March of the Toreadors as Meituan Delivers

4 Min. Read Time

Key News

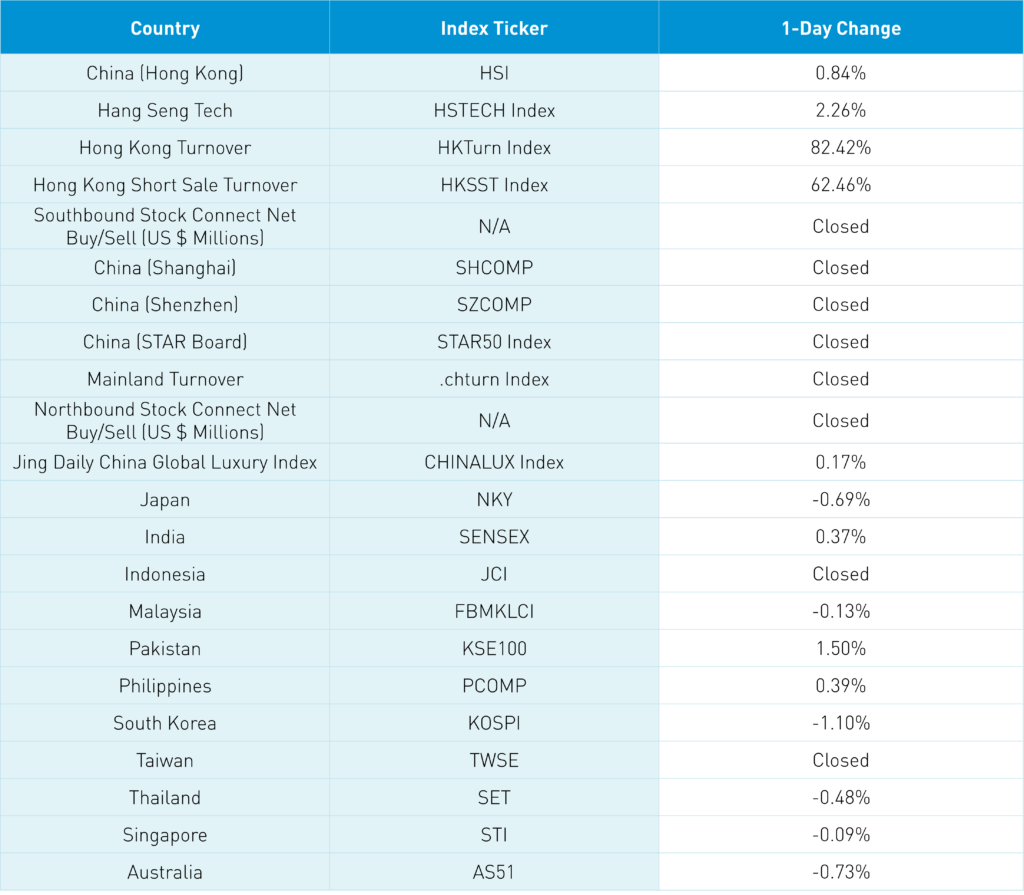

Gong Hei Fat Choy! Happy Chinese New Year! Asian equities were lower on the hotter-than-anticipated US CPI release as Fed cut hopes faded, though Hong Kong outperformed while Mainland China and Taiwan remain on holiday.

Hong Kong entered the Year of the Dragon off -2% in early trading but rallied and grinded higher all day. However, we must curb our enthusiasm. Volumes were light at just 57% of the 1-year average as most folks remain on vacation and Stock Connect remains closed for the rest of the week.

One overlooked factor on today's market action was last Friday’s release of January aggregate financing (RMB 6.5 trillion versus expectations of RMB 5.6 trillion and December’s RMB 1.94 trillion), and new loans (RMB 4.92 trillion versus expectations of RMB 4.5 trillion and December’s RMB 1.17 trillion) beating expectations.

Chinese New Year vacation and travel data within Mainland China, to Hong Kong, Macau, and overseas appear strong. For 2024, The China Tourism Research Institute predicts that domestic tourism will increase by 22% year over year to RMB 6 trillion, while international tourism will increase by 38% to $107 billion, which is 105% and 81% of the 2019 numbers. A Mainland media source stated there were 195.24 million passenger trips on last Friday's first day of the holiday, which is +26.7% year-over-year (YoY). I witnessed this at Milan’s airport last week, where I saw hundreds of Chinese tourists being shepherded onto a dozen buses.

