Tencent Denies Financial Times Divestment Article, Week in Review

4 Min. Read Time

Week in Review

- Asian equities had a mixed week as US dollar strength and Fed Chair Powell’s hawkish comments from Jackson Hole weighed on local currencies in the region, and China reported mixed economic indicators, showing an expansion of the services economy and a contraction in manufacturing in August.

- E-Commerce giant Pinduoduo, food delivery company Meituan, and search engine turned AI maverick Baidu all reported Q2 results that beat pessimistic analyst estimates.

- Investors reacted negatively to a Reuters article on Wednesday stating that the company would undergo an audit review by the US Public Company Accounting Oversight Board (PCAOB), though the company stands by the integrity of its financial statements, and we believe this should be viewed as a positive.

- Semiconductor stocks and the broader technology sector were down sharply on Thursday as chipmaker Nvidia warned that a US export restriction could place $400 million of its China revenue at risk. The company is likely to appeal the decision.

Friday’s Key news

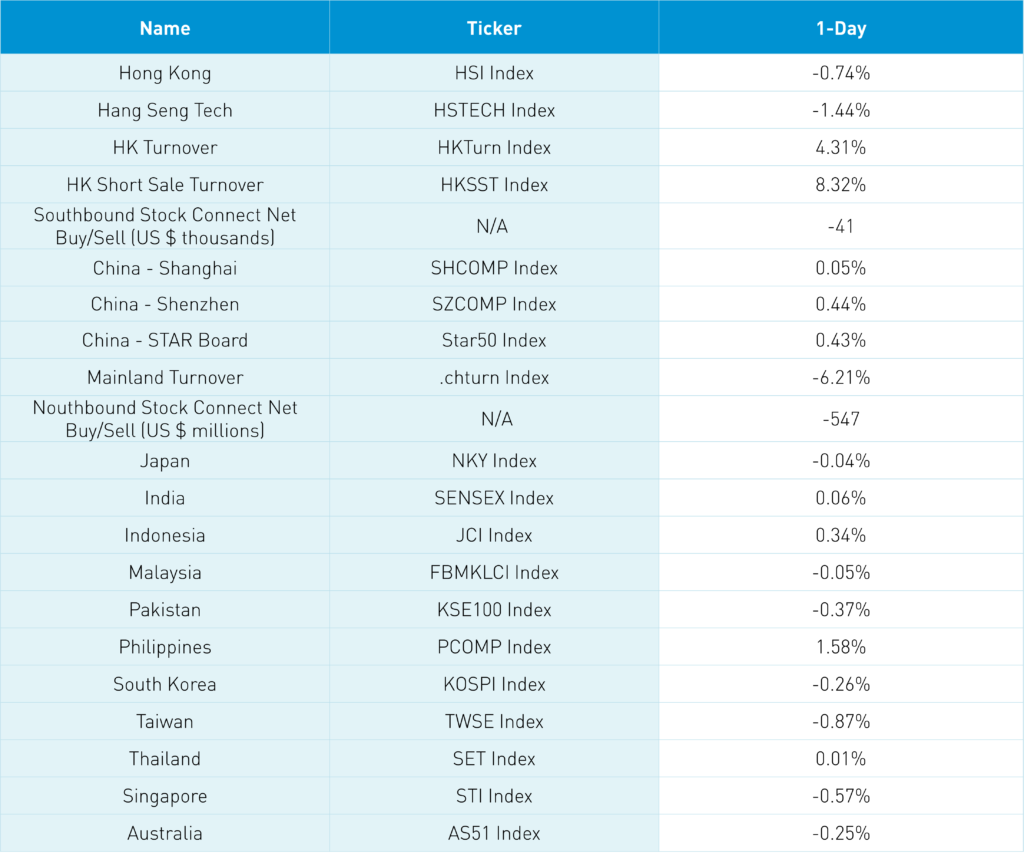

Asian equity markets were mixed on light volumes except for China and South Asian equity markets in advance of today’s US jobless number, which came in stronger than anticipated.

The Bloomberg JP Morgan Asia Dollar Index broke the 100 level yesterday, closing at 99.99, which was last seen back in September 2004. The Chinese renminbi was off just a touch.

