JD & NetEase Momentum Leads To Index Inclusion, Week in Review

3 Min. Read Time

Week in Review

- China’s retail sales beat estimates for October, according to an official release Monday. Industrial production and fixed asset investment also came in slightly higher than anticipated for the month while property investment was weak as curbs on real estate lending continued to take effect in October.

- Asian equities had a strong session on Monday, but saw declines later in the week, mirroring the US market, as inflation concerns in the US and covid lockdowns in Europe weighed on global market sentiment.

- Netease, Baidu, JD.com, and Alibaba all reported Q3 earnings this week with mixed results. JD.com, Netease, and Baidu beat estimates, while Alibaba’s release was less than stellar as cost of revenues increased due to strong investment in new businesses, though the E-Commerce giant continued to add users and buy back shares during the quarter.

- The Biden-Xi virtual summit Monday night had a muted impact on markets, though communication between the two leaders should be viewed as a positive. China clean energy stocks rallied this week on hopes for US-China cooperation on climate.

Friday’s Key News

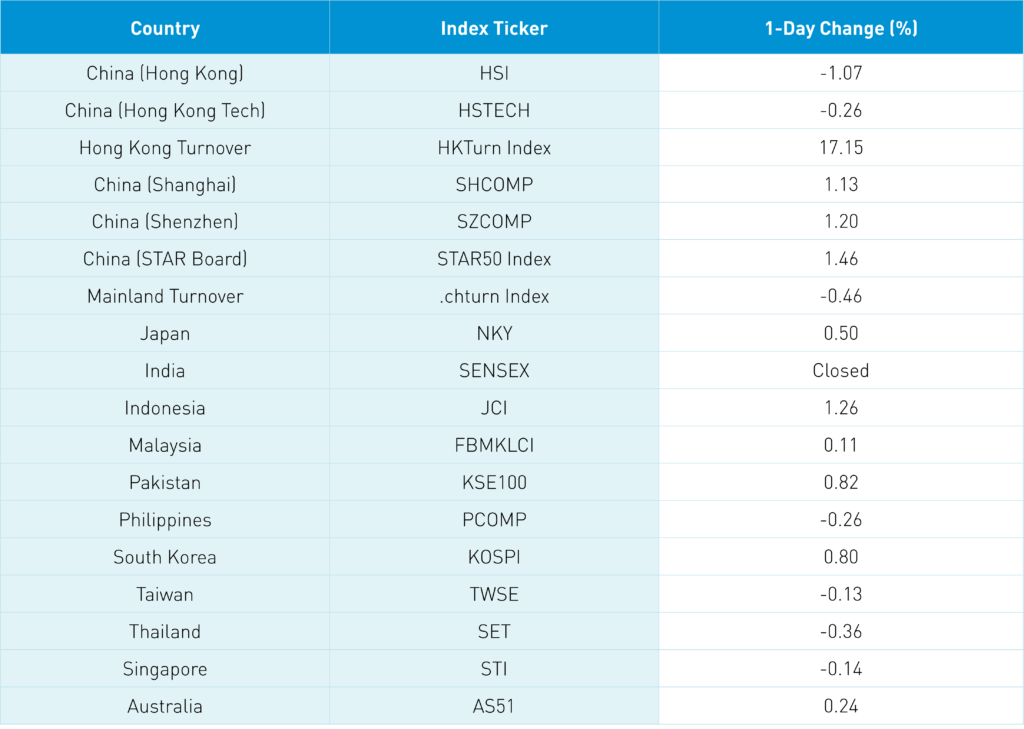

Asian equities ended the week largely higher as Mainland China outperformed, Hong Kong underperformed, and India’s market was closed. The Hang Seng was off -1.07% on volume that was +17% higher than yesterday, which is just 80% of the 1-year average.

