Hong Kong Outperforms Mainland, Evergrande Liquidation

4 Min. Read Time

Key News

Asia equities were largely higher as Hong Kong outperformed Mainland China, despite increased tensions in the Middle East.

There was an interesting and stark divergence between Hong Kong, which is predominantly foreign-owned, and Mainland China, which is predominantly owned by local investors, overnight. The former posted gains and the latter fell.

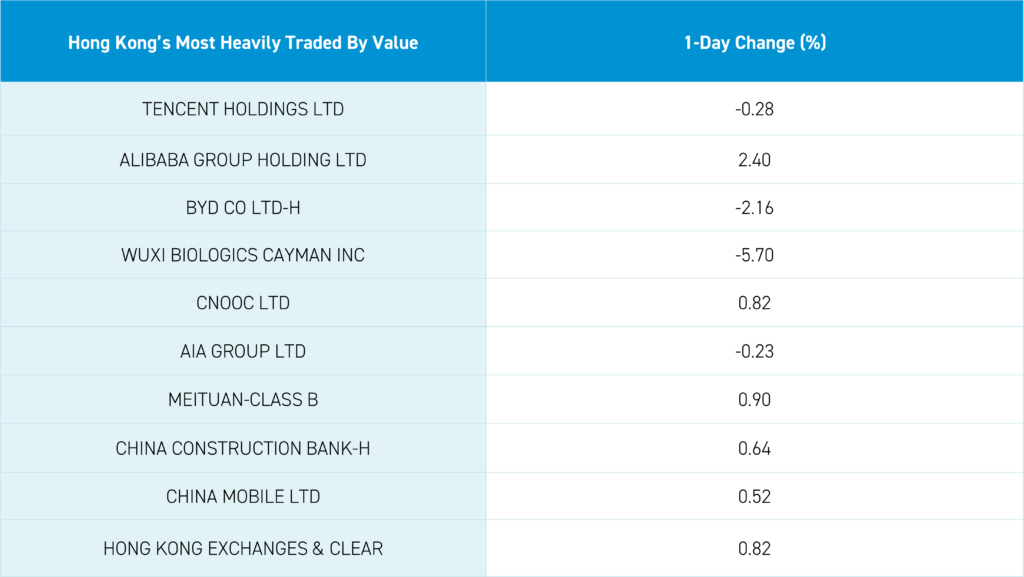

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.28%, Alibaba, which gained +2.4% as investors cheered Jack Ma and Joe Tsai’s stock purchase, BYD, which fell -2.16%, though, after the close, the company reported preliminary 2023 net income between RMB 29 billion to 31 billion, which up is +75% to +87% year-over-year, though missed analyst estimate of RMB 31 billion, Wuxi Biologics, which fell -5.7% despite the company challenging the US House Select Committee’s assertions of military links, and energy giant CNOOC, which gained +0.82% on Middle East tensions.

Based on SEC 13F filings, my calculations bring US investors' loss on the widely respected Wuxi AppTec since the House Committee announcement to $1.1 billion.

The Hong Kong High Court rejected Evergrande’s petition for more time as Judge Chen Jingfen deemed the company insolvent and failed to find an agreement from offshore creditors, who are owed $2 billion. Therefore, “an independent liquidator can take control of the company”. How the Hong Kong court decision will affect the $300 billion worth of onshore debt remains unknown. However, I suspect the company will finish projects to fulfill its obligations to property buyers.

