Rally Catches Its Breath as World Bank Releases 2023 GDP Forecast

3 Min. Read Time

Key News

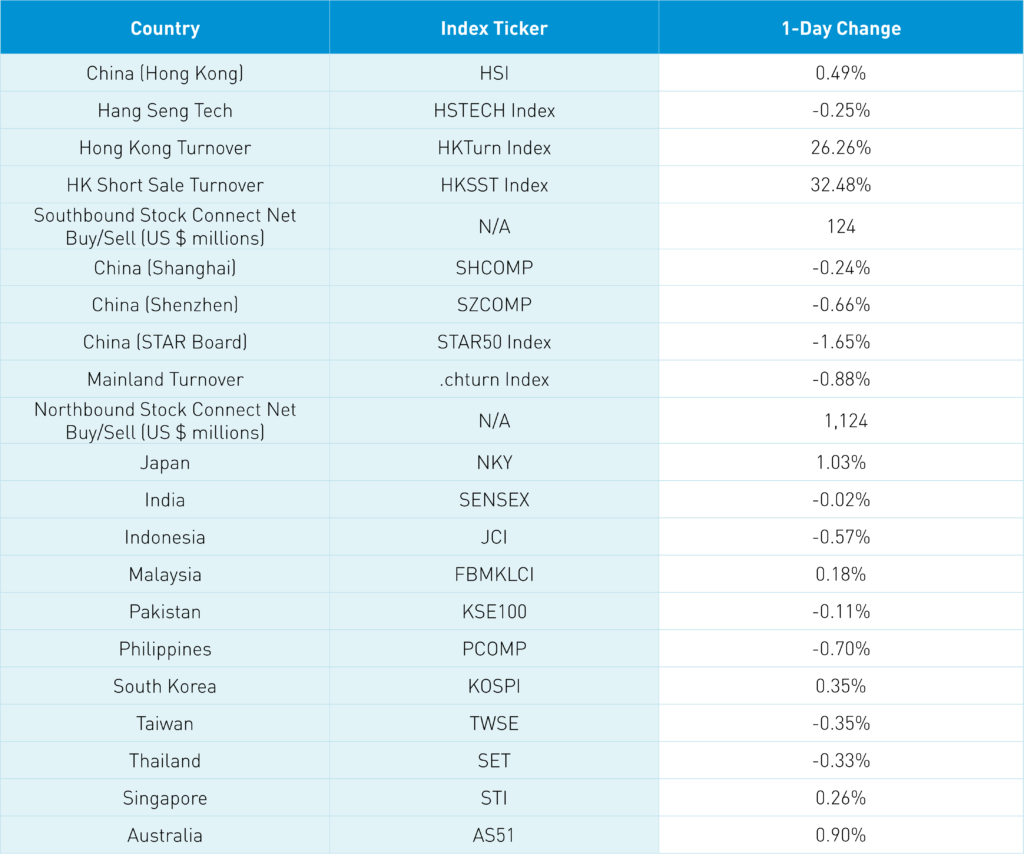

Asian equities were mixed overnight while Japan and South Korea outperformed.

