Trip.com Takes Flight on +105% Revenue Growth

3 Min. Read Time

Trip.com Q4 Earnings Overview

After the US close yesterday, travel booking platform Trip.com reported Q4 and 2023 financial results. Executive Chairman James Liang summed it up nicely: “in 2023, China embarked on a significant journey of reconnecting with the world driven by rising travel sentiment.” Management raised its 2024 guidance above analyst estimates in a strong statement of confidence.

- Q4 Revenue grew +105% year-over-year (YoY) to RMB 10.3 billion ($1.5 billion) versus expectations of RMB 10.2 billion ($1.4 billion)

- 2023 Revenue grew +122% to RMB 44.5 billion ($6.3 billion)

- Non-GAAP net income grew to RMB 2.7 billion ($376 million) from RMB 498 million ($69.3 million) in Q4 2022 versus expectations of RMB 1.5 billion ($200 million)

- Non-GAAP EPS came in at RMB 4 ($0.56) versus expectations of RMB 2.3 ($0.32)

- The company repurchase 6.8 million shares, worth $224 million in Q4 while the Board approved another $300 million worth of stock buybacks and/or dividends

Key News

Asian equities had a strong day, led by growth stocks and sectors following Nvidia’s strong results after the US close yesterday.

Both Mainland China and Hong Kong overcame early losses to grind higher on strong breadth, with advancers outpacing decliners handily and all sectors positive in Hong Kong, with only real estate down in China.

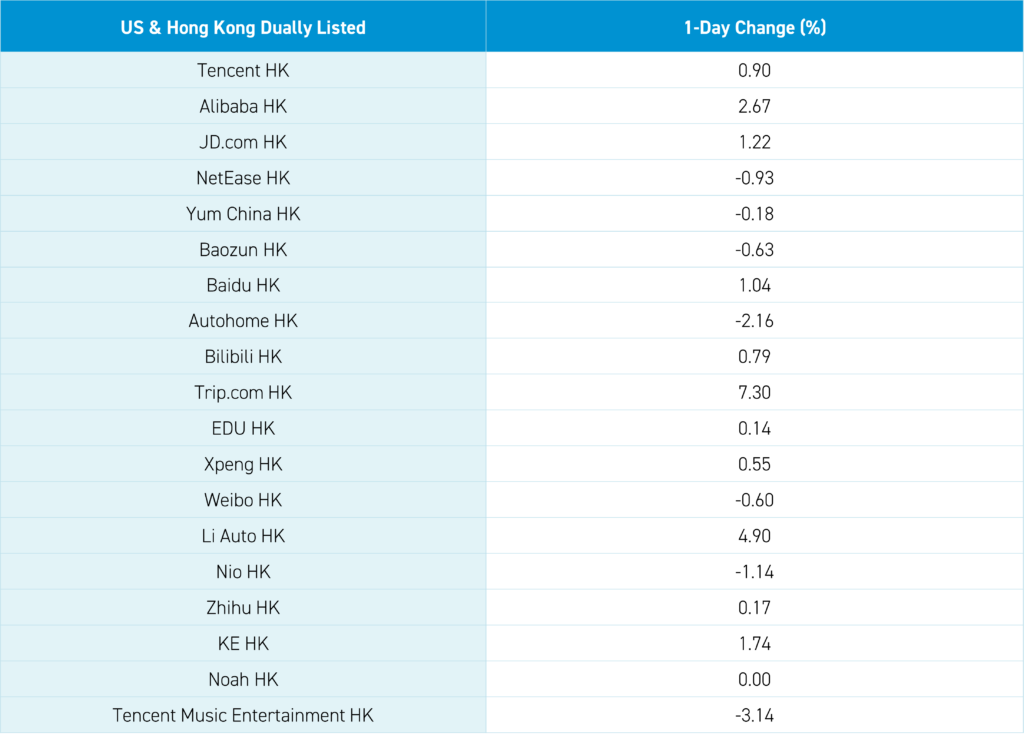

Mainland China posted its seventh straight positive day on good volumes, though it was slightly off from yesterday’s exceedingly high numbers. The skepticism on this rally is palatable, which makes me bullish. Technical analysts might notice Hong Kong and China indices driving through their 50 and 100-day moving averages. Trip.com gained +7.3% n Hong Kong on a positive outlook for travel. You can follow the bouncing ball as travel and restaurant sales led to broader retail sales.