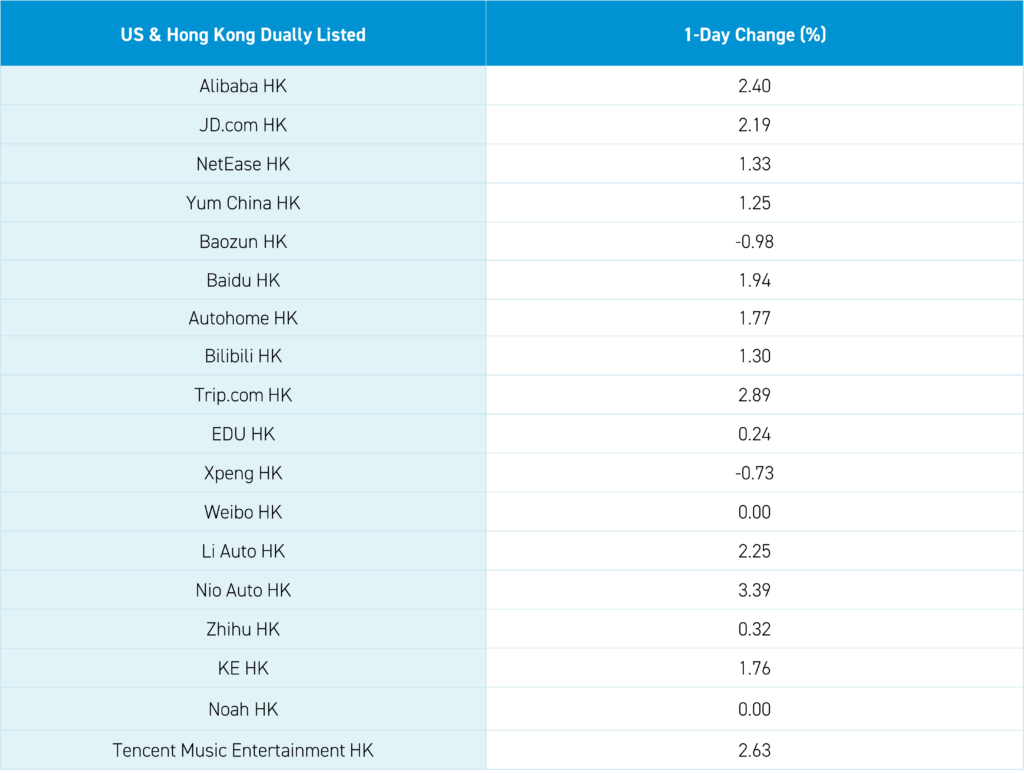

National Security Advisor Jake Sullivan met with Foreign Minister Wang Yi, which could lead to Biden-Xi conference call this spring. Trip.com gained +3% as China waives more countries’ visa requirements with Thailand coming on board. Vice Premier He Lifeng called for more support for the stock market after the close. According to Reuters, he stated that “Government departments should step up support for high-quality listed firms to boost confidence and stabilize capital markets.”

Mainland China was off as the “old economy” (i.e. SOEs, large-caps, financials, manufacturers) Shanghai Composite fell -0.92% while the “new economy” (i.e. private companies, mid-caps, technology) Shenzhen Component fell -2.42%. Shanghai benefited from a policy preventing large shareholders from lending their shares to short sellers and calling for more SOE buybacks and dividends. There was also discussion of a merger between three state-linked asset managers.

Mainland media noted the Biden Administration's inquiry into US cloud computing providers, offering the Chips Act’s third monetary outlay to Intel and Taiwan Semiconductor Manufacturing (TSMC), which might explain the weakness in technology and growth stocks on the Mainland overnight. The move will likely smother the China cloud businesses of Amazon, Microsoft, and Google.

Overnight, there was some industry news on the 2023 struggles of actively-managed mutual funds in China. Meanwhile, fixed income, money market funds, and ETFs gained market share.

January Industrial profits increased +16.8% year-over-year (YoY) versus December’s +29.5% YoY, though the release did not appear to be a market mover. PMIs will be released tomorrow night.

One well-respected Mainland equity strategist called for a more forceful fiscal policy to support the stock market. The economy is clearly improving, though slowly and incrementally, which explains the lack of a policy bazooka. With that said, the Mainland’s stock market performance shows investors are looking for more.

CNBC’s interview with Nikki Haley this morning did not include a mention of China, as domestic issues and foreign crises take center stage. The distraction technique of talking about China instead of real issues is no longer working. Maybe this China narrative is getting a little long in the tooth? A Mainland media source reported that Egypt and Qatar have negotiated an Israel-Palestine, two-month ceasefire that will occur in two weeks. I am not seeing this elsewhere but figured that I would share.

