Yum China Reports Q1, China PMIs Mixed

4 Min. Read Time

Key News

Asian equities were mixed overnight in advance of tomorrow’s Labor Day holiday as Japan outperformed following its holiday yesterday.

Growth stocks were off in both Hong Kong and Mainland China as investors took profits in outperforming sectors and stocks. Helping today’s skew of value over growth were Mainland financial results, which indicated that mega-banks and big energy are doing well versus brokerage, insurance, and weak clean tech results from solar companies. Foreign investors lightened up on their purchases of Mainland stocks, selling a healthy $1.19B via Northbound Stock Connect to avoid having their money not working in Mainland China, which will be closed until next Monday.

In morning trading, the “official” April PMIs saw Manufacturing beat expectations of 50.3 with the 50.4 release, though off from March’s 50.8, and Non-Manufacturing missed expectations of 52.3 with the release of 51.2 and off from March’s 53. The Caixin Manufacturing PMI beat expectations of 51 with 51.4 and March’s 51.1. The “official” PMI survey conducted by the National Bureau of Statistics focuses on large companies, while the Caixin survey, conducted by S&P’s IHS Markit, focuses on smaller companies.

There were several policy announcements overnight, including the Politburo’s meeting focused on “efforts to effectively implement the already determined macro policies, implement a proactive fiscal policy and a prudent monetary policy”. Actions will include issuing “ultra-long term special national bonds,” which I assume means taking advantage of China’s very low interest rates. In my opinion, it is a smart move, and it is too bad that the US Treasury hasn't done the same. The release also noted the effort to “…use policy tools such as interest rates and deposit reserve ratios, increase support for the real economy…”.

Real estate support was also featured prominently. The Third Plenum, the government’s big economic meeting, which will take place in July, focused on “deepening reforms and promoting Chinese-style modernization.”

Real estate was hit with profit-taking despite Nanjing eliminating home purchase restrictions, with Mainland media highlighting similar policies from Dalian, Huizhou, and Dezhou.