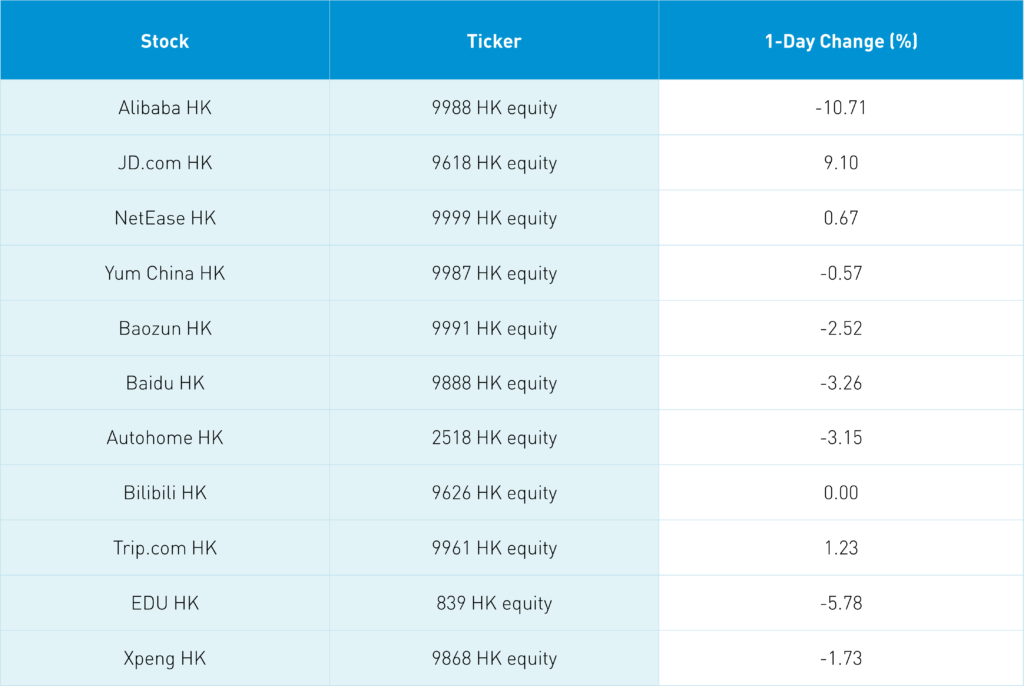

Alibaba HK’s -10.71% performance accounted for 186 of the Hang Seng’s 269-point loss. Alibaba headlines are all about the company’s weak growth driven by weak Chinese consumption. Investors appear to be ignoring that the company grew revenues by 29% year-over-year! Active customers globally increased by 62 million to 1.24 billion. There are only eleven companies globally with a market cap above $350 billion that grew revenue more than +20% in Q3, year-over-year. 11! BABA’s P/E of 24 is the lowest of the 11 at less than half the average P/E of 69 (Tesla’s P/E of 352 does skew this). The company had indicated in the previous quarter that they would increase expenditures and invest in their core businesses though analysts clearly did not mark down their net income and EPS estimates based on that guidance. Do not count Alibaba out as it has a strong management team.

JD.com’s strong Q3 performance also dismisses the China consumer slowdown narrative. Overnight, JD.com’s Hong Kong share class gained +9.1% versus yesterday’s US share class gain of +5%.

After the close, Hang Seng Indexes announced that both JD.com HK and NetEase HK, who also had a strong Q3, will be added to the Hang Seng Index along with China Resources Beer and ENN Energy on December 6th.

Weibo’s Hong Kong listing was approved though the size of the listing has yet to be revealed.

Bilibili announced they will be issuing a $1.4 billion convertible bond, which is not going to help equity investors due to the potential dilution event of more equity shares being issued upon conversion.

Tencent and Meituan were both off -0.16% and -1.61% as both saw net selling from Mainland investors via Southbound Stock Connect.

