Biden-Xi Meeting, JD.com & Tencent Earnings Send Hong Kong Higher

3 Min. Read Time

Key News

Asian equities had a strong day following the soft US CPI print yesterday, sending the US dollar lower and risk assets higher as Hong Kong outperformed the region.

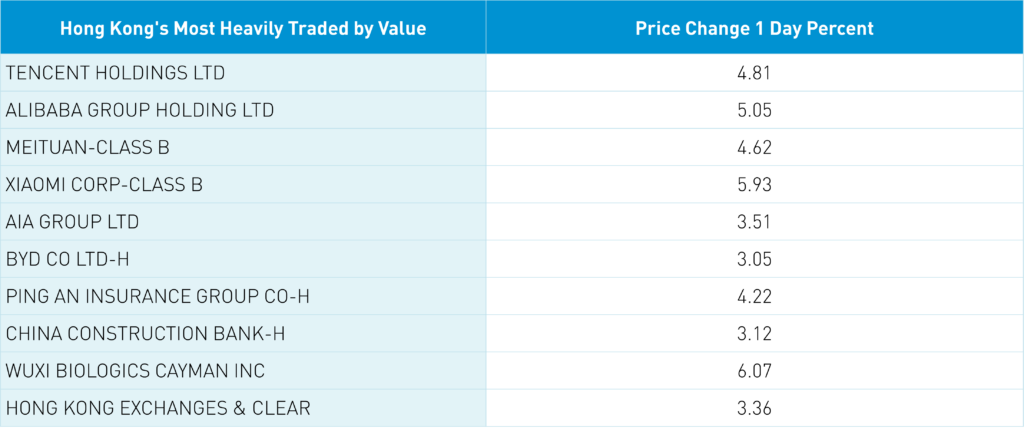

Today is evidence of how interconnected the world we live in is. Hong Kong and Mainland China rose on strong volumes, with Hong Kong posting 124% of its 1-year average volumes and Mainland China posting 113% of its 1-year average volumes amid strong breadth. The Hang Seng closed above 18,000 for the first time since October 12th. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +4.81%, Alibaba, which gained +5.05%, and Meituan, which gained +4.62%.

Additional Mainland China and Hong Kong catalysts include yesterday’s announcement of RMB 1 trillion for “urban village restoration and subsidized housing projects” and the People's Bank of China (PBOC), China's central bank, injecting the largest amount of liquidity into the financial system since December 2016 via its medium-term lending facility. There has been a fair amount of chatter that the move is in advance of a bank reserve requirement ratio (RRR) cut, which would free up more of banks’ balance sheets for lending.

October economic data was mixed but better than expected as retail sales were up +7.6% year-over-year (YoY) versus expectations of 7.0% and September’s 5.5%, Industrial Production was up +4.1% YoY versus expectations of 4.1% and September's 4.5%. Within the Retail sales data, online retail sales increased +11.2% year-to-date, as 26.7% of the total retail sales were consumer goods sold online. Autos stood out for their strong sales. Real estate data was off, as expected.

The meeting between Presidents Biden and Xi will include Treasury Secretary Yellen at 2 pm EST here in San Francisco, with a 7 pm EST press conference. Climate change appears to be an area of mutual interest, though restricting chemical inputs for fentanyl, a Boeing 737 MAX China approval, and China agricultural purchases also seem feasible.

All of this occurred before both Tencent and JD.com reported Q3 financial results after the Hong Kong close that beat analyst expectations. Tencent revenues increased +10% YoY to RMB 154.6B ($21.5B) versus expectations of RMB 154.8B, adjusted net income increased +39% to RMB 44.9B ($6.3B) versus expectations of RMB 39.98B, and adjusted EPS was RMB 4.65 versus expectations of RMB 4.13. Free cash increased +85% YoY to RMB 51.1B as the company bought 47.5 million shares in Q3.

JD.com revenue increased +1.7% YoY to RMB 247.7 ($34B) versus expectations of RMB 246B, adjusted net income increased slightly to RMB 10.6B ($1.5B) versus expectations of RMB 9.24B, and adjusted EPS was RMB 6.70 ($0.92) versus expectations of RMB 5.87. JD also noted a strong uptick in free cash flow, reporting RMB 39.4B ($5.4B) versus RMB 6.27B.

Both JD.com and Tencent demonstrated their management teams' prowess during a challenging environment.