Yesterday’s reports on short selling bans, limiting major transactions at the open and close, and the examination of a quant hedge fund’s dumping of shares, helped lift Mainland market sentiment. At a press conference, it was clarified that short selling was not banned, though arguably it is an implied ban, while “abnormal transactions” will be examined.

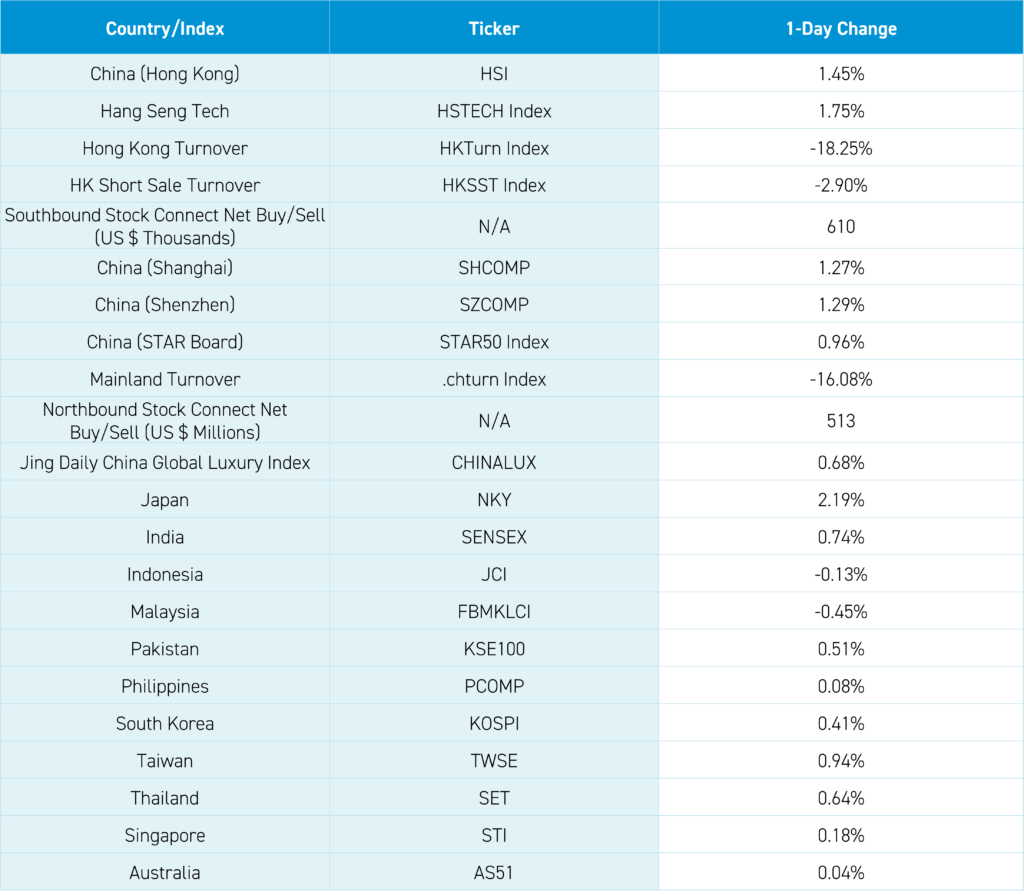

Northbound Stock Connect followed yesterday’s massive $1.89 billion worth of inflow, which I calculate as the 12th biggest net inflow day ever for Shanghai Connect, saw $513 million worth of net buying of Mainland stocks today with Kweichow Moutai a strong net buy. Ten Mainland China listed equity ETFs have seen more than +$1 billion of inflow over this month, with the top three ETFs seeing more than +$5 billion of inflow. The first China equity ETF listed outside of China, including Hong Kong, is #18, with $274 million worth of inflow this month. Foreign skepticism? Yes, and rightly so, after a very “difficult” three years.