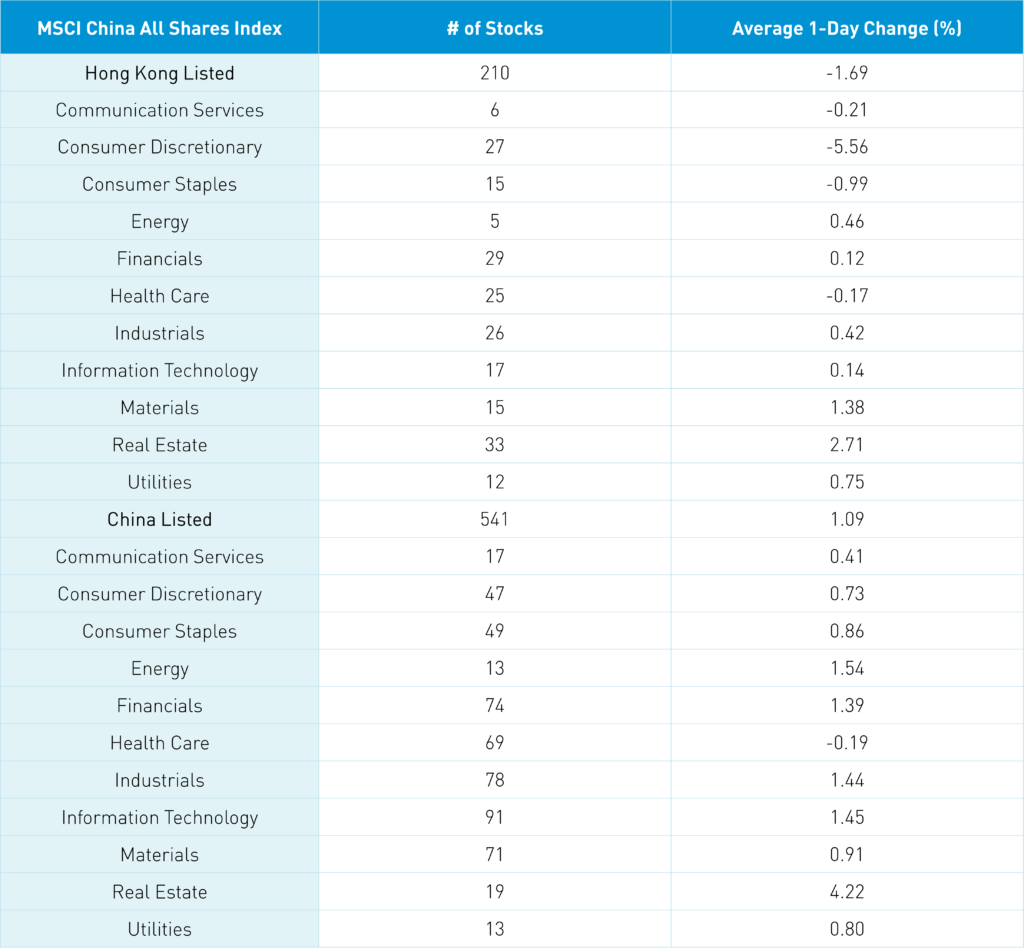

Real estate was the best performing sector in Hong Kong, gaining 2.71%, and in China, where the sector was up +4.22%.

Apart from the Alibaba downdraft, there was a significant disparity between Hong Kong and China today. For instance, BYD fell -0.99% in Hong Kong while its China share class gained +0.48%. Yicai reported on the chairman’s speech in which he predicted 3.3mm EVs will be sold in China in 2022, which would represent 35% of autos sold. Coincidentally, we have heard similar projections. The point is it appears that the disparity between foreign pessimism and what investors in China are focused on has never been greater.

Mainland markets were led higher by the clean technology ecosystem, which includes electric vehicles, solar, and wind, as Shanghai gained +1.13%, Shenzhen gained +1.2% and the STAR Board gained +1.46% on volume that was -0.46% lower than yesterday though still 110% of the 1-year average. It was a broad rally with advancers outpacing decliners by 3 to 1. Foreign investors bought a healthy $1.3 billion worth of Mainland stocks today via Northbound Stock Connect. For the week, foreign investors bought a net $1.7 billion worth of Mainland stocks. Bonds were sold today, CNY was off a touch versus the US dollar, and copper rallied.

Kuaishou Technology reports next Tuesday while Pinduoduo and Meituan report next Friday.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.38 yesterday

- CNY/EUR 7.21 versus 7.24 yesterday

- Yield on 10-Year Government Bond 2.93% versus 2.91% yesterday

- Yield on 10-Year China Development Bank Bond 3.19% versus 3.18% yesterday

- Copper Price +1.00% overnight