise the foreign exchange reserve ratio on June 15th for Chinese banks to 7% from 5% on Tuesday, the first adjustment in fourteen years, as part of an effort to stem the currency’s strong rise year-to-date.

- Ant Group’s transition from an unregulated fintech to a regulated consumer finance company took a step forward as the CBIRC approved the new entity on Thursday. The move could accelerate an IPO, likely after a few quarters of operating as the new entity.

- The Biden administration announced this week that the list of banned Chinese stocks will be reviewed and maintained by the Treasury Department’s Office of Foreign Assets Control rather than the Defense Department going forward after two Chinese companies successfully challenged their presence on the list in court and won.

Key News

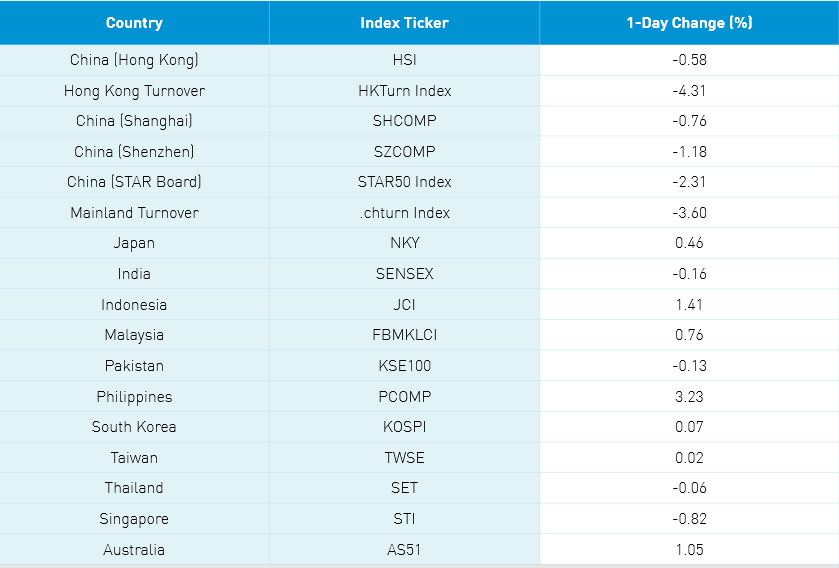

Asian equities were mixed as Southeast Asia outperformed and Northern Asia underperformed, the reverse of yesterday’s performance.

I would have bet my house that Hong Kong-listed Chinese internet companies would have done well last night due to the Hang Seng Index’s rebalance, which increased the weight of Alibaba while decreasing Tencent’s weight. If I had made that bet, it would have been an awkward breakfast this morning as active managers appeared to use the strong uptick in volume to reduce positions in the space. Optics matter for active managers as they release their holdings quarterly. Why would you hold the names with the China internet regulation headlines, US-China political rhetoric, and post-Archegos blow-up? It is easier to kick them to the curb than spend your day responding to clients defending the names. This is why I’m so bullish! The market usually does the opposite of what is expected, which I have seen several times over the last eight and a half years.

In Mainland China overnight, a star active manager asked for money from their investors by raising the amount investors can invest in his fund. We also had a Bloomberg article on another “star” Chinese portfolio manager recommending buying Chinese internet companies based on the fact that “…the valuations are working in their favor because they are much less liked by other investors.” I agree with her! Bloomberg notes that Tencent, Alibaba, and Meituan have lost $400 billion in market cap since mid-February. According to the Bloomberg article, the PM has beaten 96% of her peers over the last year. Since inception, our flagship strategy has beaten her $6.7B fund by 37%.

There has been a fair amount of chatter on the Biden Administration’s release of banned securities from the hastily thrown together year-end Executive Order. While headlines will tell you the number of companies increased, the number of stocks on the list fell. The administration moved the determination of the list away from the Department of Defense to the Treasury Department’s Office of Foreign Asset Control (OFAC), which should help with transparency and communication. It is funny to see Huawei on the list as it is a private company.

Mainland media noted the Ministry of Commerce spokesperson’s press conference post-US-China conversations with US Trade Representative Tai and Treasury Secretary Yellen as a “smooth start”. That is interesting considering the negativity here in the US.

Meituan’s founder and CEO donated 2.37% of his shares, worth $1.85 billion, to his charity. There was also chatter about Mainland China decreasing its stamp tax, which led to a rally in financial stocks led by brokers. However, it does not appear stocks’ stamp tax will be included in the tax cut, which is a shame.

Mainland electric vehicle-related stocks including metals had a strong day following GM’s comments on semiconductor shortages coming to an end.

US-listed Chinese education stocks were crushed yesterday on rumors policies will reduce the costs of tutoring to reduce the cost of raising children. However, I saw nothing on the subject in Mainland media nor did our institutional brokers, which had us all scratching our heads.

Since early May, Chinese stocks have made a comeback. Now we are seeing a mild pullback as indexes reach big round numbers. Shanghai is just below 3,600, Shenzhen is just above 2,400, and the Hang Seng Index is just below 29,000.

Policymakers are talking down commodity prices and the renminbi. This is working in the short term as CNY now at 6.40 versus May 28th’s low of 6.36 while copper was smoked overnight. I do not think the talk will overcome the invisible hand of the market, which is driven by supply/demand imbalances in the medium to long run.