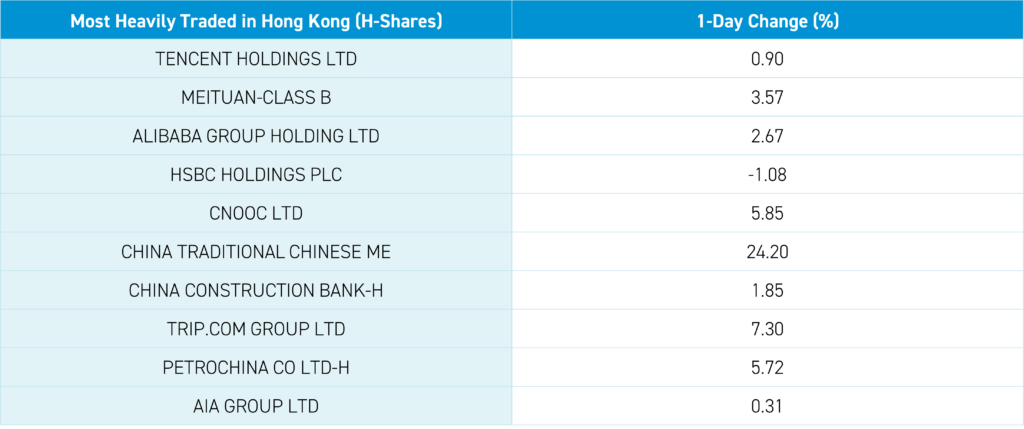

After the close, the Ministry of Commerce held its first press conference since Chinese New Year with a focus on efforts to attract foreign capital and reported that e-commerce sales over Chinese New Year grew +9% to RMB 1.2 trillion. Air conditioners and foldable mobile phones were popular, with increases of +262% and +131%, respectively, YoY. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.90%, Meituan, which gained +3.57%, Alibaba, which gained +2.67%, HSBC, which fell -1.08%, and CNOOC, which gained +5.85%. In another sign of the bottom, China Traditional Medicine (570 HK) gained +24.2% after announcing being taken private by Sinopharm.