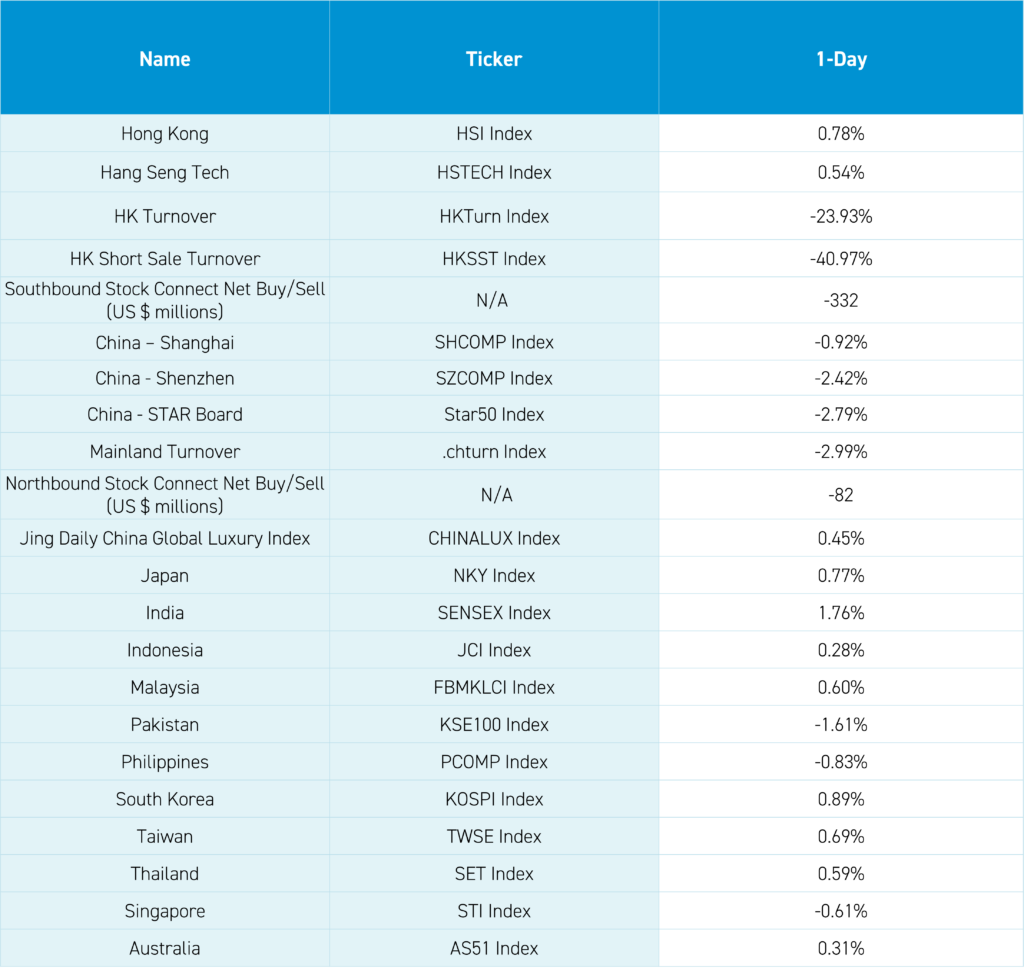

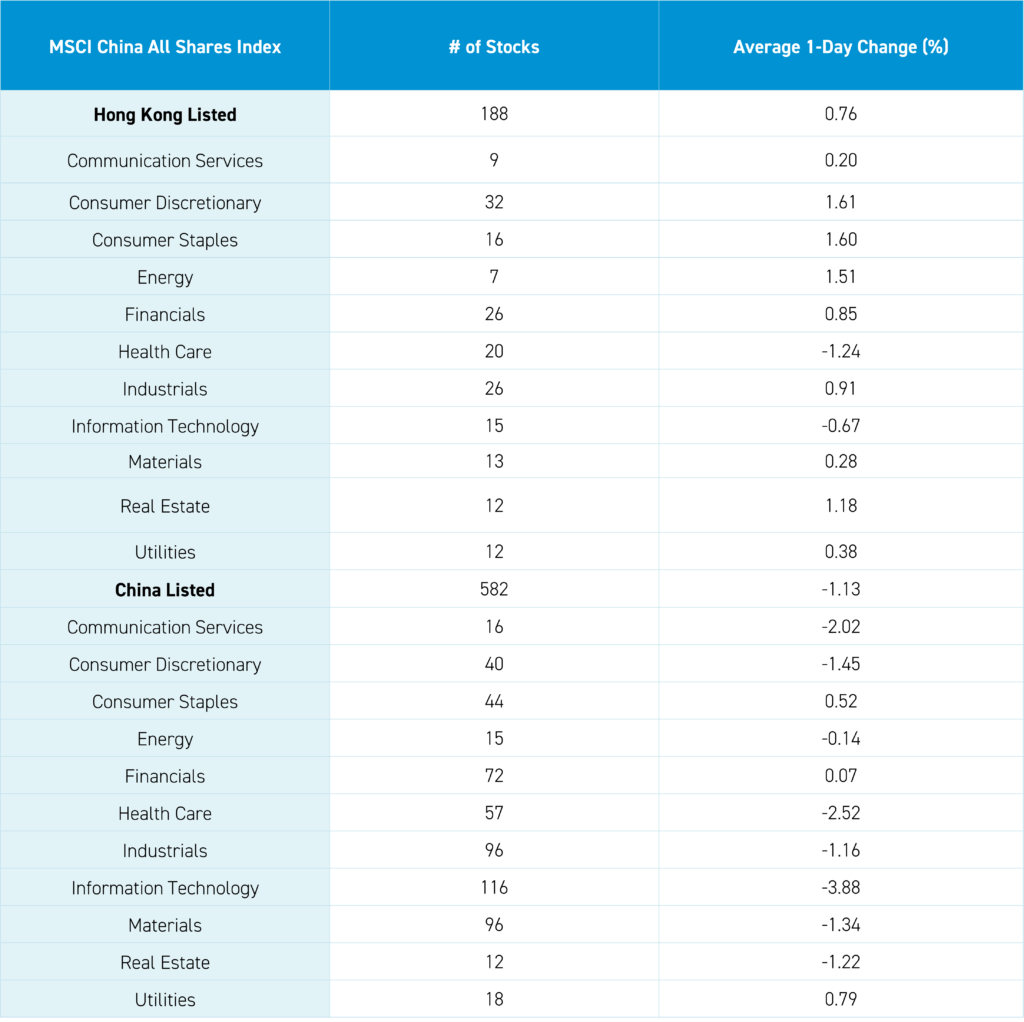

The Hang Seng and Hang Seng Tech indexes gained +0.78% and +0.54%, respectively, on volume that decreased -23.93% from Friday, which is 99% of the 1-year average. 260 stocks advanced while 213 declined. Main Board short sale turnover declined -41% from Friday, which is 103% of the 1-year average, as 18% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps outperformed the growth factor and large caps. The top-performing sectors were Consumer Discretionary, which gained +1.61%, Consumer Staples, which gained +1.60%, and Energy, which gained +1.51%. Meanwhile, Health Care fell -0.03% and Technology fell -0.01%. The top-performing subsectors were Foodstuffs, retail, and capital goods. Meanwhile, pharmaceuticals and semiconductors were among the worst-performing. Southbound Stock Connect volumes were high as Mainland investors sold a net -$332 million worth of Hong Kong-listed stocks and ETFs, including Sunac, which was a very small net buy, the Hang Seng Tech ETF, and China Tower. Meanwhile, Tencent, Lenovo, and CNOOC were moderate net sells.

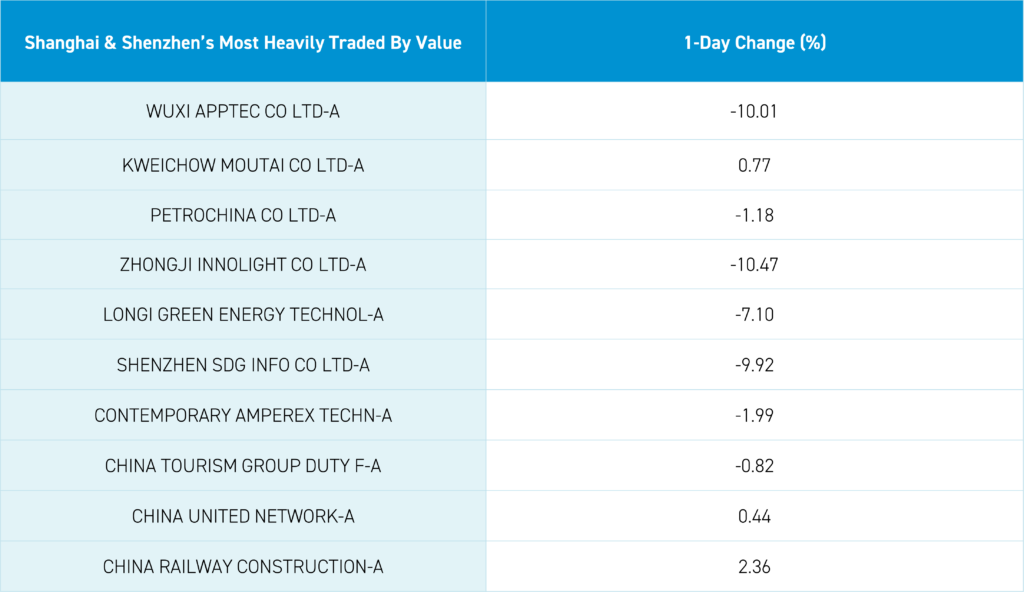