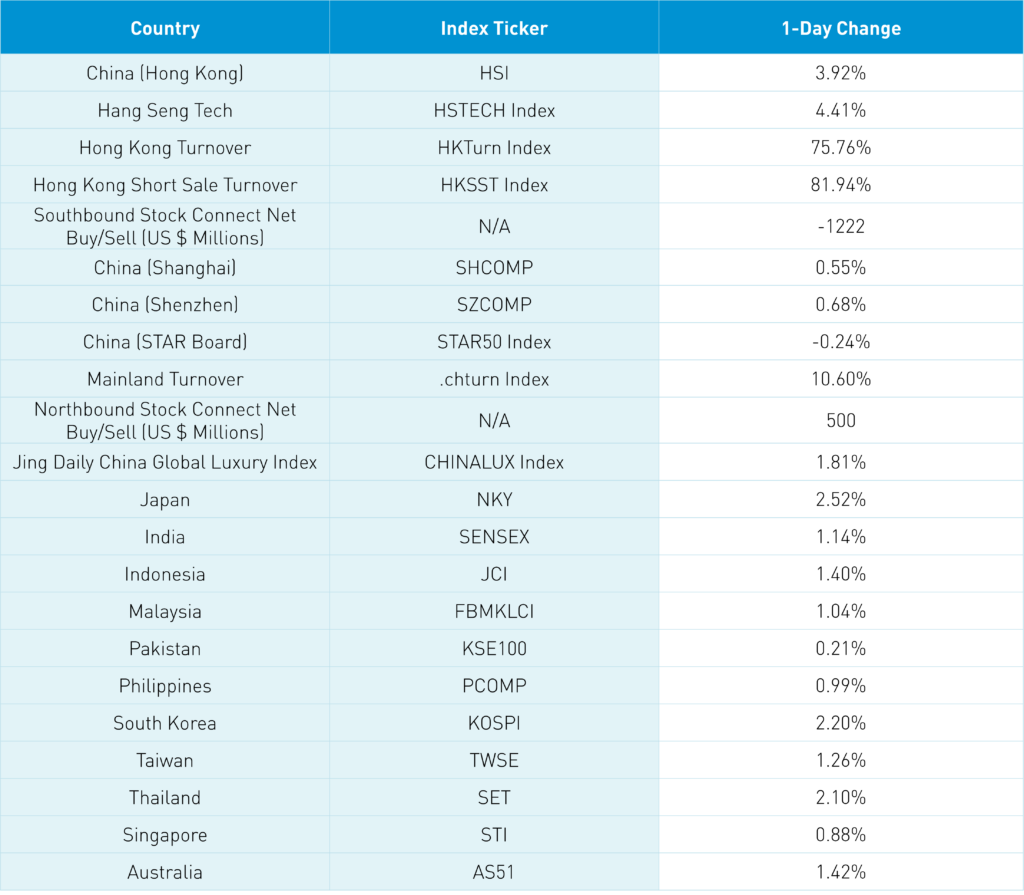

The only negative today was the big net sale of the Hong Kong Tracker ETF and Tencent from Mainland investors via Southbound Stock Connect. Their behavior is hard to explain, though their sale of Tencent appears poorly timed. Foreign investors bought a net $500 million worth of Mainland growth stocks via Northbound Stock Connect. All this good news is occurring while China allocations are at all-time lows. Alibaba reports tomorrow after the Hong Kong close.

MSCI released the pro-forma for its month-end Semi-Annual Index Review (SAIR). There was nothing major to report as Asia’s percentage of Emerging Markets is now 79%, with China at 29.5% (765 stocks), India at 16.3% (131 stocks), Taiwan at 15.1% (90 stocks), and Korea at 12.4% (103 stocks). The US is 61.4% of the All-Country World Index.