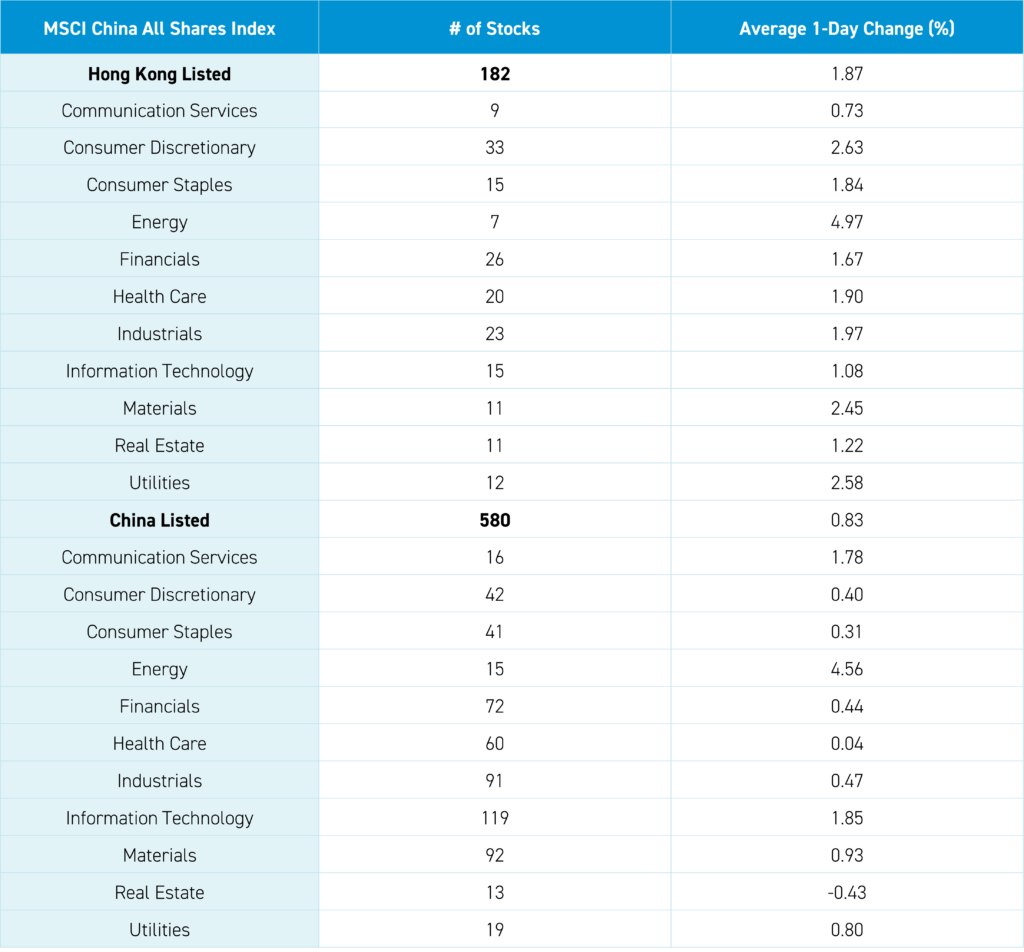

The Hang Seng and Hang Seng Tech indexes gained +1.45% and +1.75%, respectively, on volume that decreased -18.25% from yesterday, which is 101% of the 1-year average. 395 stocks advanced, while 94 declined. Main Board short turnover fell -2.9% from yesterday, which is 90% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were positive, as the growth factor and large caps outperformed the value factor and small caps. All sectors were positive, including Energy, which gained +4.97%, Consumer Discretionary, which gained +2.63%, and Utilities, which gained +2.58%. Media was the only negative sub-sector. Meanwhile, Energy, Retail, and Foodstuffs were among the top-performing subsectors. Southbound Stock Connect volumes were high/moderate as Mainland investors bought a net $610 million worth of Hong Kong-listed stocks, including CNOOC, a large net buy, Meituan, and Li Auto. Meanwhile, China Traditional Medicine was a moderate net sell, along with China Mobile and Semiconductor Manufacturing (SMIC).

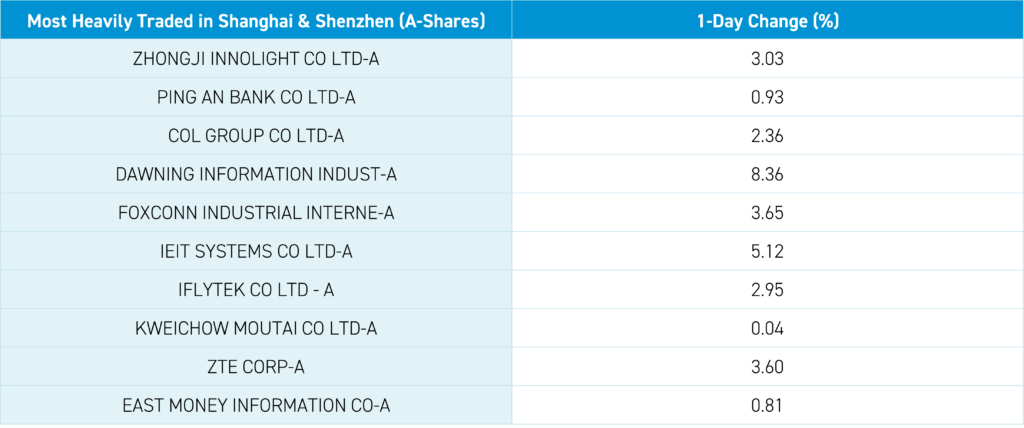

Shanghai, Shenzhen, and the STAR Board gained +1.27%, +1.29%, and +0.96%, respectively, on volume that decreased -16.08% from yesterday, which is 96% of the 1-year average. 418 stocks advanced, while 479 declined. All factors were positive, as the growth factor and large caps outperformed the value factor and small caps. Real Estate was the only negative sector, falling -0.44%, while Energy gained +4.56%, Technology gained +1.85%, and Communication Services gained +1.78%. Airports and education were the only negative subsectors, while coal, computer hardware, and oil/gas were the top performers. Northbound Stock Connect volumes were moderate/high as foreign investors bought $513 million worth of Mainland stocks, including Kweichow Moutai, which was a moderate/high net buy, CATL, and PAB. Zhongji Innolight was a small/moderate net sell, while CMB and ZTE were very small net sells. CNY was up slightly versus the US dollar. Treasury bonds rallied along with copper and steel.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.80 versus 7.76 yesterday

- Yield on 10-Year Government Bond 2.40% versus 2.41% yesterday

- Yield on 10-Year China Development Bank Bond 2.57% versus 2.58% yesterday

- Copper Price +0.55%

- Steel Price +0.13%