National Team Catches Bottom, Alibaba May Spin Off Grocery Service, Week in Review

4 Min. Read Time

Week in Review

- China’s markets were lower this week following strong performance from last week, as volatility remains elevated.

- A Hong Kong court ordered the liquidation of Evergrande’s offshore assets on Monday, potentially putting the developer’s issues to rest as the PBOC’s pledged supplementary lending program was increased to help homes get delivered.

- CATL, the world’s largest battery maker, estimated net income growth between 38% and 48% for 2023 in its preliminary Q4 earnings report.

- China’s official non-manufacturing (services) Purchasing Managers’ Index (PMI) beat estimates and December’s reading, showing expansion.

Friday’s Key News

Asian equities cheered US technology earnings overnight, except for Apple, in a strong day, except for Mainland China and Hong Kong.

Both Hong Kong and Mainland China opened higher alongside their regional peers, though China came under significant pressure from forced selling as the small-cap CSI 500 Index hit the 4,500 level, creating a flash-crash due to the absence of buyers. “Snowballs”, which are like Hong Kong’s Callable Bull/Bear Contracts (CBBCs), provide investors exposure to an index or stock with an element of downside protection. When an index, such as the CSI 500, hits the maximum downside level, the issuer is forced to redeem the snowball by selling the underlying futures. The lack of buyers, which is exacerbated by light volumes as we approach the Chinese New Year holiday, the market plunged. The Shanghai Composite hit an intra-day low of -3.77%, Shenzhen hit a low of -5.80%, and the CSI 500 fell -5.19%. However, the cavalry arrived, as the National Team, which includes institutional investors affiliated with government-related entities, bought Mainland China-listed ETFs, which stabilized the market and pulled it off its lows to result in Shanghai closing lower by -1.46%, Shenzhen closing lower by -2.99%, and the CSI 500 closing lower by -2.47%. As a result of the mid-day buying, a certain CSI 300 ETF saw a massive volume increases of above +30% from yesterday, which includes a massive intra-day surge in the mid-afternoon.

