Tesla & Baidu Venture Wins, Panda Diplomacy, & Another Massive Net Buy Day In Northbound Stock Connect

3 Min. Read Time

Key News

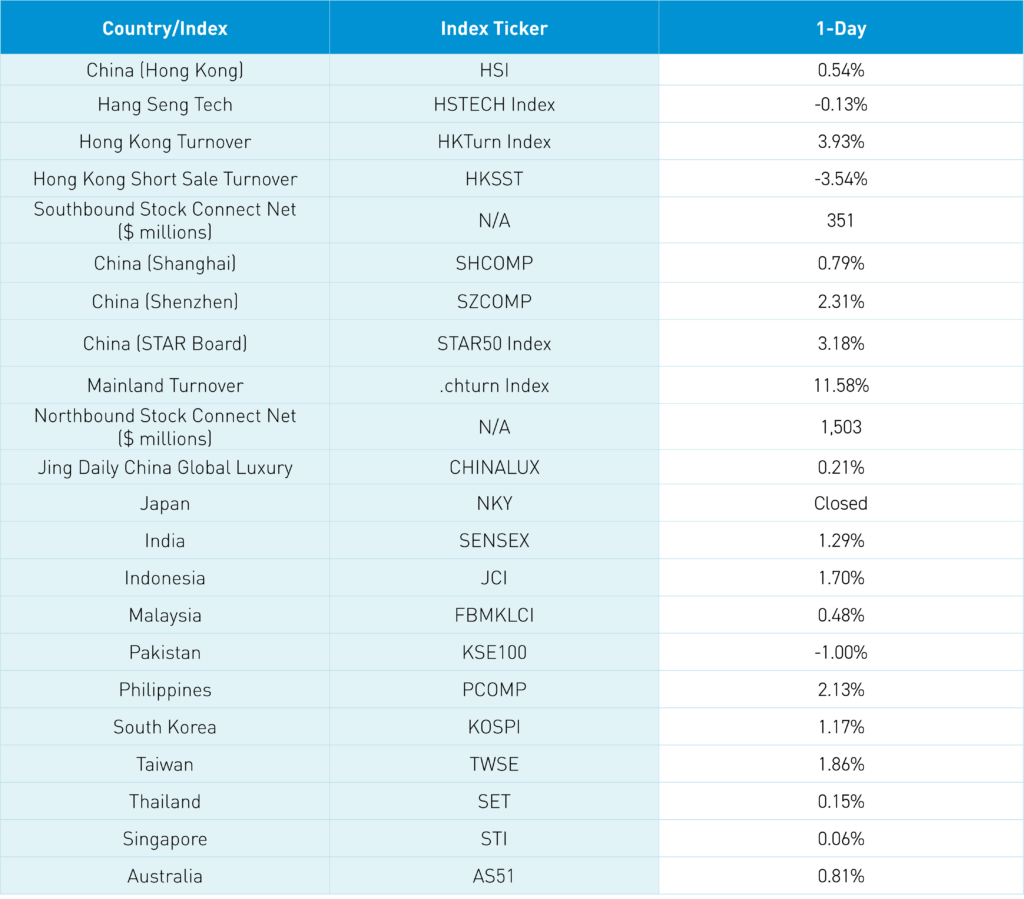

Asian equities had a strong night as Mainland China, Taiwan, South Korea, Indonesia, the Philippines, and India posted +1% returns, though Japan was closed for Showa Day in honor of Emperor Showa (Hirohito), who reigned from 1926 to 1989.

Real estate was the top-performing sector in both Hong Kong, where it gained +4.4% and Mainland China, where it gained +6.39% on reports that Chengdu lifted property purchase restrictions following similar policy purchase adjustments from Beijing, Shenzhen, and Nanjing. Remember, the real estate stock sector is small and very volatile, which is why we prefer real estate bonds for access.

Speaking of Chengdu, the San Diego Zoo and the China Wildlife Conservation Association (CWCA) announced that two pandas will be delivered soon following the San Francisco Zoo’s similar announcement last week. The revival of panda diplomacy is a good sign, as Secretary of State Blinken’s China visit did not receive any rave reviews, but at least the two sides are talking.