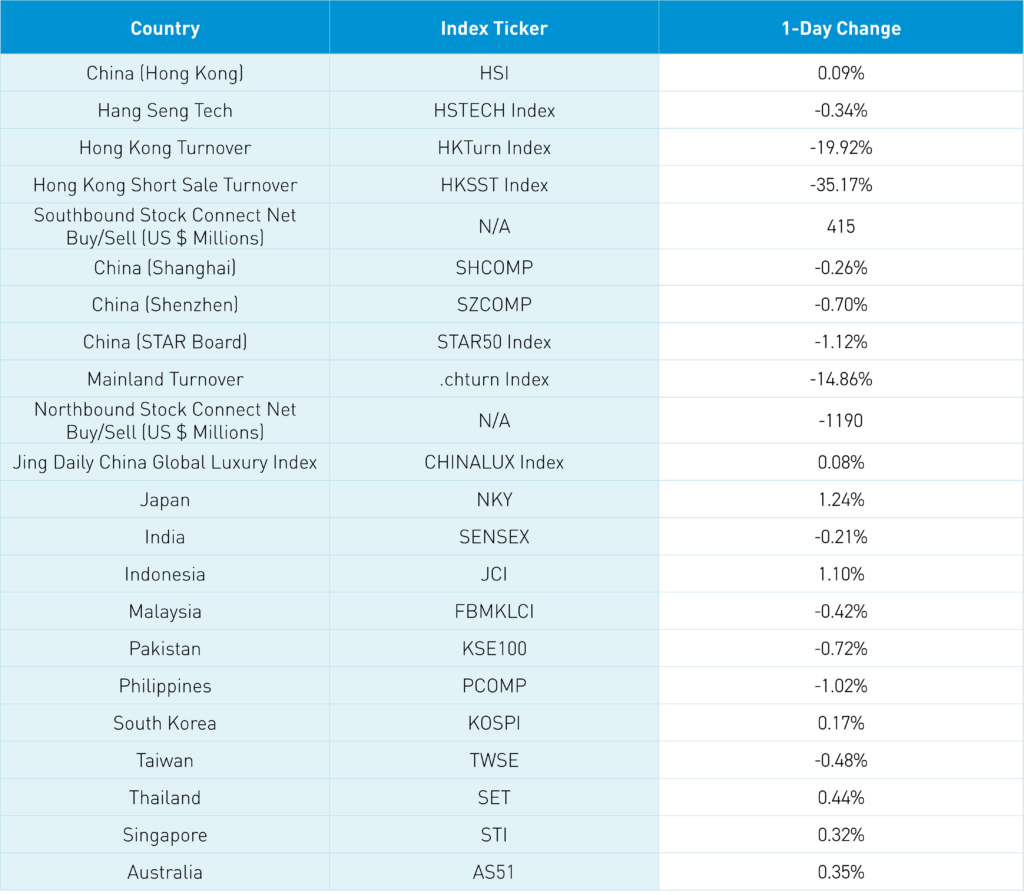

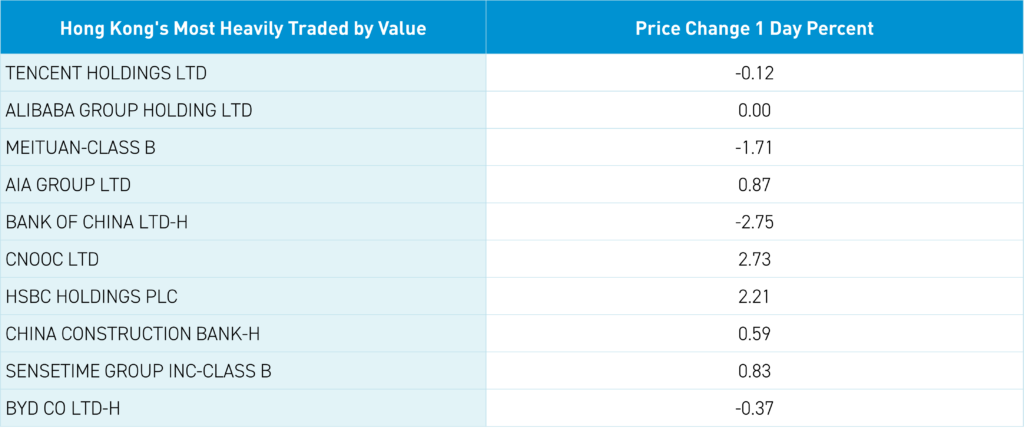

Still, profit-taking ruled the day as Hong Kong’s most heavily traded stocks were Tencent, which fell -0.12%, Alibaba, which was flat, Meituan, which fell -1.71%, AIA, which gained +0.87%, and the Bank of China, which fell -2.75% (the Bank of China’s Mainland share class gained +0.44%). Mainland investors bought the dip in Hong Kong through net purchases of $415 million worth of Hong Kong-listed stocks and ETFs today. Mainland markets bounced around the room, though they fell into the close with growth and small caps falling further.

China Last Night will be taking the day off tomorrow as both Hong Kong and Mainland China will be closed for Labor Day, which runs until next Monday for the latter. Domestic consumption has had a slow rebound due to conservatism around zero COVID and household exposure to real estate. If you were going to start to spend, what would you do first? I would take my wife out to dinner. Then, I’d plan a vacation. There are signs that the consumption hibernation is thawing, as we saw in the Q4 2023 financial results from restaurant chains and travel agencies. Fliggy, Alibaba’s online travel platform, reported yesterday that “outbound travel bookings during the holiday in 2024 doubled year-on-year”. International travel costs more than domestic travel with popular destinations including Japan, Thailand, South Korea, and Australia. Another sign that reports of Chinese consumers’ death are greatly exaggerated!

Yum China, which operates multiple American fast food chains including Taco Bell and KFC in China, fell -6.24% after announcing Q1 2024 financial results, with revenue missing expectations despite revenue hitting an all-time high. Remember, Q1 2023 was just after the removal of Zero COVID, making for a tough year-over-year (YoY) comparison. In the management call, management highlighted the new “juicy pineapple beef burger” but, more importantly, provided interesting macroeconomic insights. Northern China is recovering faster, and the “eastern part of China continues to be very resilient, which is brilliant.” Tier 2 cities are the best performers, while “sales at shopping malls, where we have more stores, have surpassed the 2019 level… China last year actually added about 400 shopping malls to the base of about 6,000 shopping malls that we are tracking.” Even management noted that China building more malls is interesting, which I would agree with! The company repurchased 16.6 million shares in Q1 2024 with another $853 million worth of shares available for future share repurchase under the current program, along with a $0.16 dividend approved.

- Revenue was +1% YoY to $2.958B from $2.917B versus expectations of $3.021B

- Adjusted Net Income was -1% YoY to $287mm from $289mm versus expectations of $266mm

