China Trade Data Highlights Commodity Demand

3 Min. Read Time

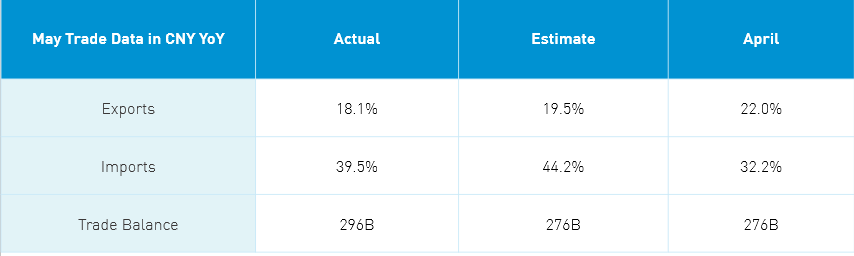

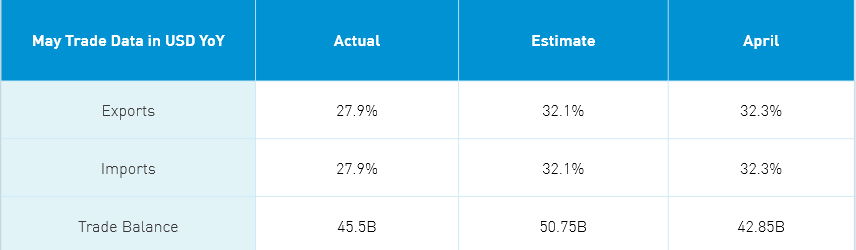

Trade Data Overview

Takeaway: May trade data was quite strong as the percentage change is compared to a year ago, making for a low bar comparison. Export growth is likely to accelerate in the months ahead as the global economy comes back online. Yes, exports and imports slightly missed expectations, though May had fewer days than April due to China’s Labor Day holiday. Exports to the US jumped +17% year over year (YoY), which was the most of any trade counterparty and was likely driven by agricultural purchases. Commodity imports were largely the same in tons month over month (iron ore was off, soybeans were up) though the dollar value of the imports all rose due to higher commodity prices. It is worth noting that trade data solely focused on goods that are put on a plane or ship. If General Motors builds a car in China and sells it in China, it does not show up in this data at all. If GM builds a car in China, puts it on a boat, and sells it in another country, that shows up as a China export even though the profits flow back to Detroit. Then there are services such as accountants, lawyers, computer software, etc. that are not shown in this data. This might be one reason institutional brokers did not believe today’s strong release had a meaningful impact on trading.

Key News

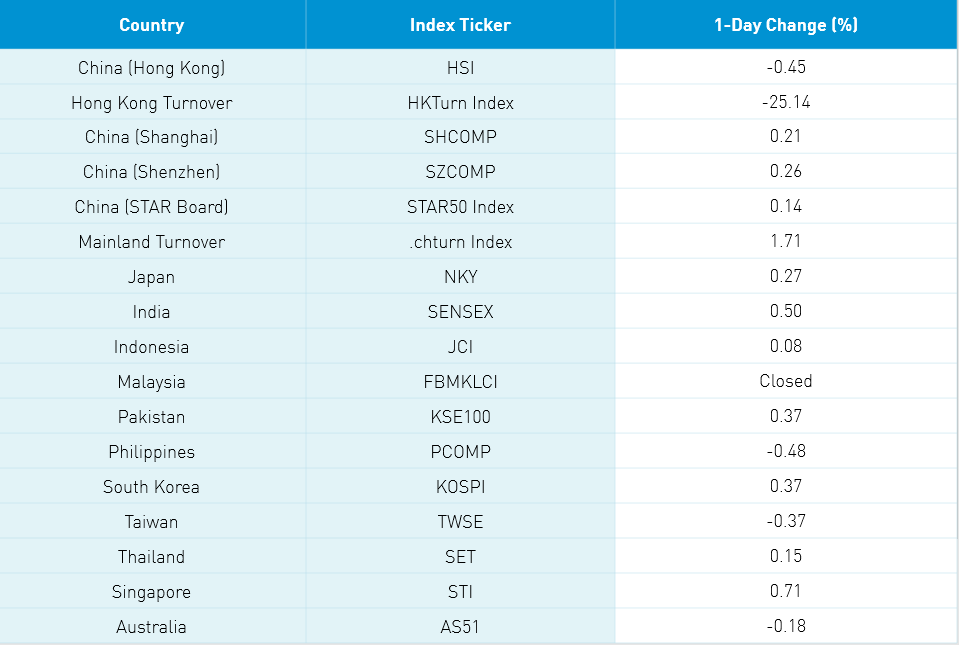

Asian equities were mixed overnight as Janet Yellen’s veiled reference to higher interest rates and a global tax agreement on multi-national companies weighed on growth names in Hong Kong, Taiwan, and South Korea. Mainland China-listed electric vehicle battery maker CATL was off as cornerstone investors’ shares will be unlocked on its three-IPO anniversary on June 11th. Meanwhile, Huawei-related stocks outperformed again including semiconductors following the company’s new smartphone release last week. Real estate was off on reports of a pilot program to tax land sales and transfers, which could lead to a wider implementation of real estate taxes. All in all, it was a quiet night, though one broker noted a fair amount of negative US-China headlines (Taiwan visit, Wuhan lab leak, etc.) which likely weighed on sentiment.