Shanghai, Shenzhen, and the STAR Board were off -0.92%, -2.42%, and -2.79%, respectively, on volume that declined -3% from Friday, which is 93% of the 1-year average. 456 stocks advanced while 4,537 stocks declined. The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. The top-performing sectors were Utilities, which gained +0.79%, Consumer Staples, which gained +0.53%, and Financials, which gained +0.07%. Meanwhile, Technology fell -3.88%, Health Care fell -2.52%, and Communication Services fell -2.02%. The top-performing subsectors were soft drinks, airports, and household appliances. Meanwhile, power generation, internet, and communication equipment were among the worst-performing subsectors. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$82 million worth of Mainland-listed stocks, including Kweichow Moutai, which was a large net buy, Zhongji Innolight, which was a moderate net buy, and CATL, which was a small net buy. Meanwhile, Wuxi AppTec was a moderate net sell, and PetroChina and CITS were small net sells. CNY and the Asia Dollar Index were off small versus the US dollar. Treasury bonds rallied along with steel, while copper was off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.18 versus 7.18 yesterday

- CNY per EUR 7.76 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.60% versus 1.60% yesterday

- Yield on 10-Year Government Bond 2.49% versus 2.50% yesterday

- Yield on 10-Year China Development Bank Bond 2.64% versus 2.65% yesterday

- Copper Price -0.06% overnight