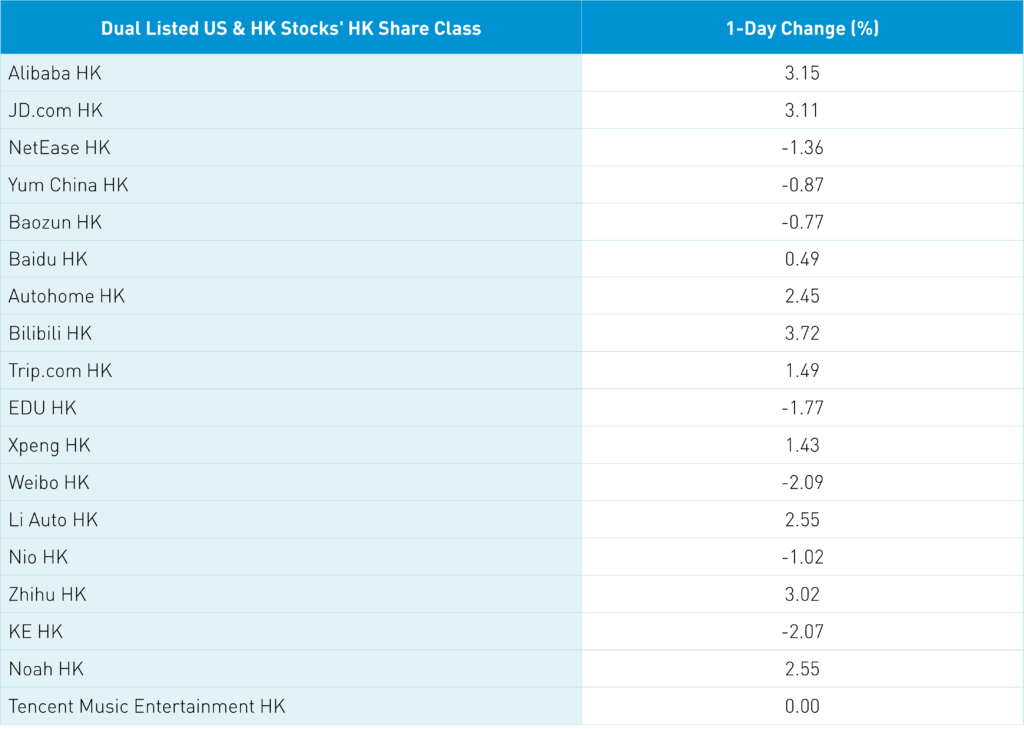

Hong Kong and China eased in afternoon trading though the Hang Seng closed in the green and above the 21k level while the Mainland dipped into negative territory. Hong Kong growth stocks were mixed today as Hong Kong’s most heavily traded by value were Tencent gaining +3.15% as the company continues to buy back stock and announced a push for short videos on WeChat, Alibaba HK gained +3.11% on yesterday's news of its home province support, and Meituan fell -2.52% as several reopening plays were clipped. Hong Kong internet stocks were largely higher led by e-commerce though didn’t gain as much as their US ADRs yesterday which should lead to a small pullback in US trading hours. Macao casinos and Trip.com HK -1.77% were hit with profit taking as we have a bit of profit taking and a buy the rumor – sell the news dynamic.

Mainland investors via Southbound Stock Connect were net buyers of Hong Kong stocks though Tencent, Kuaishou, and Meituan were all net sells. We had the first day in recent memory that Hong Kong short volume increased more than aggregate Hong Kong volume though the total amount of short selling relative to aggregate volume was moderate at 15%. Hong Kong volume was above its 1-year average at 132% while Main Board short turnover was 117% of its 1-year average. Energy was the top sector in both Hong Kong +2.93% and China +3.82% as a cold spell hits China lifting coal stocks in particular. While Mainland stocks pulled back leading to a rally in Chinese Treasuries, foreign investors bought the dip with $1.124 billion of net buying via Northbound Stock Connect. Fairly quiet from a news perspective as the PBOC and CBIRC reiterated their support for the economy. CNY managed a small gain versus the US dollar.

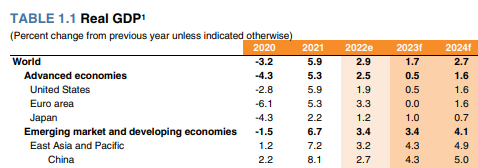

The World Bank provided their GDP forecasts. GDP is neither the stock market nor corporate revenue/net income/EPS. Neither should it be ignored! Do you think most investors are allocated appropriately if these forecasts play out? Me neither. Think about the CPI and interest rate trajectory of these economies. This information and more will be covered in our 2023 China Outlook this Thursday.

