MSCI Announces Index Review Results, Week in Review

2 Min. Read Time

Week in Review

- It was a choppy week of trading for Asian equities as China released lower-than-expected imports, exports, loan growth, and CPI figures while US inflation showed further cooling in April.

- Automaker Li Auto and car dealer Autohome both released positive results for the first quarter this week, as total sales in China are rebounding, up over +50% year-over-year.

- E-Commerce giant JD.com kicked off internet earnings season with a clean beat on first quarter revenue.

- Value stocks outperformed early in the week while growth stocks made a comeback as the week ended, including last night.

Friday’s Key News

Asian equities were mixed but mostly lower overnight.

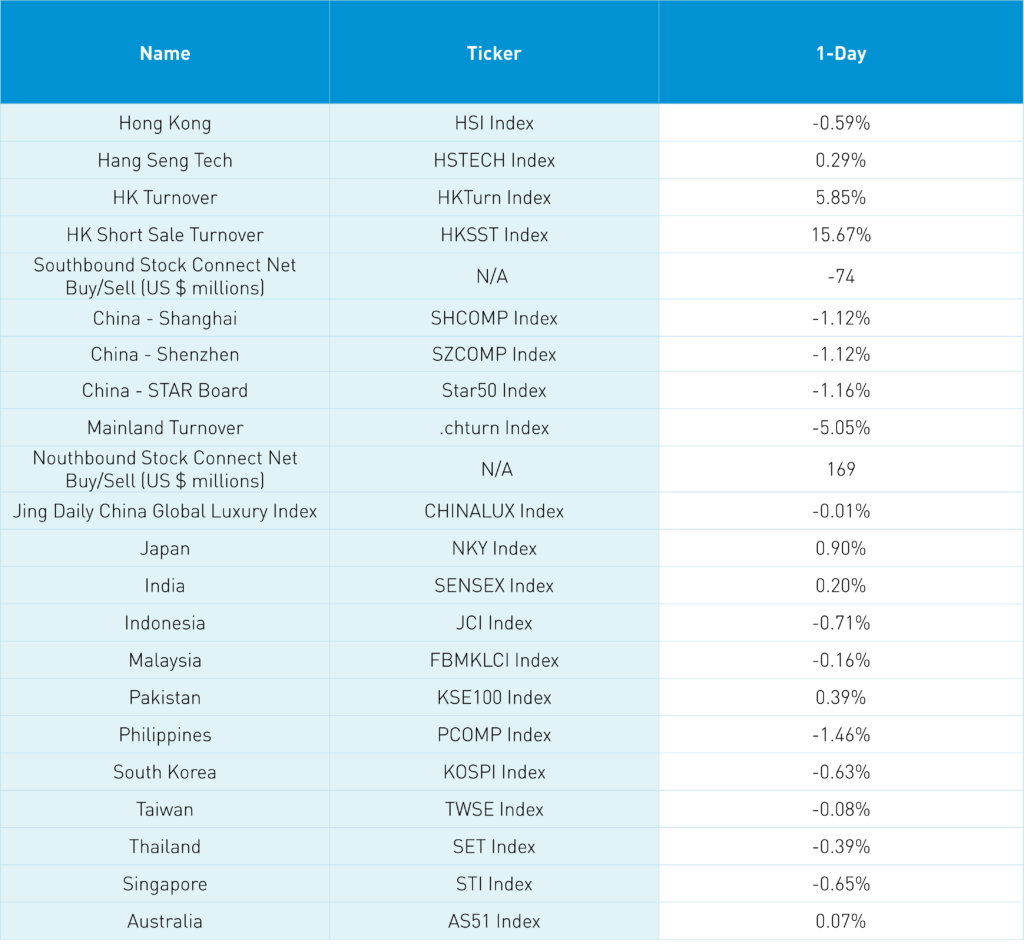

Mainland markets were lower because of slow loan growth reported yesterday. China’s recovery may need further policy support to keep it going, which should be viewed as a positive.

US National Security Adviser Jake Sullivan met with China’s foreign minister Qin Gang for “substantive and constructive” meetings. This is another green shoot for US-China relations. Hopefully, Biden and Xi will get on the phone relatively soon.

