Grind Higher as Baidu’s AI Efforts Recognized from an Unlikely Source, Week in Review

3 Min. Read Time

Week in Review

- Asian equities were mostly higher this week as Mainland China outperformed with the Shanghai Composite logging a gain of +4.85% and the Shenzhen Component gaining +5.87%.

- China cut the 5-year loan prime rate (LPR), which mortgages are based on, down to 3.95% from 4.20% versus expectations of 4.10%, one of the deepest cuts ever, leading to a rebound in real estate.

- The China Securities Regulatory Commission (CSRC) added new restrictions on short-selling this week, which helped market sentiment.

- Trip.com reported Q4 and 2023 financial results on Thursday, announcing that revenue increased +105% year-over-year (YoY) to RMB 10.3 billion as travel rebounds in China.

Friday’s Key News

Asian equities closed a positive week, mostly higher, with Japan on holiday for the Emperor’s Birthday. It was a quiet end to a good week for Hong Kong and China, as yesterday’s CSRC regulatory news was still a topic of discussion.

There was a fair amount of chatter on the Shanghai Composite closing above the 3,000 level for the first time since mid-December as mainland China extended its winning streak to eight days on another strong breadth/advancers beat decliners handily. Growth stocks had a good day in mainland China as Nvidia’s supply chain stocks gained.

President Xi presided over the fourth meeting of the Central Committee for Financial and Economic Affairs with the release promoting “large-scale equipment updates and consumer trade-in issues, study the effective reduction of logistics costs.” Maybe a good thing for home appliance makers? Premier Li presided over a State Council meeting focused on “policy measures to attract and utilize more foreign investment.”

Since the San Francisco APEC conference, there has been a change in the tone of China’s leaders towards the economy, foreign investors, and corporations. Did you notice any news from China on the US Congressional visit to Taiwan? Me neither. Ultimately, China’s economy is geared to the West, which could explain the policy shift.

Bloomberg is reporting the US and China are working together on preventing EM defaults at World Bank meetings.

Hong Kong was basically flat overnight on light news, led by the most heavily traded stocks by value, which were Meituan, which gained +2.19%, Tencent, which fell -0.21%, CNOOC, which gained +0.49%, Ping An Insurance, which gained +1.63%, and China Construction Bank, which gained +0.40%.

New and used home prices fell in January, though at a slower rate, as recent measures should slowly stabilize the prices. If anything, the “bad” data will mean more policy support as headlines look backward though markets look forward. Hong Kong and Mailand China-listed real estate stocks were up, though I still find the bonds more interesting.