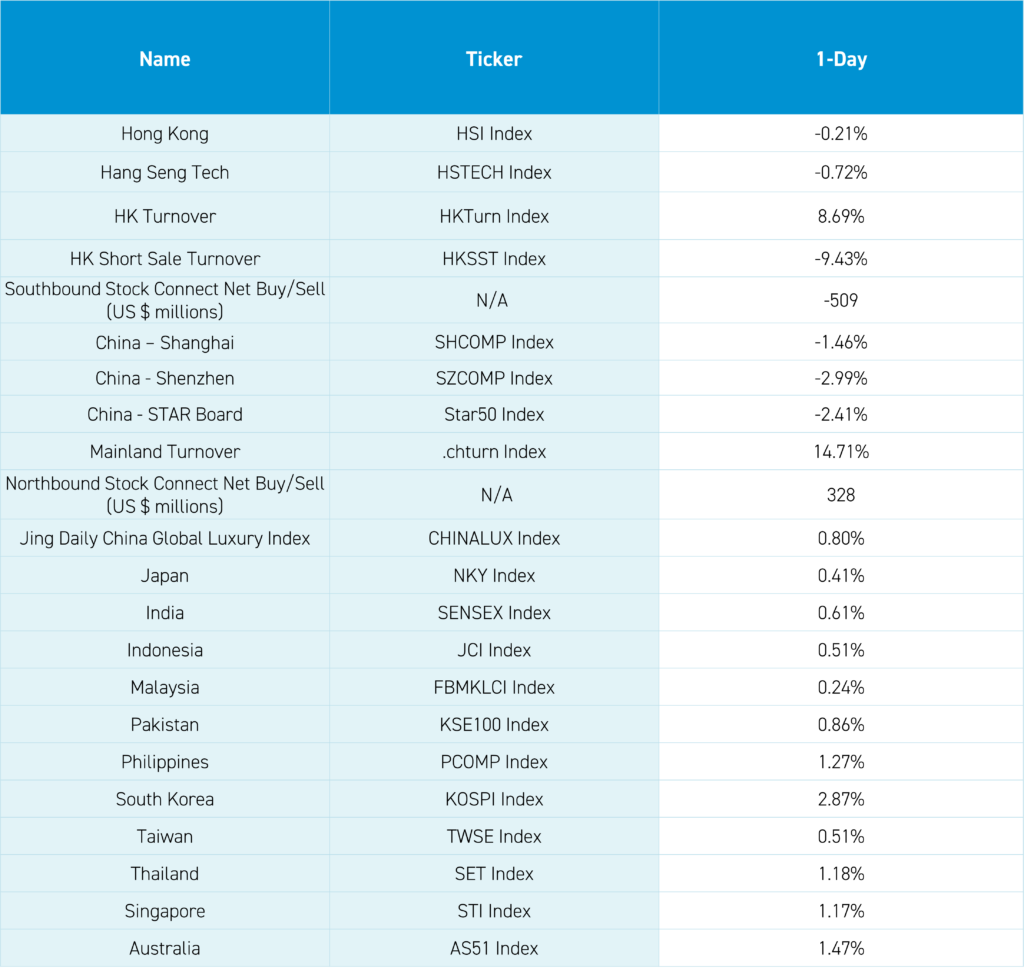

There was chatter about a potential Mainland China stabilization fund, to be funded by SOEs’ international revenue. This appears to be true as Northbound Stock Connect saw an intra-day jump of $328 million. Remember that neither Mainland China nor Hong Kong have circuit breakers like we do in the US.

Hong Kong came off morning gains as Mainland China pulled it down while Apple suppliers were weak on tepid revenue growth and increased competition in China.

