PBOC Steps Up Real Estate Support, Game Over for Gaming Officials as Tencent & NetEase Rally

4 Min. Read Time

Key News

Asian equities followed US stocks south with Apple’s downgrade. Investors' slow realization the company’s growth rate has slowed weighed on growth/tech stocks regionally and Apple suppliers, as Taiwan and South Korea underperformed.

Several interesting items are occurring today. Larry McDonald, a macro strategist and author of the Bear Traps Report, noted Apple’s market cap is 15X larger than Alibaba’s market cap. A similar and timely comparison could be made for Tesla’s market cap of $789 billion versus BYD’s $78 billion despite the latter unseating the former yesterday as the global NEV (hybrid and pure EV) leader. BYD’s Hong Kong and Mainland China shares gained +0.57% and +0.30% as the EV ecosystem sold off on concerns of price wars. Yes, there is EV competition, though an element of these gains comes from gas automakers.

The PBOC made a very explicit move to support the real estate market with RMB 350B ($9B) of pledged supplementary lending (PSL, a fancy way of saying a loan backed by collateral) to three policy banks in December for the first time since November 2022. The banks will make loans to support “China’s urban village redevelopment and affordable housing programs to shore up its struggling property market,” according to Reuters. Surprisingly, the move had little reaction in real estate stocks in Hong Kong and Mainland China, though the stocks were apt to suffer from new stock issuance. We continue to advocate investors ignore the stocks and examine the bonds, which have stabilized and, in some cases, actually rallied as the companies restructure their debt.

Coincidentally, distressed developer CIFI Holdings announced proposed restructuring terms for its offshore US dollar debt today. I can’t get anyone to even glance at the Asia high yield US dollar bond market despite a yield nearly 2X the US high yield. Widely followed Mainland financial outlet China Securities Journal highlighted an economist who believes 2023 interest rate and bank reserve requirement ratios will be cut in 2024. Not exactly burying the headline!

The Hong Kong Tracker ETF was today’s most heavily traded by value as mainland investors bought HK $4.22 billion of the ETF. This is the first time I can recall an ETF being the most heavily traded security in Hong Kong. Market makers had to create ETF shares, which led to a spike in short turnover as they hedged themselves. Tencent and NetEase gained +1.35% and +0.96%, respectively, after yesterday’s news of the firing of the head online gaming official following last Friday’s proposed online game spending rules. The importance of this is it proves the Chinese government is a big bureaucracy where one hand sometimes doesn’t know what the other hand is doing and not some 007 James Bond as the media would have us think and also reinforces President Xi’s APEC speech to US business executives on changing foreign investor and corporate sentiment. The firing is a clear signal that a mistake was made by the official who failed to impart the new pro-investor/corporate-friendly directive.

The Apple news weighed on suppliers like Hong Kong-listed Sunny Optical -3.84% and Mainland-listed GoerTek -3.37%. Yesterday’s news of US government pressure on ASML to limit sales to Chinese companies weighed on semiconductors and tech plays. Tencent continues to buy back stock with 3.36 million shares bought following yesterday’s 3.38 million, 12/29’s 3.42 million, 12/28 3.45 million, etc. Hong Kong internet plays were off, with Alibaba -1.87%, Meitan -1.76%, JD.com -3.19%, and Baidu -2.43% for no reason. Baidu’s fall is surprising as it calls off its purchase of JOYY, which will bolster its cash reserves. Mainland media noted seventeen internet companies and Shanghai Market Supervision will work together to ensure adherence to rules. Mainland China was off despite foreign buying via Northbound Stock Connect and the launch of several mainland equity ETFs focused on the fifty largest Mainland stocks.

Yesterday, South Korea’s President announced a plan to scrap capital gains tax following a ban on short selling in advance of their election later this year. The moves have worked, which I can’t compare to efforts by China’s government to get investors back into the markets. Psychological moves such as buying stocks and ETFs from their sovereign wealth fund have done little to adjust investor sentiment. Hong Kong’s stamp tax was cut, but that’s a frictional cost enhancement and arguably not a catalyst. Companies' buybacks and dividends will have an effect as Tencent and Alibaba vie to become the most shareholder-friendly companies, with many others following suit. China’s economy is coming back, though incrementally. Ultimately, restoring investor confidence is key, which will take time, though there are moves that would have a direct impact, as evidenced by South Korea’s moves.