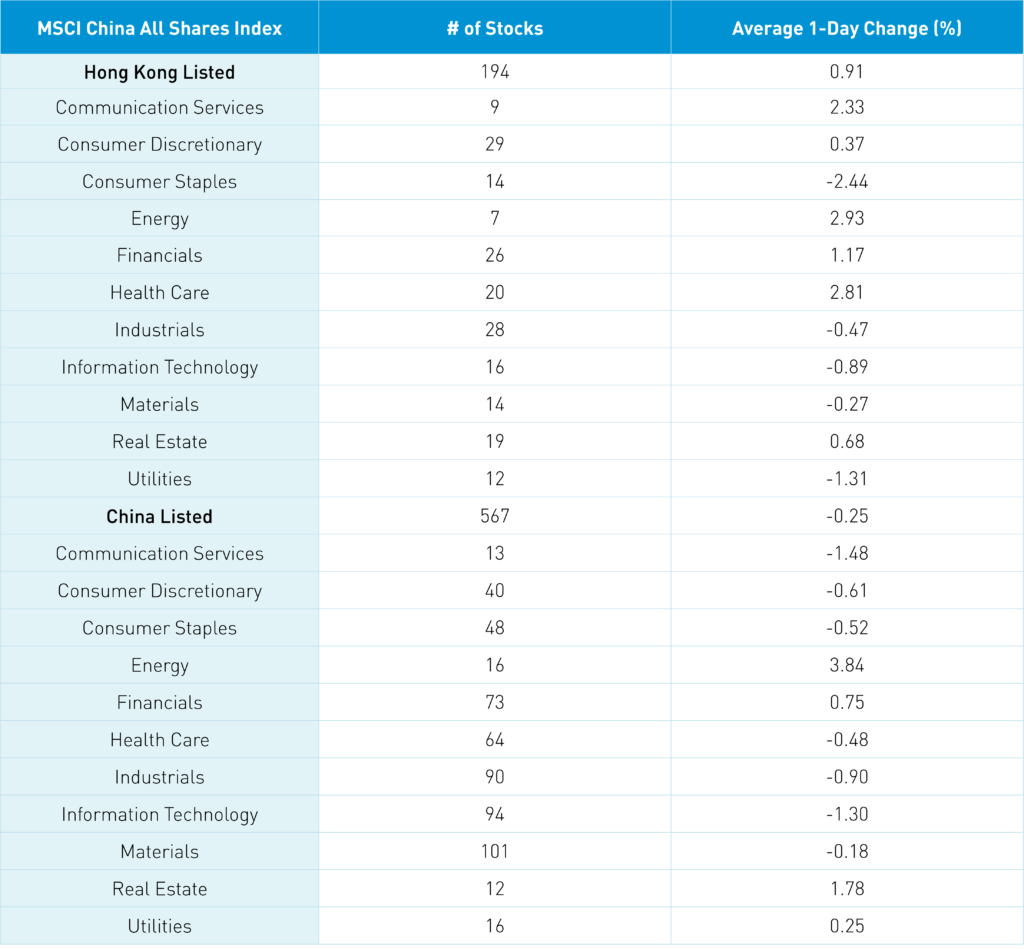

The Hang Seng and Hang Seng Tech diverged +0.49% and -0.25% respectively on volume +26.26% from yesterday which is 132% of the 1-year average. 181 stocks advanced while 310 stocks declined. Main Board short turnover increased +32.4% from yesterday which is 117% of the 1-year average as 15% of turnover was short turnover. Value and growth factors were mixed as large caps outpaced small caps. Top sectors were energy gaining +2.93%, healthcare up +2.8%, and communication closing higher +2.33%, while staples fell -2.44%, utilities closed lower -1.31%, and tech was down -0.89%. Top sub-sectors were food, energy, and software while consumer services, food/beverage/tobacco, and semis were among the worst. Southbound Stock Connect volumes were moderate as Mainland investors bought $124 million of Mainland stocks with Lu Auto a small net buy, Tencent a large net sell, Meituan, Li Auto, and Kuaishou small net sells.

Shanghai, Shenzhen, and STAR Board fell -0.24%, -0.66%, and -1.65% respectively on volume -0.88% from yesterday as 967 stocks advanced while 3,689 stocks declined. Value factors outperformed growth factors as large caps outpaced small caps. Top sectors were energy gaining +3.84%, real estate up +1.78%, and financials closing higher +0.75% while communication fell -1.47%, tech was down -1.3%, and industrials closed lower -0.89%. Top sub-sectors were coal, insurance, and gas while software, chemical, and internet were among the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $1.124 billion of Mainland stocks. CNY gained +0.11% versus the US dollar closing at 6.77, Treasury bonds rallied, and Shanghai copper gained +1.32%.