- Adjusted EPS increased to $0.71 from $0.68 versus expectations of $0.65

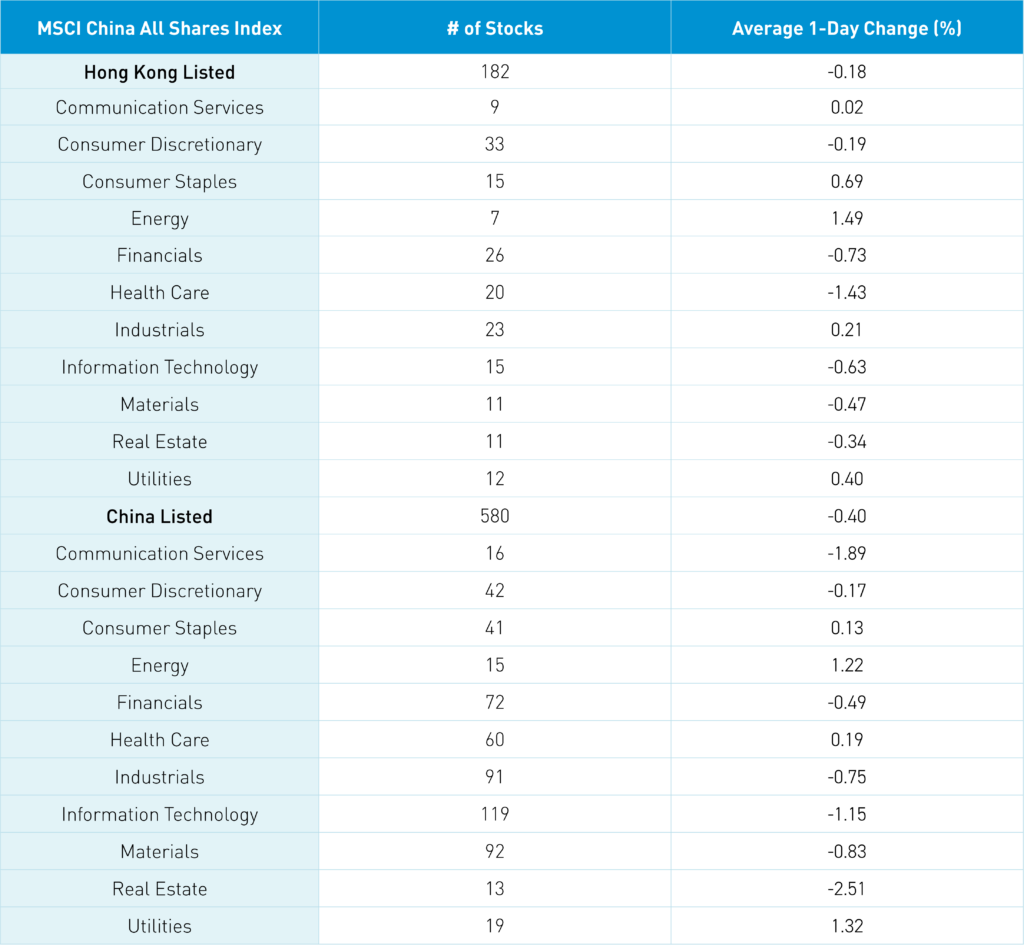

The Hang Seng and Hang Seng Tech indexes diverged to close +0.09% and -0.34%, respectively, on volume that decreased -19.92% from yesterday, which is 133% of the 1-year average. 224 stocks advanced, while 259 declined. Main Board short turnover declined -35.17% from yesterday, which is 94% of the 1-year average, as 13% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and large caps didn’t fall as much as the value factor and small caps. The top sectors were energy +1.48%, staples +0.68%, and utilities +0.39%, while healthcare -1.44%, financials -0.75%, and tech -0.64%. The top sub-sectors were household products, consumer durables, and energy, while diversified financials, insurance, and capital goods were the worst. Southbound Stock Connect volumes were moderate/high as mainland investors bought $415mm of Hong Kong stocks and ETFs, with Bank of China a large net buy.

Shanghai, Shenzhen, and the STAR Board all closed lower -0.26%, -0.70%, and -1.12%, respectively, on volume that decreased -14.96% from yesterday, which is 121% of the 1-year average. 1,982 stocks advanced, while 2,909 declined. The value factor and large caps fell less than the growth factor and small caps. The top-performing sectors were Utilities, which gained +1.32%, Energy, which gained+1.22%, and Health Care, which gained +0.20%. Meanwhile, Real Estate fell -2.51%, Communication Services fell -1.89%, and Technology fell -1.14%. The top-performing subsectors were household appliances, marine/shipping, and soft drinks. Meanwhile, autos, business services, and power generation equipment were among the worst-performing subsectors. Northbound Stock Connect volumes were very high as foreign investors sold a healthy net -$1.2 billion worth of Mainland stocks, including China Merchants Bank, CATL, and Midea Group, which were small net buys. Meanwhile, Focus Media, Nari-Tech, and Kweichow Moutai were moderate net sells. CNY and the Asia Dollar Index were basically flat versus the US dollar. Treasury bonds rallied. Copper had another nice gain with steel flat.

Last Night Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.24 yesterday

- CNY per EUR 7.76 versus 7.75 yesterday

- Yield on 10-Year Government Bond 2.30% versus 2.35% yesterday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.46% yesterday

- Copper Price +1.29%

- Steel Price unchanged