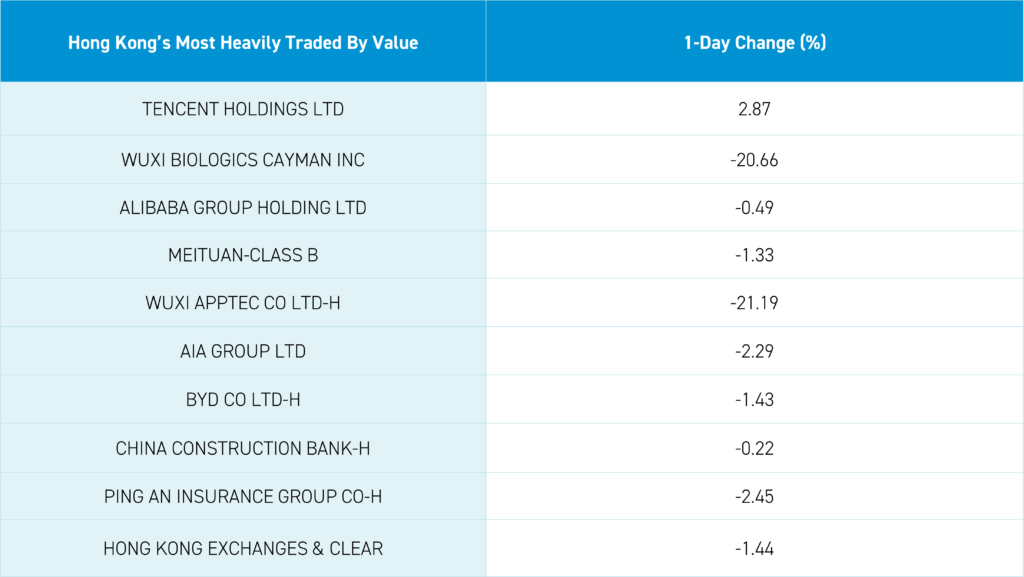

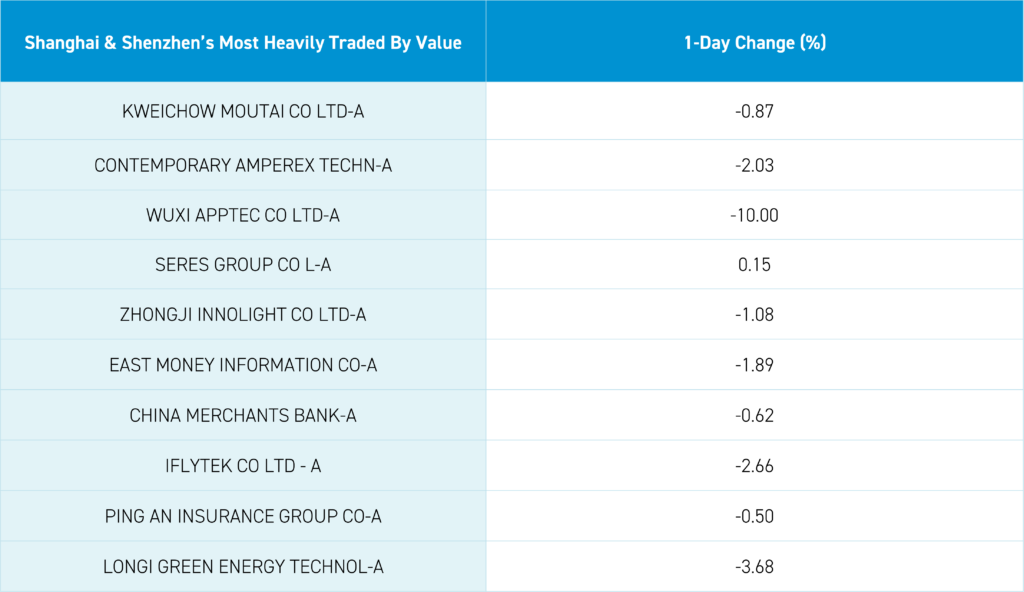

A mid-afternoon broker conference call on WuXi AppTec took the stock from a morning high of +4.6% after the company’s buyback announcement to -21.19% and WuXi Biologics to a low of -20.66%. The broker stated that the Biosecure Act will be passed, which would bar the company from US medical providers that receive federal Medicaid and Medicare dollars. Remember what happened when TikTok was banned? They sued and won in court. Today, US courts threw out the Florida law barring Chinese citizens from owning property in the state. I do not believe the allegations against a highly respected company that employs thousands of Americans across a dozen US facilities are true.

Hong Kong was off, but not nearly as much as Hong Kong’s most heavily traded stocks by value, which were Tencent, which gained +2.87% as several video games were approved, Wuxi Biologics, which fell -20.66%, Alibaba, which fell -0.49%, Meituan, which fell -1.33%, and WuXi AppTec, which fell -21.19%.

After the close, Reuters reported that Alibaba is considering spinning off its Freshippo grocery chain after yesterday’s rumor it would spin off its In Time department store chain. Clearly, the company is telling investors they believe the stock is cheap. Alibaba’s US Dollar bond, due this year, has outperformed the stock by 70%, showing the extent of the absurdity of Alibaba’s valuation.

Real Estate was a top-performing sector in Hong Kong, where it gained +1.25%, and Mainland China, where the sector gained +0.74% after yesterday’s expansion of the Pledged Supplementary Lending program, as the policy support increases.

Auto was another bright spot after January sales, though BYD fell -1.43% for no reason.

ANTA Sports gained +2.15% after yesterday’s Amer Sports IPO, which gained +6.2%. Tencent owns a stake in the sports apparel company as well. Things will get quiet as Chinese New Year starts next Friday as many will take a full, 2-week holiday.