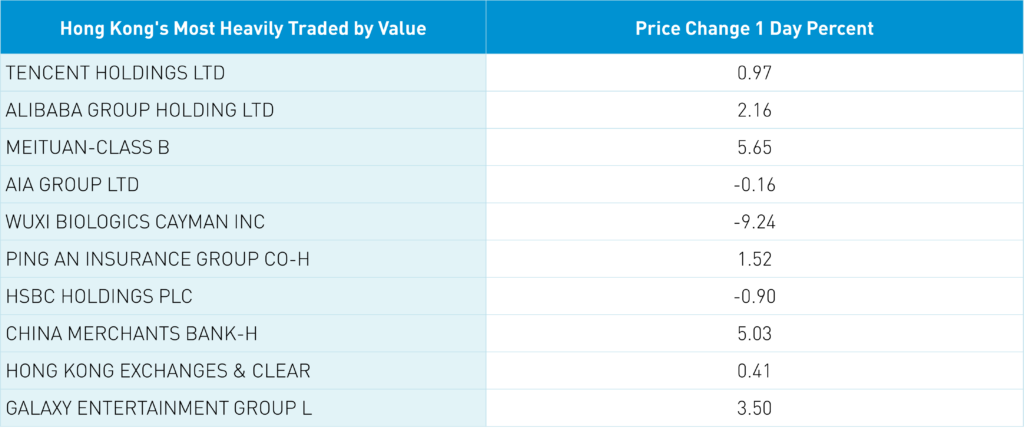

Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.97%, Alibaba, which gained +2.16%, with President Michael Evans attending the World Government Summit in Dubai, Meituan, which gained +5.65% after reporting an increase of +29% YoY of “offsite meal orders” through February 11th, AIA, which fell -0.16%, and Wuxi Biologics, which fell -9.24% on continued scrutiny from US lawmakers. The company employs thousands of workers in the US, and the claims of these lawmakers are entirely inaccurate, in my opinion. No journalist has written that US institutional investors, according to SEC 13F filings, owned 446,560,699 shares, putting the loss incurred by US investors due to the Congressional proposal to $7.591 billion!!!

Below is a deep dive into the absurdly stupid headlines about MSCI’s “purge” of Chinese stocks. Mainland investors have cheered the new head of the China Securities Regulatory Commission (CSRC) due to the market’s strong performance while he ran the Shanghai Stock Exchange, as I’m sure improving market sentiment is job #1 for him. There was a fair amount of chatter about a Bank of America report showing professional investors’ favorite/most crowded trades are long US tech and short China tech, indicating that investors are not well positioned for a rally. Hong Kong’s Callable Bull/Bear Contracts (CBBCs) and China’s Snowballs are derivative contracts that provide investors leveraged exposure to an index, though they have an index level that forces the contract to be liquidated if the index falls, which forces the issuer to redeem the futures contract behind the contract. If we’ve had a liquidation of these contracts over the last two months, I would hope we can get a rally from here. Fingers crossed!

On Monday night, MSCI released the pro forma for its end-of-the-month index rebalance. The US’ weight in the All-Country World Index (ACWI) is 62%. the nattering nabobs of negativity have highlighted that 66 Chinese companies are being removed from indices. While true, these stocks are tiny weights in the index! Meanwhile, virtually all companies being removed are less than 0.00% of the MSCI EM index! The largest stock being removed is Chinasoft International, which is at a 0.03% weight!!!! That’s the LARGEST being removed, with the majority of the eliminated stocks having weight less than 0.00%. Absurd right? I posted the weights on my X yesterday (@ahern_brendan).

China’s remaining 703 stocks' weight in EM will fall from 25.7% to 25.4%. Is that world ending? Hardly. A better article would have been on how Amazon and Nvidia have market caps larger than MSCI China, India, and Taiwan. With either Amazon or Nvidia’s market cap, you could buy 2 South Koreas. India’s 136 stocks weight increases from 17.9% to 18.2%. Meanwhile, China’s GDP is still more than 4X larger than India’s. Investors should remember index providers have a poor track record of inclusions marking a top (S&P 500 adding Yahoo back in 2000, Hang Seng adding tech stocks in December 2020, etc). India’s bonds will also be added to the Bloomberg Global Aggregate and JP Morgan indexes this year.

A prominent Congressional China hawk announced he is retiring because he isn’t a Trump Republican, as he was going to face a primary challenge. He’ll visit Taiwan for some photos. Maybe that was the top of the China narrative, as domestic issues are what people really care about—likely wishful thinking.

The Hang Seng and Hang Seng Tech indexes gained +0.84% and +2.26%, respectively, on volume that increased +82% from Friday, which is 57% of the 1-year average. 220 stocks advanced, while 261 declined. Main Board short turnover increased by +62% from last Friday, which is 57% of the 1-year average, as 18% of turnover was short turnover (remember HK short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps outperformed the growth factor and small caps. The top sectors were discretionary +2.7%, financials +1.2%, and communication +1.18%, while utilities -1.83%, healthcare -1.81% and materials was 1.26%. The top sub-sectors were retailing, consumer services, and media, while pharmaceuticals, materials, and diversified finance were the worst. Southbound Stock Connect was closed.

Shanghai, Shenzhen, and STAR Board were closed and will remain closed until next Monday, February 19th.

Last Night’s Performance

Last Night's Exchange Rates, Prices, & Yields

Mainland China's fixed income, currency, and commodity markets were closed overnight.