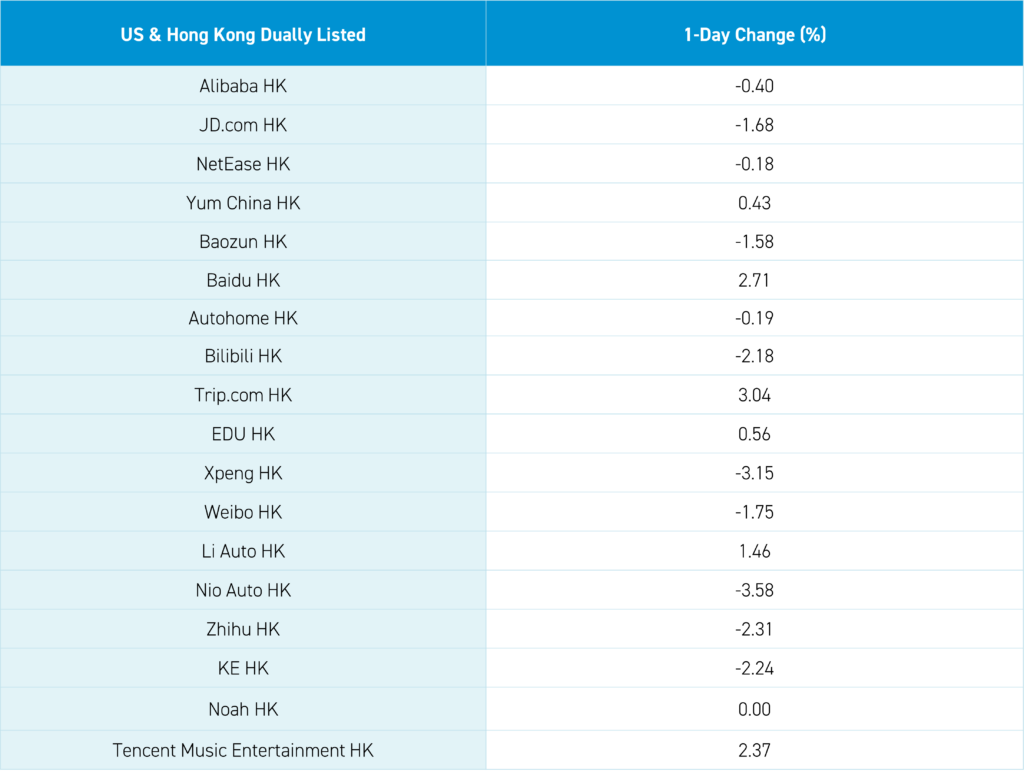

Baidu gained +2.71% on a short-selling firm recommending investors buy the stock as an inexpensive AI play. That is interesting, right? Baidu wisely invested profits from their search business in AI and EV years ago.

BYD fell -1.12% despite announcing Middle East expansion plans. Mainland investors bought a healthy net $823 million worth of Hong Kong-listed stocks and ETFs today. CNY has been very stable versus the US dollar, even with US interest rate cuts being pushed out.