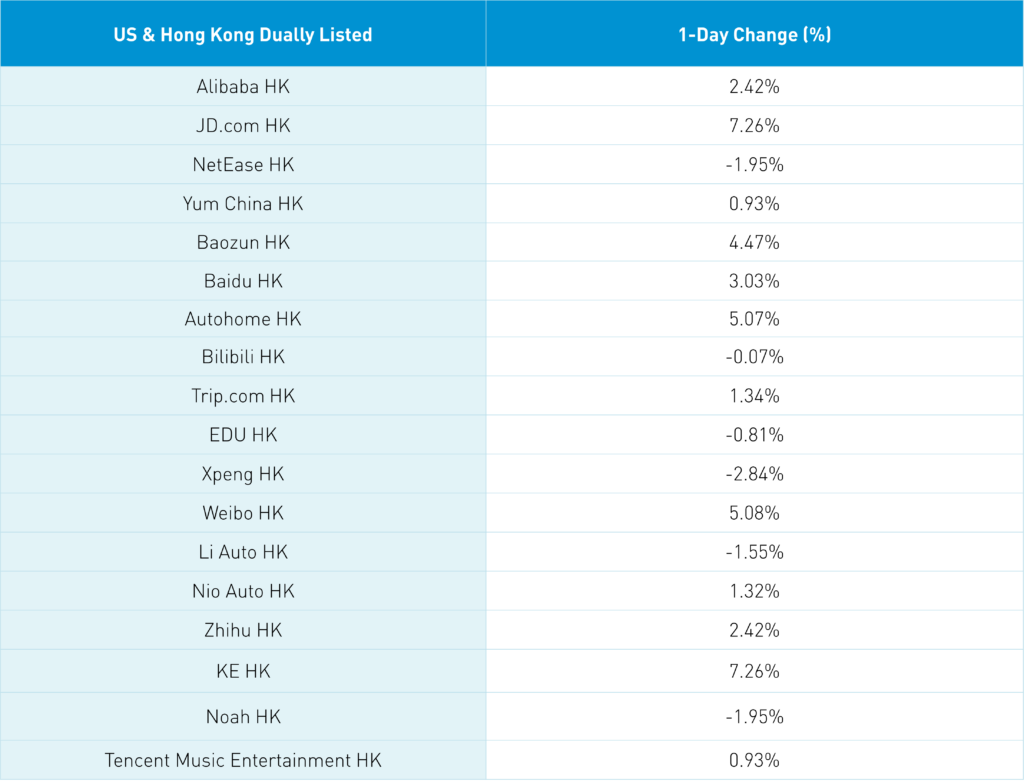

After yesterday’s US market close, MSCI released their pro forma for the month-end Semi-Annual Index Review. Trip.com will see its holding in MSCI indices migrate to their Hong Kong share class from their US listing. This is unrelated to geopolitical news, but entirely related to MSCI’s index methodology ,which always prefers a local share class versus a foreign listing, i.e. a US ADR. Trip.com’s Hong Kong share class has an average daily value of trading of $31 million versus $141 million in the US. Trip.com’s Hong Kong share class’ value of trading is only 23% of the US listing, though I suspect that will increase fairly dramatically in the future. Meanwhile, China’s weight in MSCI Emerging Markets will increase to 32.7% from 32.2% based on 53 additions and 13 deletions driven by further additions to Northbound Stock Connect, which is a pre-requisite for MSCI index inclusion. MSCI Emerging Markets will have 1,378 stocks, which includes 756 Chinese stocks. A surprise addition is JD Logistics, though Full Truck Alliance was not added as its underlying shares are not available for trading. It might time for a Hong Kong listing! The US’ weight in the All Country World Index (ACWI) is now 58.8%. Alibaba is seeing a significant float increase, which should lead to approximately 100 million shares having to be bought. Tencent is seeing a small float decrease.

China-based semiconductor manufacturer SMIC gave positive guidance that Q2 sales would likely increase by up to 7%. This is likely as US export restrictions begin to bite, which is an opportunity for local players. The State-Owned Assets Supervision and Administration Commission (SASAC) issued new guidance for SOEs. The guidance includes more incentives to pursue emerging industries and technologies including artificial intelligence and semiconductors.