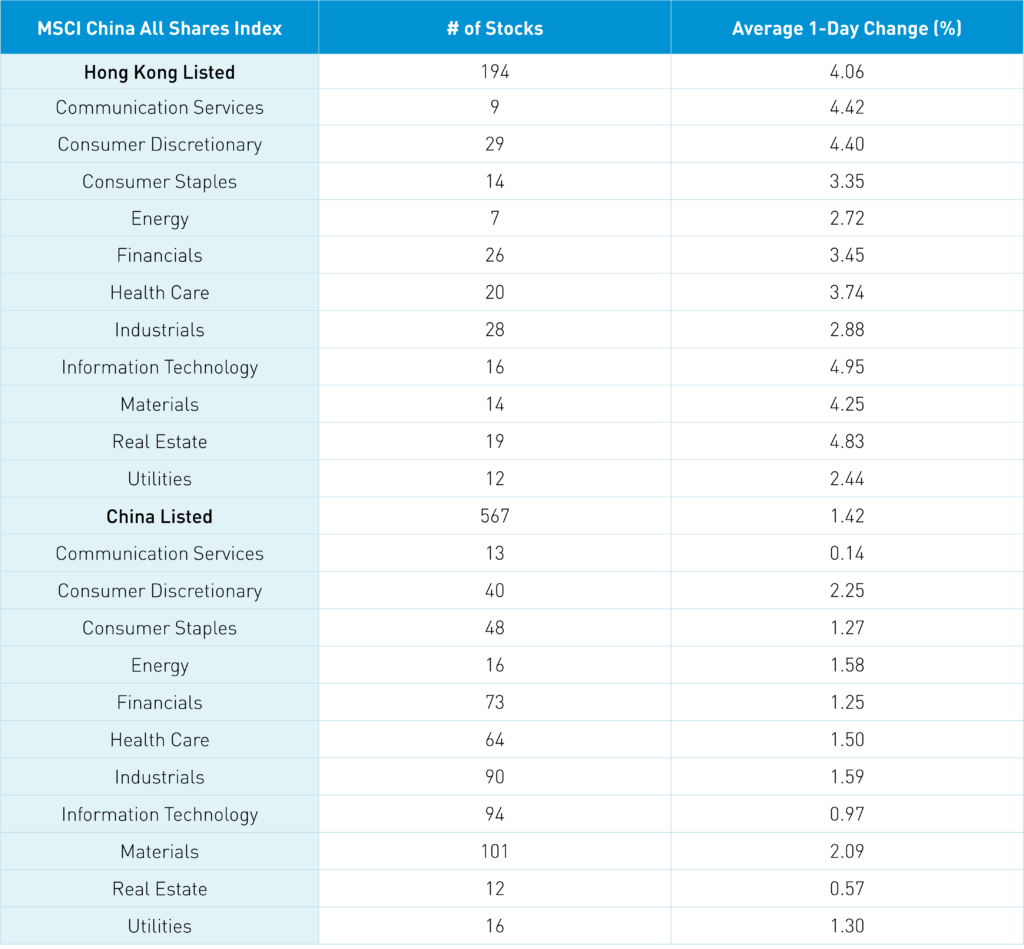

The Hang Seng and Hang Seng Tech indexes gained +3.92% and +4.41%, respectively, on volume that increased +75.76% from yesterday, which is 123% of the 1-year average. 453 stocks advanced, while 48 declined. Main Board short turnover increased by +81.94% from yesterday, which is 135% of the 1-year average, as 18% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outpaced the value factor and large caps. All sectors were higher, led by technology, which gained +4.95%, real estate, which gained +4.83%, and communication services, which gained +4.42%. All subsectors were positive, as retail, technical hardware, and software were the top performers. Southbound Stock Connect volumes were high as Mainland investors sold a healthy net -$1.22 billion worth of Hong Kong stocks and ETFs, with Kuiashou a small net buy while the Hong Kong Tracker ETF and Tencent had very large net sells.

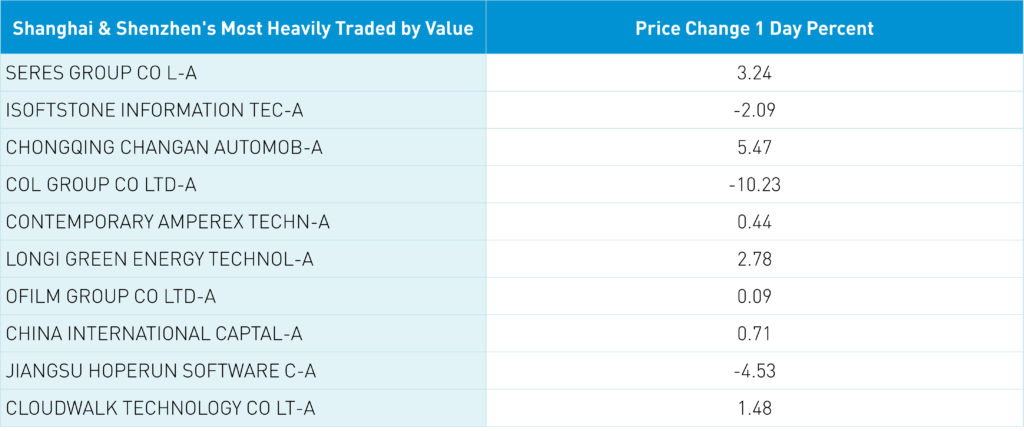

Shanghai, Shenzhen, and the STAR closed diverged to close +0.55%, +0.68%, and -0.24%, respectively, on volume increased +10.6% from yesterday, which is 113% of the 1-year average. 3,148 stocks advanced, while 1,607 declined. The growth factor and large caps outperformed the value factor and small caps. All sectors were positive, led by consumer discretionary, which gained +2.15%, materials, which gained +2%, and industrials, which gained +1.5%. The top-performing subsectors were motorcycles, auto parts, and power generation equipment. Meanwhile, internet, cultural media, and aerospace/military were among the worst-performing. Northbound Stock Connect volumes were high as foreign investors bought a net $500 million worth of Mainland stocks, including Ganfeng Lithium, LONGi Green Technology, Kweichow Moutai, BYD, China Merchants Bank, Cypc, Tianqi Lithium, and Mindray. CNY and the Asia Dollar Index had a very strong day versus the US dollar. The Treasury curve steepened while copper gained and steel were off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.29 yesterday

- CNY per EUR 7.86 versus 7.82 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.65% yesterday

- Yield on 10-Year China Development Bank Bond 2.73% versus 2.73% yesterday

- Copper Price +0.27% overnight

- Steel Price -0.41% overnight