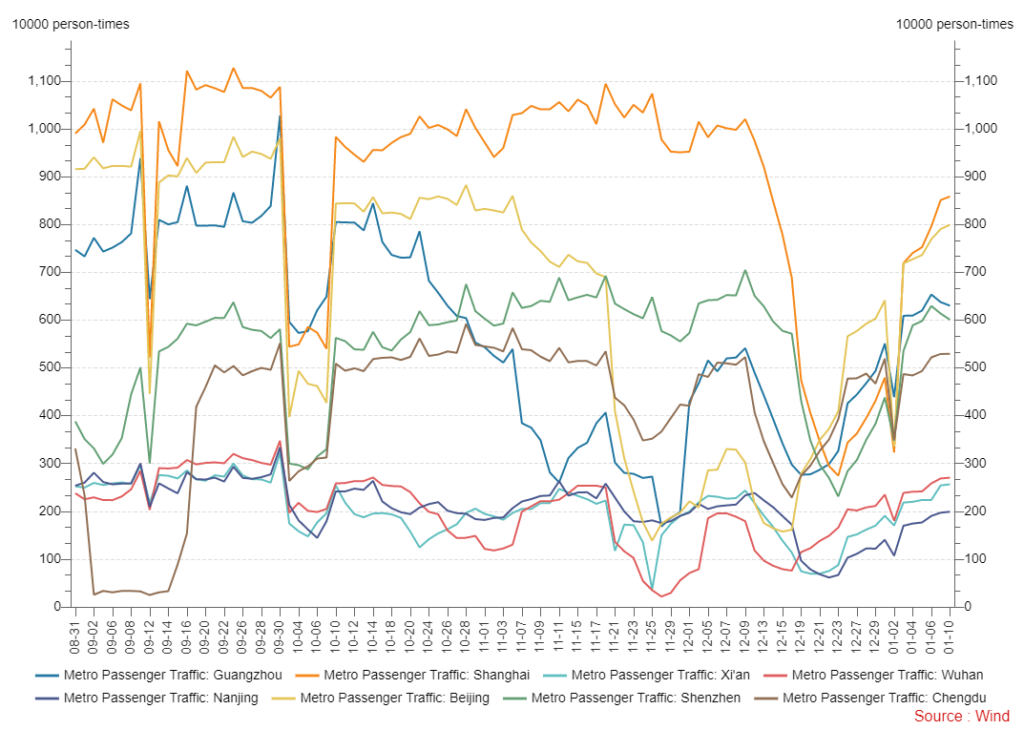

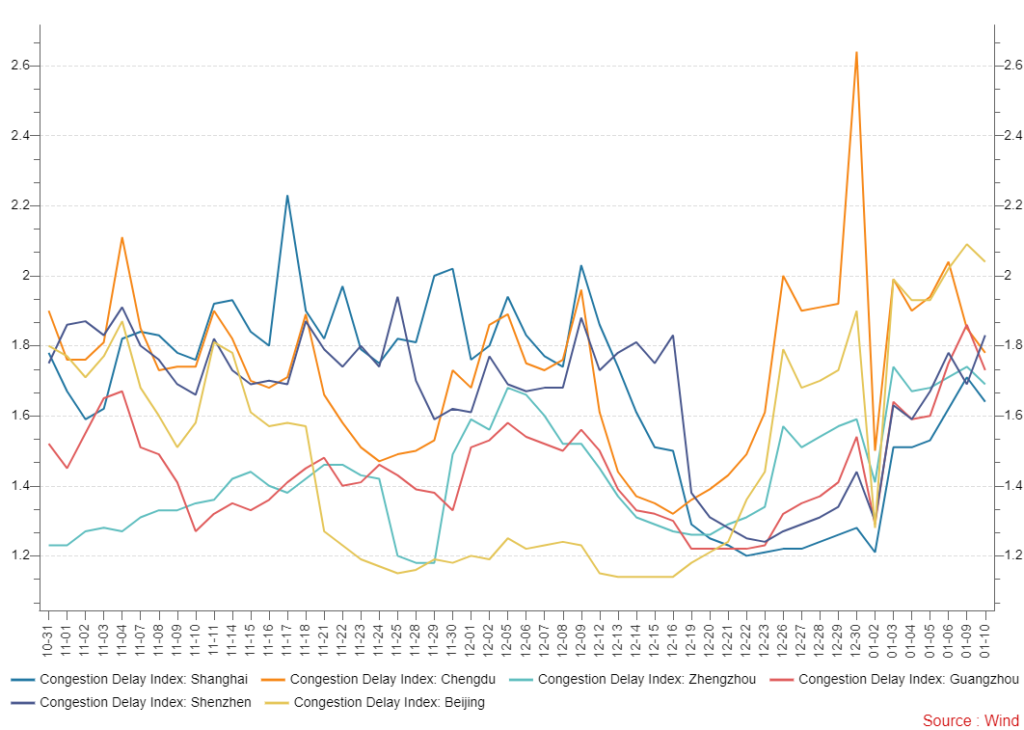

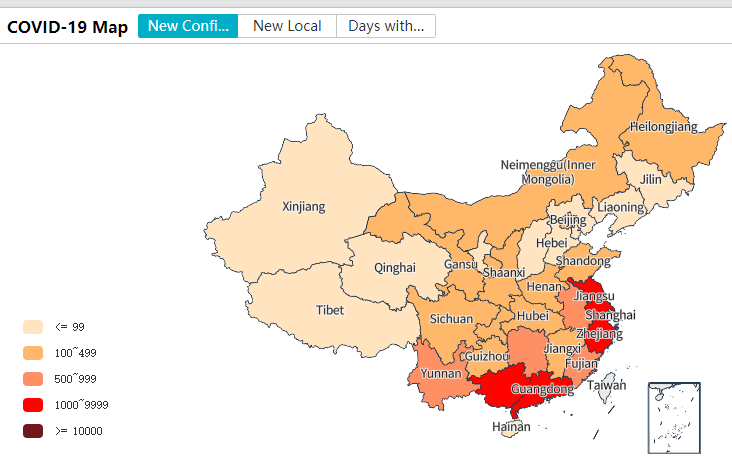

Major Chinese City Mobility Tracker

Trajectory is positive though several provinces are clearly still in the thick of it.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.77 versus 6.78 yesterday

- CNY per EUR 7.27 versus 7.28 yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 2.99% versus 3.01% yesterday

- Copper Price +1.32% overnight