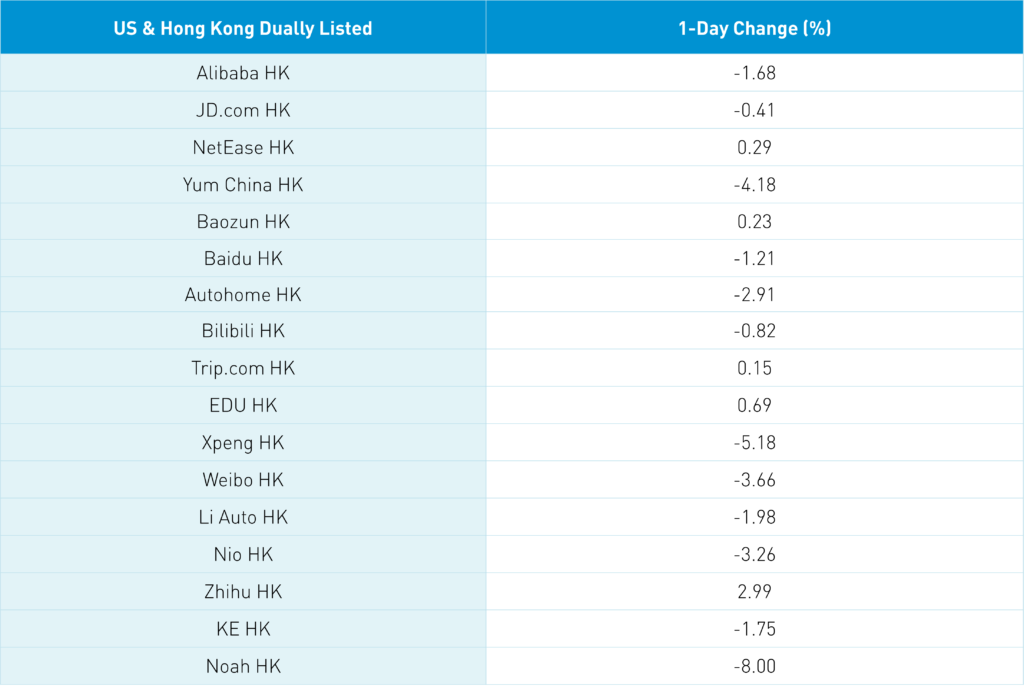

There has been a fair amount of chatter about Hong Kong reopening in November. However, the market was off today. Hong Kong-listed internet stocks were off, but less so than their US-listed counterparts yesterday. Tencent gained +1.23% after denying an article in the Financial Times stating that the company would unload $14.5 billion of its equity portfolio. Alibaba fell -1.68%, Meituan fell -1.14%, JD.com fell -0.41%, and Baidu fell -1.21%. The Financial Times (FT) article absolutely pummeled the stocks that Tencent owns, including Meituan and Kuaishou. However, the company’s denial was through a Mainland media source and was not on their investor relations page. I have not seen any corroborating media stories written based on the FT article nor the FT article itself amended based on the company’s denial.

While Hong Kong volumes were light overnight, at just 84% of the 1-year average, short turnover was 111% of the 1-year average. Tencent had 21% of its volume sold short versus yesterday’s 23%, JD.com HK had 35% short versus yesterday’s 43%, Meituan had 22% short versus yesterday’s 27%, and NetEase had 26% short versus yesterday’s 27%. Alibaba fell off today’s top ten most heavily shorted leaderboard.

Two US Senators are proposing a bill that would label US-listed Chinese companies due to their VIE structure. Bills are proposed all the time, so we have no clue whether this will pass but the timing is interesting as US auditors are preparing to leave for Hong Kong to conduct inspections. We recommend reading our VIE structure Q&A for anyone who wants to examine the facts of the structure. Candidly, they blame China for every problem and the narrative is getting a little tired and out-of-date.

The China Securities Regulatory Commission (CSRC) Vice Chairman Fang Xinghai gave a speech in China today, stating that “China and the United States have successfully signed a cross-border listed company audit and supervision cooperation agreement…”. What’s interesting is that he had just prior to this comment stated: “The China Securities Regulatory Commission has earnestly implemented the requirements of the CPC Central Committee and the State Council…”. It sounds like the audit deal got the green light from senior government leadership, a very positive sign.

Mainland China managed a small up day despite mass testing in Chengdu and restrictions in Shenzhen. Premier Li and the State Council’s economic stimulus plan, which had an emphasis on housing, has not given the market the jump that one would have hoped for. Based on the market’s reaction, we may see a more demonstrative move.

The Caixin Services PMI will be reported this weekend with expectations at 54 versus July’s 55.5.