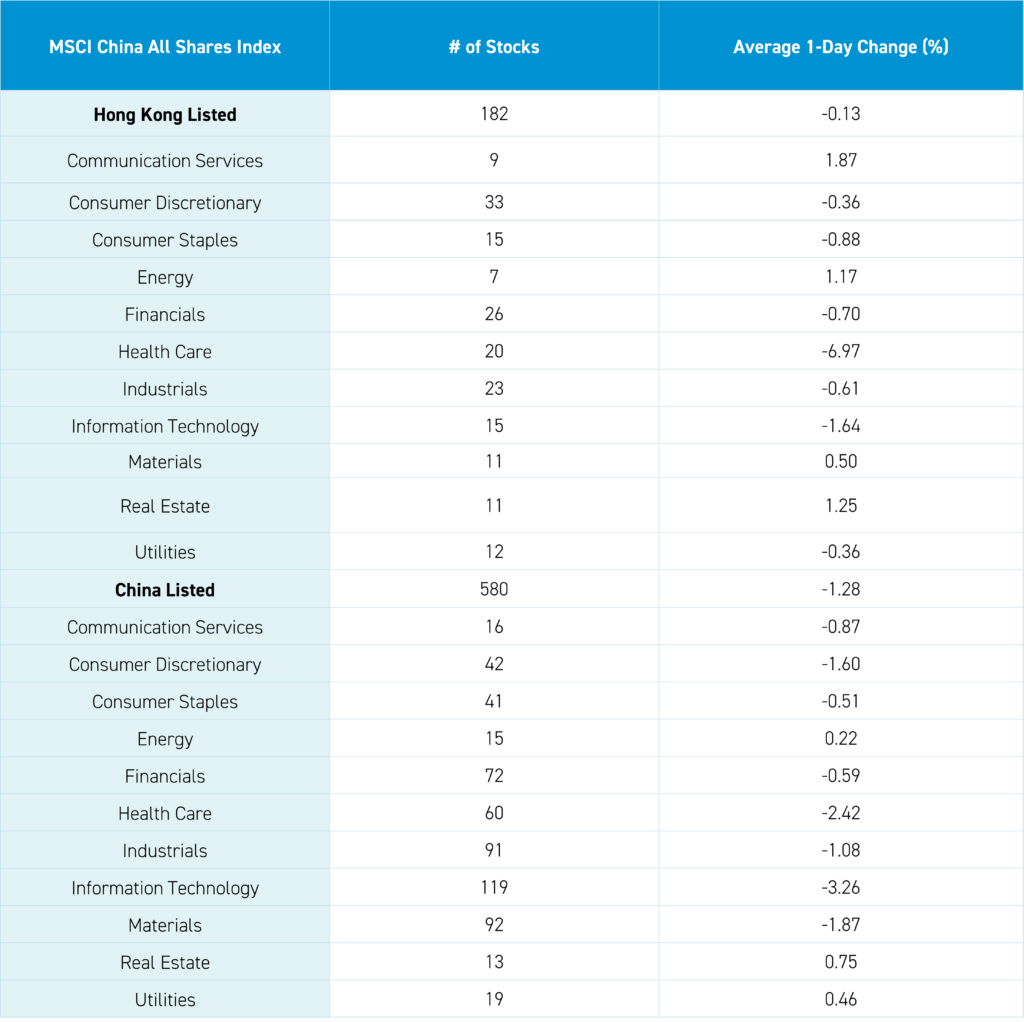

The Hang Seng and Hang Seng Tech indexes fell -0.21% and -0.72%, respectively, on volume that increased +8.69% from yesterday, which is 102% of the 1-year average. 153 stocks advanced while 320 stocks fell. Main Board short turnover declined -9.43% from yesterday, which is 97% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value and growth factors were both down, though the latter was down much more so than the former. The top-performing sectors were Communication Services, which gained +1.87%, Real Estate, which gained +1.25%, and Energy, which gained +1.18%. Meanwhile, Health Care fell -697%, Technology fell -1.64%, and Consumer Staples fell -1.64%. The top-performing subsectors were software, energy, and telecom services while media, pharmaceutical and food/staples were the worst. Southbound Stock Connect volumes were moderate as mainland investors sold -$509mm of HK ETFs and stocks with Wuxi AppTec, WuXi Bio and China Mobile small net buys while Tencent, HK Tracker ETF and HS China Enterprise ETF were large net sells.

Shanghai, Shenzhen, and the STAR Board fell -1.46%, -2.99%, and -2.41%, respectively, on volume that increased +14.71% from yesterday, which is 93% of the 1-year average. 376 stocks advanced while 4,627 declined. The value and growth factors were both down, though the latter was down much more so than the former. The top-performing sectors were Real Estate, which gained +0.74%, Utilities, which gained +0.45%, and Energy, which gained +0.21%. Meanwhile, Technology fell -3.27%, Health Care fell -2.42%, and Materials fell -1.88%. The top-performing subsectors were telecom, banking, and coal, while environmental protection, business services and software were the worst. Northbound Stock Connect volumes were very high as foreign investors bought $328 million worth of Mainland stocks with Zijin Mining, BYD and China Merchants Bank small net buys while Wuxi AppTec was a large net sell, Midea a moderate/large net sell and CATL a moderate net sell. The renminbi and Asia dollar index gained versus the US dollar. Treasury bonds rallied while copper and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.18 yesterday

- CNY per EUR 7.77 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.65% versus 1.64% yesterday

- Yield on 10-Year Government Bond 2.42% versus 2.44% yesterday

- Yield on 10-Year China Development Bank Bond 2.60% versus 2.60% yesterday

- Copper Price -0.85% overnight

- Steel Price -0.90% overnight