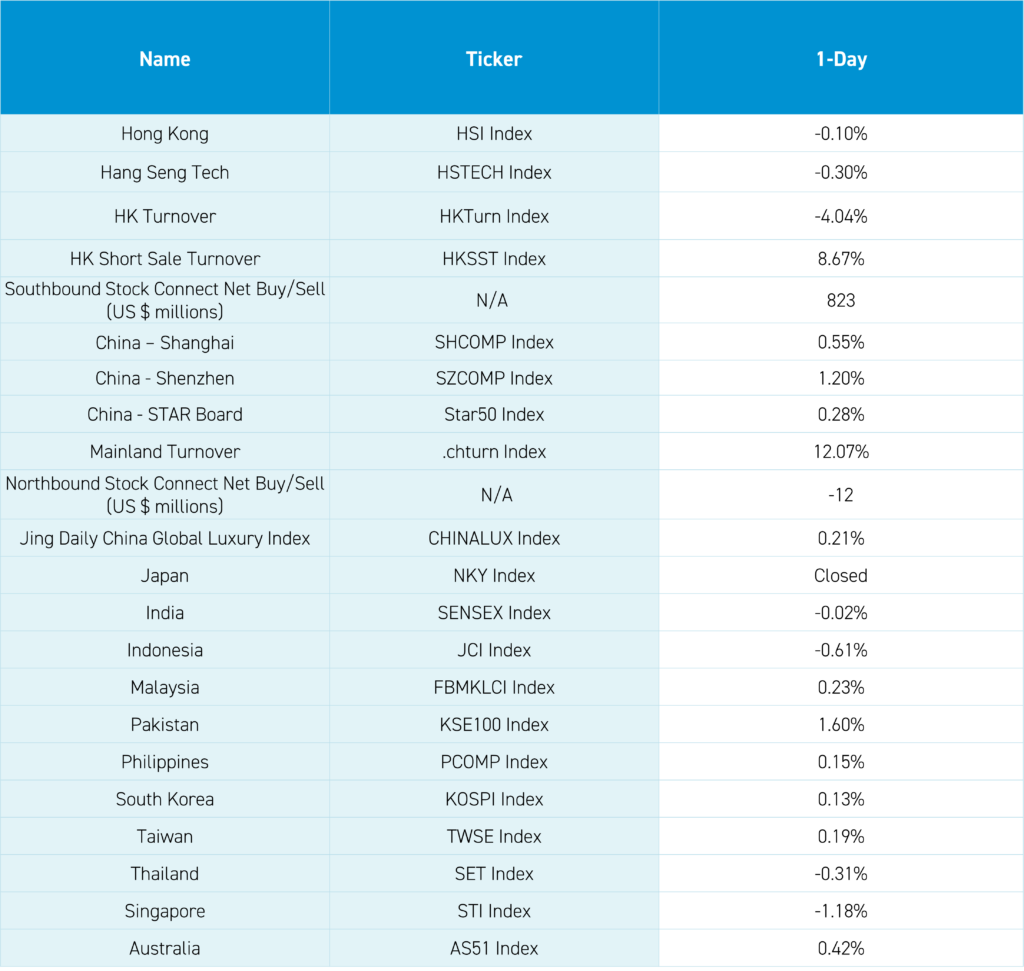

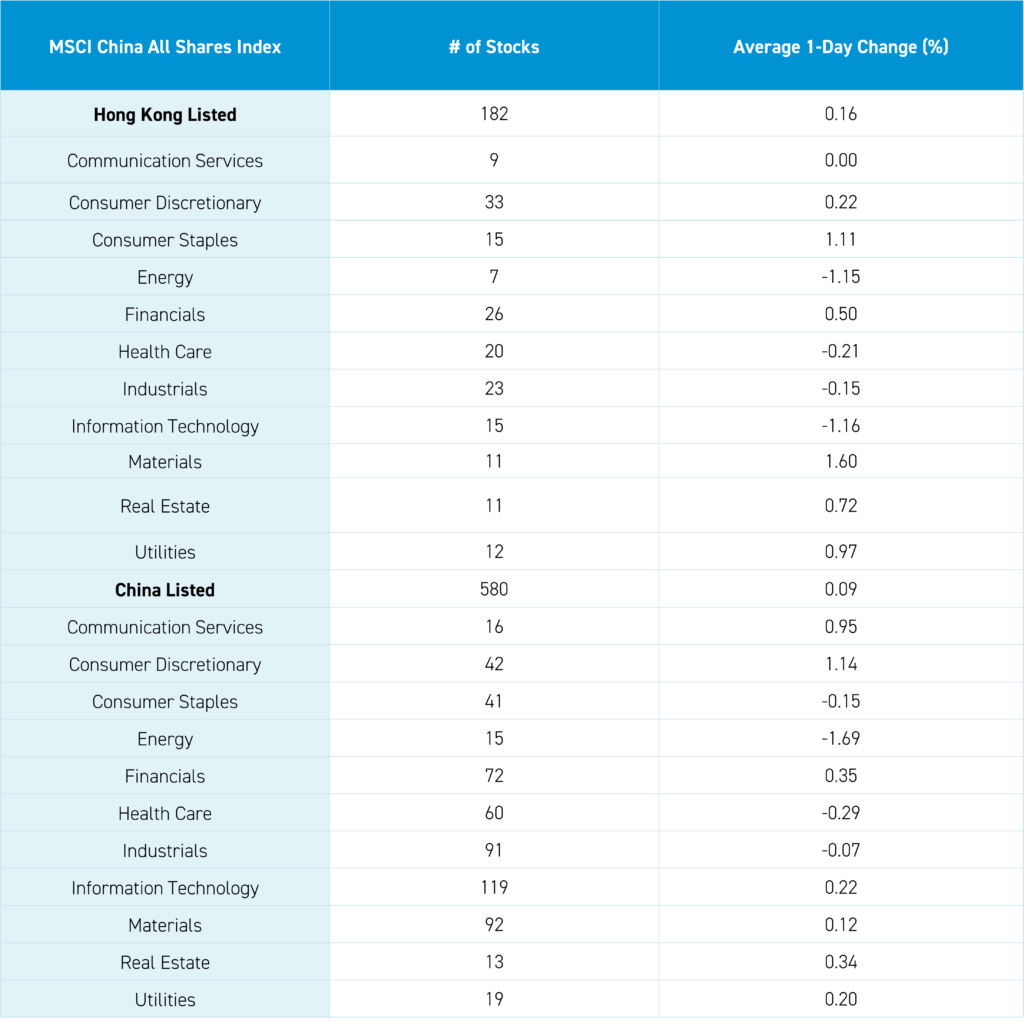

The Hang Seng and Hang Seng Tech indexes fell -0.10% and -0.30%, respectively, on volume that decreased -4.04% from yesterday, which is 97% of the 1-year average. 241 stocks advanced, while 237 declined. Main Board short turnover increased +8.67% from yesterday, which is 97.9% of the 1-year average, as 18% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor outperformed the value factor, with both posting a positive return, while large caps underperformed small caps. The top-performing sectors were Materials, which gained +1.6%, Consumer Staples, which gained +1.11%, and Utilities, which gained +0.97%. Meanwhile, Technology fell -1.16%, Energy fell -1.15%, and Health Care fell -0.21%. The top-performing subsectors were food/staples, media, and materials, while telecom services, technical hardware, and energy were among the worst-performing subsectors. Southbound Stock Connect volumes were moderate/high as Mainland investors bought a net $823 million worth of Hong Kong-listed stocks and ETFs, including energy giant CNOOC, which saw a large net inflow, the Hong Kong Tracker ETF, and Hang Seng Tech ETF, which saw moderate/light net buying.

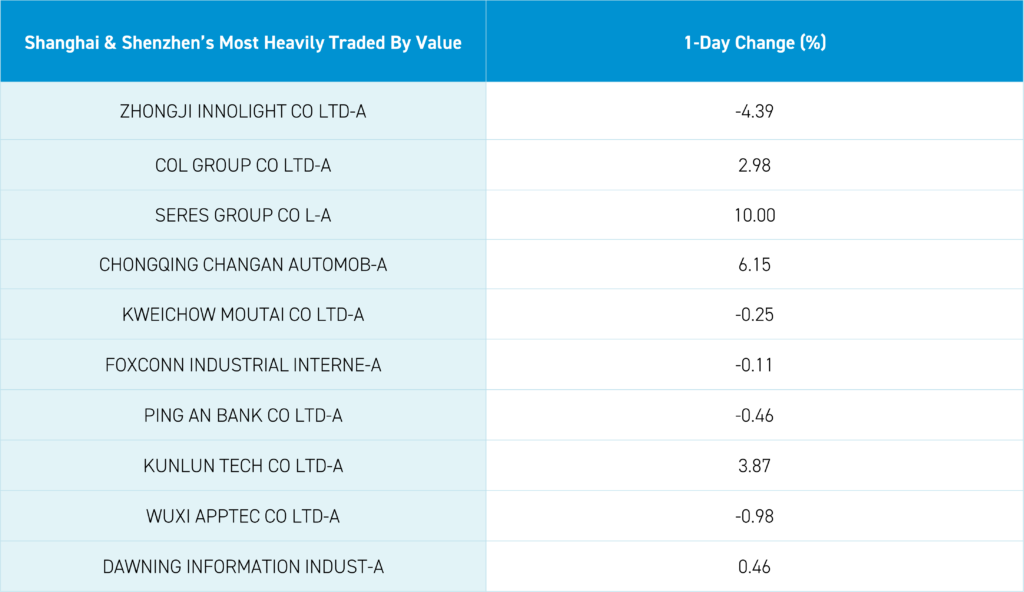

Shanghai, Shenzhen, and the STAR Board gained +0.55%, +1.2%, and +0.28%, respectively, on volume that increased +12% from yesterday, which is 107% of the 1-year average. 4,279 stocks advanced while 634 declined. The growth factor and small caps outperformed the value factor and large caps underperformed. The top-performing sectors were Consumer Discretionary, which gained +1.14%, Communication Services, which gained +0.95%, and Financials, which gained +0.35%. Meanwhile, energy -1.69%, healthcare -0.29% and staples -0.15% were the worst. Top sub-sectors were cultural media, leisure products and industrial machinery while coal, telecom and construction machinery were the worst. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$12mm of mainland stocks led by moderate buys in Ping An, ICBC and ABC while Luzhou Lao Jia was a moderate net sell, Changan Auto and BYD very small net sells.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.20 versus 7.19 yesterday

- CNY per EUR 7.79 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.50% yesterday

- Yield on 10-Year Government Bond 2.40% versus 2.40% yesterday

- Yield on 10-Year China Development Bank Bond 2.56% versus 2.57% yesterday

- Copper Price +0.19%

- Steel Price +0.13%