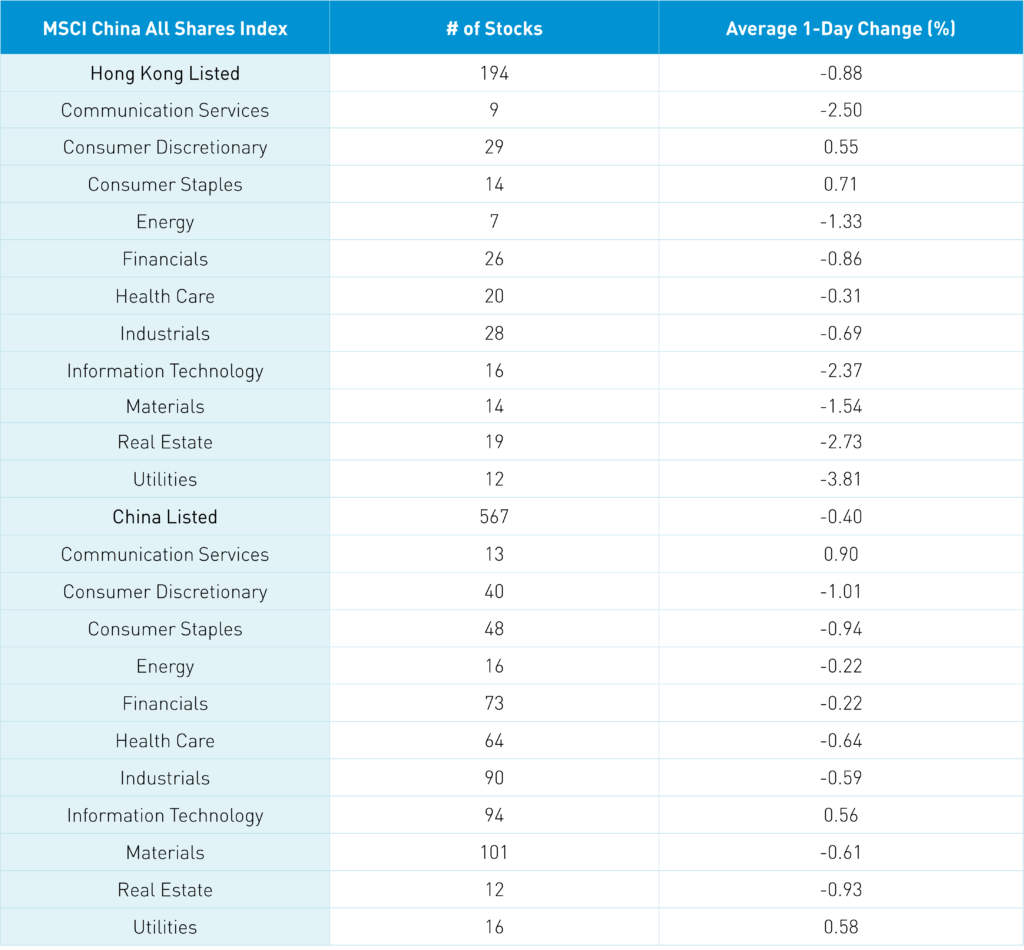

The Hang Seng and Hang Seng Tech indexes fell -0.77% and -1.44%, respectively, on volume that increased +4.31% from yesterday, which is 84% of the 1-year average. 113 stocks advanced while 363 declined. Hong Kong short sale turnover increased +8.31% from yesterday, which is 111% of the 1-year average, as short trading accounted for 22% of total turnover. Growth and value factors both performed poorly, while small caps “outperformed” large caps by a small amount. Communication and utilities were the only green sectors, gaining +0.71% and +0.55%, respectively. Meanwhile, real estate fell -3.81%, tech fell -2.73% and materials fell -2.5%. The top performing sub-sectors were online education, electric utilities, and fintech. Meanwhile, semiconductors, property management, and gold were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$41 million worth of Hong Kong stocks as Tencent was a slight net buy, Kuaishou was a very small net buy, and Meituan was sold moderately.

Shanghai, Shenzhen, and the STAR Board gained +0.05%, +0.44%, and +0.43%, respectively, on volume that fell -6.21% from yesterday, which is 71% of the 1-year average. 3,191 stocks advanced while 1,282 stocks declined. Value and growth factors were mixed as small caps outperformed large caps. The top performing sectors were communication, which gained +0.9%, utilities, which gained +0.58%, and tech, which gained +0.56%. Meanwhile, discretionary fell -1.01%, consumer staples fell -0.94%, and real estate fell -0.93%. The top performing sub-sectors included satellite, industrial gases, and hardware. Meanwhile, CROs (contract research organizations/outsourced pharma manufacturers), liquor, and food were among the worst. Northbound Stock Connect volumes were moderate as foreign investors sold -$547 million worth of Mainland stocks today. Treasury bond prices declined, CNY was off -0.02% versus the US dollar to 6.91, and copper was hit -1.77%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.91 versus 6.90 yesterday

- CNY/EUR 6.90 versus 6.91 yesterday

- Yield on 10-Year Government Bond 2.62% versus 2.61% yesterday

- Yield on 10-Year China Development Bank Bond 2.80% versus 2.79% yesterday

- Copper Price -1.77%