Last weekend Barron’s interviewed the great Israeli behavioral finance genius Daniel Kahneman in a very good article. I found Kahneman’s Thinking, Fast and Slow a tough read candidly while Michael Lewis’ Undoing Project was very well done on Kahneman and partner Amos Tversky’s pioneering work on how emotions lead us astray. It made me think about how headlines often form our opinions and are anathema to data-driven analysis. Everything we do in finance is data-driven, but, when it comes to China, we allow headlines to form our opinions. The data tells a very different narrative.

CNY depreciated versus the US dollar to 6.40, bonds were off, and copper fell -2.66%

Happy birthday to my father this weekend!

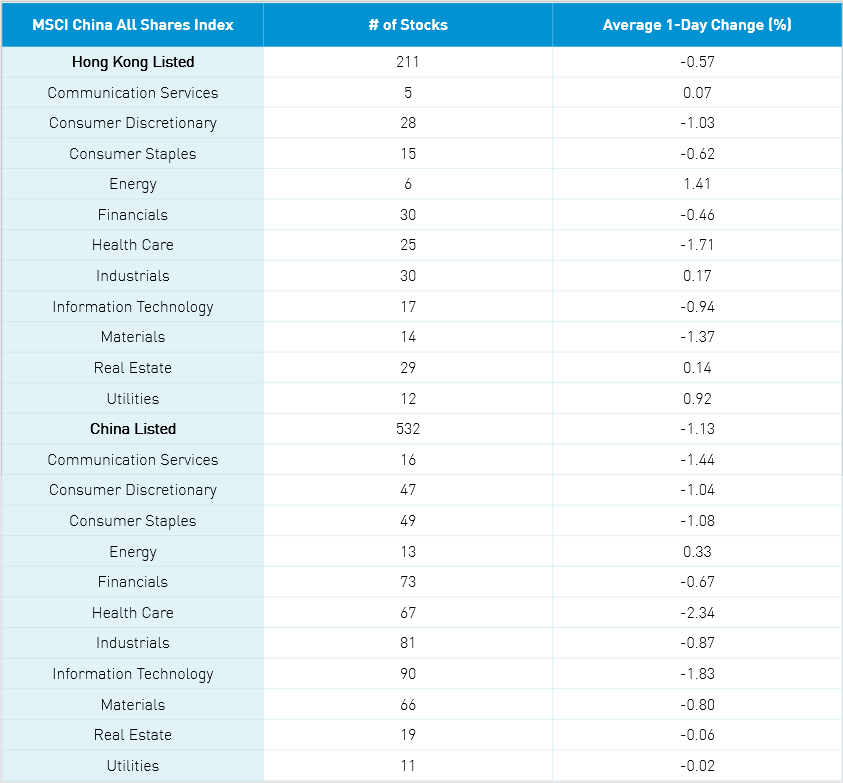

H-Share Update

The Hang Seng Index bounced around the room to close -0.17% at 28,918 as volume increased +38% from yesterday, which is 118% of the 1-year average. The 211 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -0.39% as financials +0.32% and utilities +0.27% while materials -2.96%, real estate -1.11%, tech -0.96%, industrials -0.88% and staples -0.58%. Hong Kong’s most heavily traded stocks by value were Xiaomi, which fell -1.5% despite being removed from the EO list and was sold heavily via Southbound Connect, Meituan, which fell -1.69% despite very heavy buying via Southbound Connect, Tencent, which fell -0.65%, Alibaba HK, which fell -0.28%, AIA, which gained +0.41%, BYD, which gained +1.16%, e-cigeratte company Smoore, which fell -11.27%, Geely Auto, which gained +6.21%, Country Garden Services, which fell -4.14%, and Ping An Insurance, which fell -0.55%. Southbound Stock Connect Volumes were elevated as Mainland investors sold $140 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 11.5% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +0.21%, +0.63%, and +1.2%, respectively, as Mainland turnover fell -1.73%, which is 102% of the 1-year average. Breadth was dismal with 1,630 advancers and 2,243 declining stocks. The 532 Mainland stocks within the MSCI China All Shares Index gained +0.63% led by financials +1.06%, industrials +0.97%, communication +0.94%, staples +0.91%, healthcare +0.6%, tech +0.42% while real estate -1.07%, energy -0.81% and utilities -0.49%. The most heavily traded stocks by value in the Mainland were broker East Money, which gained +0.52%, CATL, which gained +4.2% though was heavily sold in Northbound Connect, Kweichow Moutai, which gained +1.32%, BYD, which gained +2.99%, Wuliangye Yibin, which gained +0.54%, Longi Green Energy, which fell -1.11%, Eve Energy, which fell -1.12%, Sany Heavy Industry, which fell -1.12%, Sungrow Power, which fell -2.84%, and Tianqi Lithium, which gained +2.13%. Northbound Stock Connect volumes were moderate as foreign investors bought $479 million worth of Mainland stocks today as Northbound Connect trading accounted for 5.8% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.40 yesterday

- CNY/EUR 7.78 versus 7.77 yesterday

- Yield on 1-Day Government Bond 1.60% versus 1.65% yesterday

- Yield on 10-Year Government Bond 3.09% versus 3.06% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price -2.66% overnight