Last Friday at 4 pm EST, SEC Chair Gary Gensler removed Wiliam Duhnke as the head of the PCAOB. The rationale behind the move was not explained, though Senators Warren and Sanders used some unflattering terminology to describe PCAOB head during Gensler’s confirmation hearing. The move could have the unintended consequence of resolving the long-standing audit issue of US-listed Chinese companies. Our DC sources reported Duhnke was unwilling to engage the CSRC, China’s SEC, on the issue despite the Chinese side reaching out several times.

H-Share Update

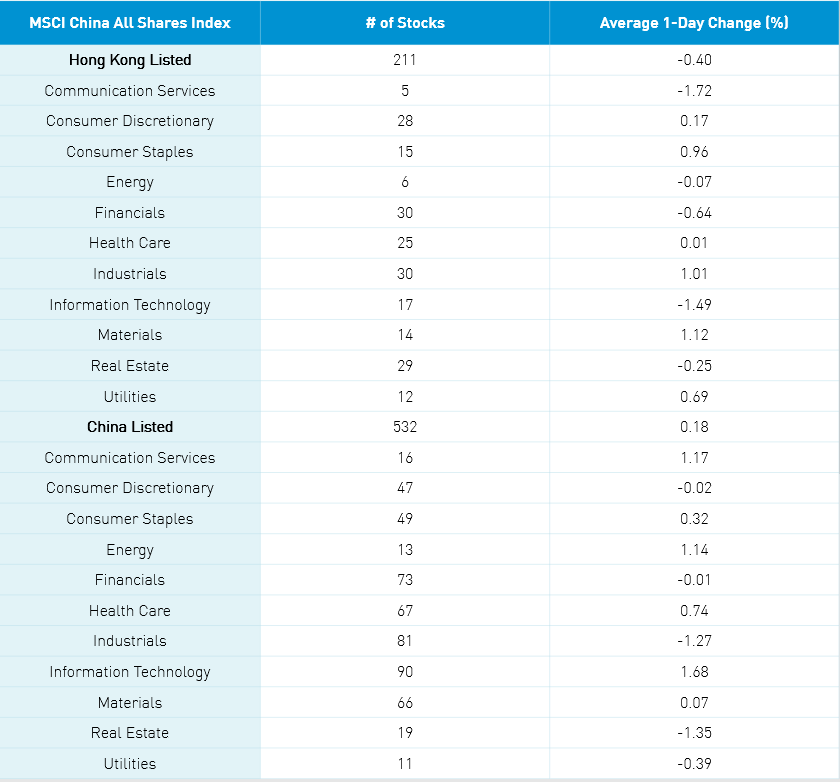

The Hang Seng posted a loss of -0.45% as volume collapsed -25% from Friday’s high volume, driven by the index rebalance to just 88% of the 1-year average. The 211 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index lost -0.4% with materials +1.12%, industrials +1.01%, staples +0.96%, and utilities +0.69%. Meanwhile, communication -1.72%, tech -1.49%, financials -0.64%, and real estate -0.25%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.8% after it was reported that President Lau sold a small amount of his shares, Xiaomi, which fell -4.06%, Meituan, which fell -0.73%, Alibaba HK, which gained +0.86%, Geely Auto, which fell -5.7%, Ping An Insurance, which fell -0.31%, energy giant CNOOC, which gained +2.35%, e-cigarette maker Smoore, which gained +2.83%, AIA, which fell -0.61%, and pork giant WH Group, which gained +7.71% on a buyback announcement. Southbound Stock Connect volumes were moderate/high as Mainland investors sold -$186 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 14.4% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board posted gains of +0.21%, +0.26%, and +0.14%, respectively, as volume increased +1.71% from Friday, which is 103% of the 1-year average. There were 2,235 advancing stocks and 1,638 declining stocks today. The 532 Mainland stocks within the MSCI China All Shares Index gained +0.17% led by tech +1.66%, communication +1.15%, energy +1.12%, healthcare +0.73% and staples +0.31% while real estate -1.37%, industrials -1.28%, utilities -0.41%. The Mainland’s most heavily traded stocks by value were CATL, which fell -5.72%, broker East Money, which gained +0.58%, Inner Mongolia Yili, which fell -4.78% after a share sale, GEM Co, which fell -8.39%, liquor company Wuliangye Yibin, which fell -0.76%, rival Kweichow Moutai, which gained +0.87%, Hangzhou Silan Microelectronic, which gained +10.01%, Longi Green Energy, which fell -1.91%, BYD, which gained +0.5% after car sales jumped 56% to 195k units, and COSCO Shipping, which gained +5.63%. Northbound Stock Connect volumes were moderate as foreign investors sold -$620 million worth of Mainland stocks today as Northbound trading accounted for 5.3% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.40 Friday

- CNY/EUR 7.79 versus 7.78 Friday

- Yield on 1-Day Government Bond 1.72% versus 1.60% Friday

- Yield on 10-Year Government Bond 3.11% versus 3.09% Friday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% Friday

- Copper Price +0.79% overnight