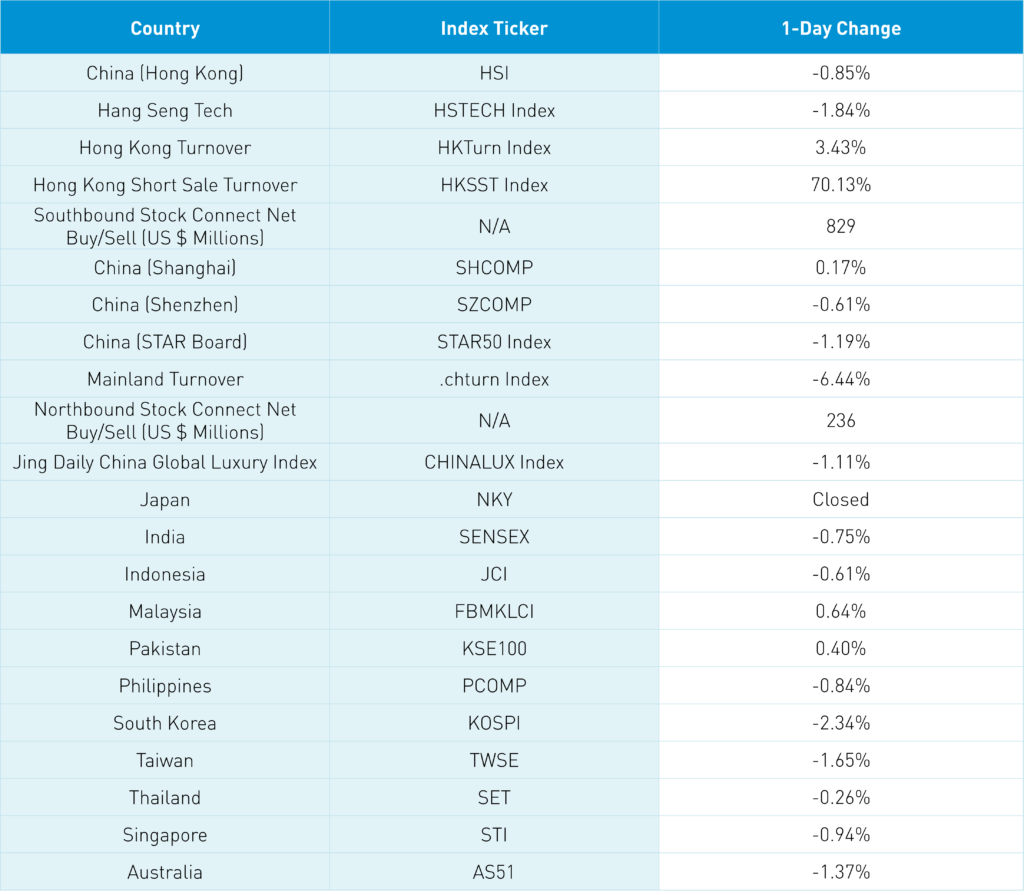

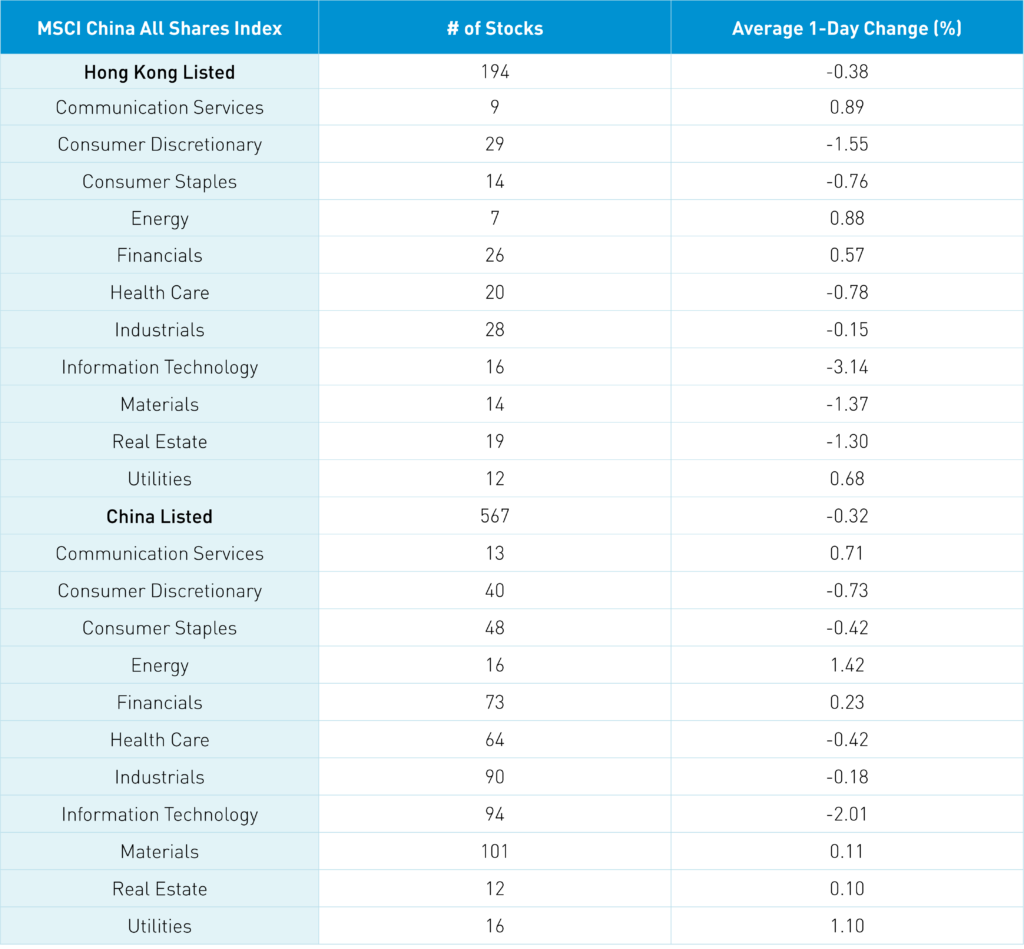

The Hang Seng and Hang Seng Tracker fell –0.85% and -1.84% on volume +3.43% from yesterday, which is 75.9% of the 1-year average. 145 stocks advanced, while 316 declined. Main Board short turnover increased by +70.13% from yesterday, which is 97% of the 1-year average, as 22% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed”/fell less than the growth factor and small caps. The top sectors were communication +0.89%, energy +0.88%, and utilities +0.68%, while tech -3.14%, discretionary -1.55%, and materials -1.37%. The top sub-sectors were software, utilities, and energy, while technical hardware, semis, and consumer durables were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $829 million of Hong Kong stocks and ETFs, with the Hong Kong Tracker ETF seeing a large net inflow, the Hang Seng China Enterprise ETF, and the Hang Seng Tech ETF seeing moderate net inflow while Great Wall Motor and SMIC had small net outflow.

Shanghai, Shenzhen, and STAR Board were mixed +0.17%, -0.61%, and -1.19% on volume -6.44% from yesterday, which is 85% of the 1-year average. 1,872 stocks advanced, while 2,947 declined. The value factor and large caps “outperformed”/fell less than the growth factor and small caps. The top sectors were energy +1.42%, utilities +1.1%, and communication +0.71%, while tech -2.01%, discretionary -0.73%, and staples -0.42%. The top sub-sectors were coal, ports, and marine, while electronic components, software, and semis were the worst. Northbound Stock Connect volumes were light/moderate as foreign investors bought $236 million of Mainland stocks Changan Auto, Midea, and Agriculture Bank moderate net buys, while CATL, Longi Green Energy, and iFlytek were moderate net sells.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.14 versus 7.14 yesterday

- CNY per EUR 7.80 versus 7.83 yesterday

- Yield on 10-Year Government Bond 2.55% versus 2.56% yesterday

- Yield on 10-Year China Development Bank Bond 2.72% versus 2.72% yesterday

- Copper Price -0.29%

- Steel Price +0.47%