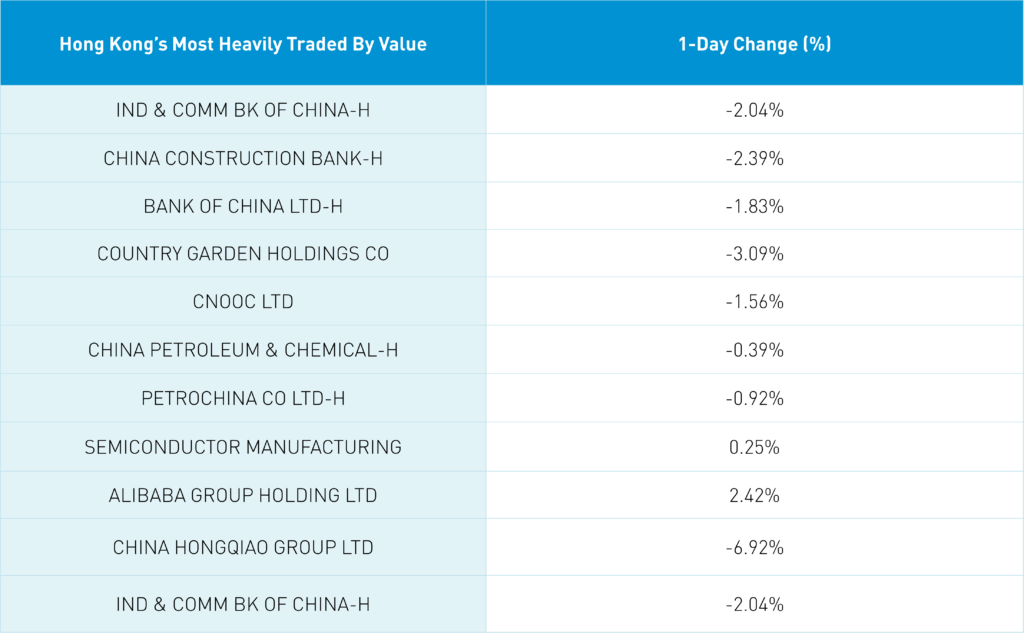

The Hang Seng and Hang Seng Tech indexes diverged to close -0.59% and 0.29%, respectively, on volume that increased +6% from yesterday. Mainland investors sold a net $74 million worth of Hong Kong stocks. The top-performing sectors were Information Technology, Consumer Discretionary, and Consumer Staples. Meanwhile, the worst-performing sectors included Materials and Industrials.

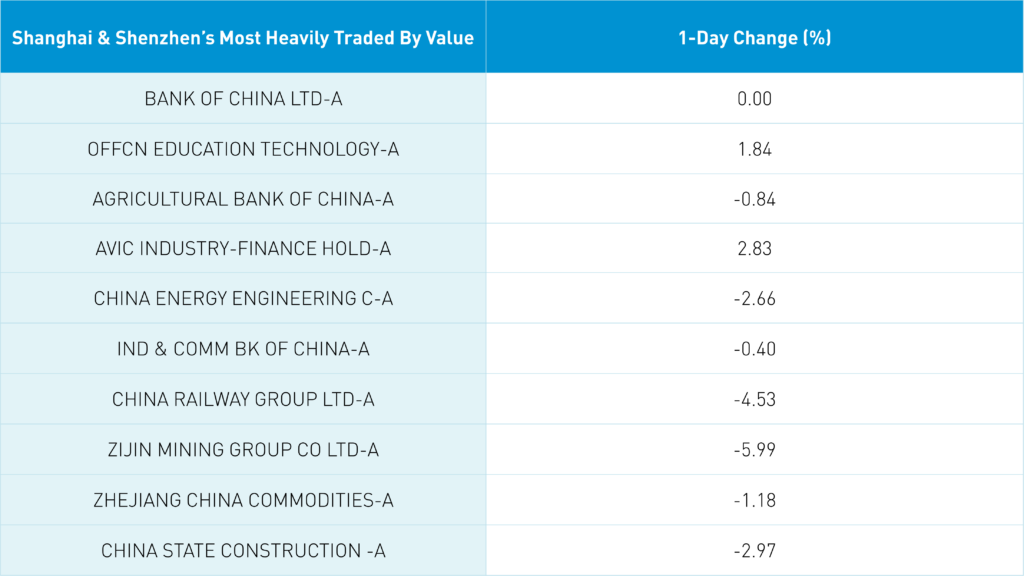

Shanghai, Shenzhen, and the STAR Board closed lower by -1.12%, -1.12%, and -1.16%, respectively, on volume that decreased -5% from yesterday. Foreign investors purchased a net $169 million worth of Mainland stocks. The top-performing sectors were Utilities, Health Care, and Consumer Staples. Meanwhile, the worst-performing sectors were Communication Services, Materials, and Industrials.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.95 versus 6.95 yesterday

- CNY per EUR 7.56 versus 7.59 yesterday

- Yield on 1-Day Government Bond 1.37% versus 1.37% yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.87% versus 2.87% yesterday

- Copper Price -2.95% overnight