Elon Musk’s surprise China visit around the Beijing Auto Show included meeting with Premier Li, Tesla’s “compliance with Beijing’s data security rules,” and use of Baidu’s map and navigation for fully autonomous driving. Surprisingly, Baidu’s Hong Kong-listed shares were up only +2.38%.

Hong Kong reversed from intra-day highs after the Hang Seng Index touched the 18,000 level, sparking a wave of profit-taking. The profit-taking takes place before Hong Kong’s Wednesday Labor Day holiday while Mainland China is closed Wednesday until next Monday. Hong Kong had very high volume, which was 167% of the 1-year average, and strong breadth, i.e. advancers outnumbered decliners. Hong Kong’s most heavily traded stocks were Tencent, which fell -0.23%, AIA, which gained +6.11% on strong financial results and a healthy buyback and dividend policy. Meanwhile, Meituan fell -3.63%, the Bank of China gained +4.91% on strong Southbound Stock Connect buying, and Alibaba fell -1.26%.

Mainland China had a strong day on high volumes, which were 143% of the 1-year average and strong breadth, i.e. advancers outnumbered decliners. The Shanghai Composite closed above 3,100 for the first time since October 2023 after clearing its 200-day moving average last week. Growth stocks led the market higher as small caps had a strong day after lagging large caps year-to-date. There was another very large net buy via Northbound Stock Connect today to the tune of $1.5 billion, following the fourth-largest net buy day ever of $3.1 billion on Friday. Foreign investor China allocations have been very light, though there could be some “window dressing” at the end of the month. One of the two ETFs favored by the National Team traded 1.5 million shares versus Friday’s 1.4 million shares, Thursday’s 664,000m and the 1-year average of just over 1 million.

The Hang Seng and Hang Seng Tech indexes diverged to close +0.54% and -0.13%, respectively, on volume that increased +3.93% from Friday, which is 167% of the 1-year average. 350 stocks advanced while 133 declined. Main Board short sale turnover fell -3.54% from Friday, which is 145% of the 1-year average, as 15% of turnover was short turnover (remember Hong Kong’s short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps outperformed the growth factor and large caps. The top-performing sectors were Real Estate, which gained +4.4%, Financials, which gained +2.34%, and Health Care, which gained +1.34%. Meanwhile, Energy fell -1.73%, Consumer Discretionary, which fell -1.41%, and Materials, which fell -0.70%. The top-performing subsectors were insurance, real estate, and banks. Meanwhile, food & beverage, telecom, and energy were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a net $351 million worth of Hong Kong-listed stocks, including the Bank of China, which was a large net buy, Sense Time, which was a moderate net buy, and Sunac, which was a small net buy. Meanwhile, Meituan was a large net sell and China Mobile was a moderate net sell.

Shanghai, Shenzhen, and the STAR Board gained +0.79%, +2.31%, and +3.18%, respectively, on volume that increased +11.58% from Friday, which is 143% of the 1-year average. 4,267 stocks advanced while 725 declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were real estate +6.39%, tech +2.61% and healthcare +2.22% while energy and utilities were -1.93% and -0.49%. The top-performing subsectors were power generation equipment, real estate, and household products. Meanwhile, precious metals, oil & gas, and land transportation were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $1.5 billion worth of Mainland stocks, including CATL, which was a moderate net buy, Mindray, and LXJM, which were moderate net buys. Meanwhile, Kweichow Moutai was a moderate net sell, and Midea and Cypc were small net sells. CNY and the Asia Dollar Index were basically flat versus the US dollar. Treasury bonds were off. Copper gained while steel was flat.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.25 yesterday

- CNY per EUR 7.75 versus 7.76 yesterday

- Yield on 1-Day Government Bond 1.43% versus 1.40% yesterday

- Yield on 10-Year Government Bond 2.35% versus 2.32% yesterday

- Yield on 10-Year China Development Bank Bond 2.46% versus 2.40% yesterday

- Copper Price +0.41%

- Steel Price unchanged