Meituan Runs Over Shorts As Investors Call For The Policy Support Cavalry, Week in Review

5 Min. Read Time

Week in Review

- Asian equities were mostly higher this week as Mainland China and Pakistan outperformed.

- For the week, Shanghai gained +0.74%, Shenzhen gained +3.33%, and the STAR Board gained +6.67%.

- We had earnings reports from Li Auto, which beat estimates; Baidu, which was mixed; Vipshop, which beat estimates; and NetEase, which missed estimates slightly.

- AI and hardware stocks powered the STAR Board’s gain this week on comments from some government meetings that were precursors to the “Two Sessions”, which is next week.

Friday's Key News

Asian equities were mixed overnight, as Japan, China, and India outperformed, while Taiwan and South Korea fell.

Mainland China and Hong Kong overcame morning losses to grind higher on high volumes that were over 100% of the 1-year average, an indication that someone is buying. Yesterday was MSCI’s index rebalance, which is always one of the highest volume days of the year, so today’s continuing high volumes are quite impressive. However, China’s breadth (advancers versus decliners) was not as positive as yesterday’s amazing 50 to 1, but it was decent, nonetheless.

Investors bid up stocks and sectors that are potential beneficiaries of new policies that could arise from the upcoming “Two Sessions”, including technology subsectors with buzzwords like AI, semiconductors, lithography, home appliances, and autos. The top-performing sectors were Technology, Consumer Discretionary, and Health Care.

February’s purchasing managers’ indexes (PMIs) were mixed. PMIs are diffusion indexes with readings above 50 indicating expansion and readings below 50 indicating contraction. These readings are not bad, considering that very little gets done during China’s 2-week Lunar New Year celebration. Services (i.e. non-manufacturing) showed a higher-than-expected expansion. However, manufacturing was not great as new orders were 49%, “indicating that manufacturing market demand declined compared with last month.” Manufacturing employment was off, though inventories declined. It is not a coincidence that US consumer confidence for February was also lower than expected.

The economic data shows that the economy needs more support. Fortunately, next week’s “Two Sessions” provides the perfect opportunity to do so. Poor real estate price performance in February also validates the need for more policy support, though it is difficult to buy property if you are visiting Europe, Hainan Island, or Thailand during vacation.

Treasury bonds had a mini flash crash intra-day today as the 30-year sold off -2.04% before recovering to a loss of only -0.33%. The 10-year sold off -0.54% before closing at a loss of only -0.20%. The 30-year has small relative issuance as most of the Chinese government debt is very short-term, which likely explains the volatility, though someone clearly took some profits. Could these profits be going into stocks? It certainly would make sense, as Mainland equity dividend yields are nearly equal to bond yields.

Foreign investors sold a net -$740 million worth of Mainland stocks, though net sales driven by MSCI’s index rebalance might have been a factor. It looks like the National Team had the day off.

Despite US-listed China stocks’ lackluster day yesterday, Hong Kong had a great day, led by the most heavily traded stocks Meituan, which gained +10.78% after exiting their Groupon-like group buying business and ran over shorts (I will not shed a tear), Tencent, which pulled another James Bond by gaining +0.07%, Alibaba, which gained +0.21%, Li Auto, which gained +1.07% after reporting that February deliveries increased to 20,251 versus January’s 16,620, HSBC, which gained +1.58%, and NetEase, which fell -1.93% after a weak Q4, though their game pipeline looks good for Q1.

Li Auto appears to be an outlier as peers, including BYD, NIO, and XPeng, saw big declines in January sales, which, I assume, are due to holiday travel. Li Auto focuses exclusively on SUVs geared towards use by families.

Are we in a period of de-enlightenment? Despite having access to so much data, why are there so many examples of misinformation, hyperbole, exaggeration, and misleading messaging? I could not help but ponder this yesterday as I watched US politicians try to outdo one another with dueling headlines on banning China-based electric vehicle (EV) manufacturers in the US. They are already effectively banned due to extremely high tariffs, though somehow Polestars get a pass being made in conjunction with Volvo. I find the security concern argument a joke, as our mobile phones are already mobile surveillance devices that sell everything we do to advertisers and are, you guessed it, made in China. Virtually every country globally enjoys the benefits of low-cost EVs from China-based automakers. Protecting US auto jobs is a good idea, though most foreign-branded vehicles are made here anyway. Why not allow for more foreign companies to set up factories in Michigan, Ohio, etc.? That would seem logical to me. I grew up with reporters like John Stossel and Bernie Goldberg, who investigated officials and called them out for their pandering. Today, no one in the media does that, I assume. Because the US government’s media spending must be so large, no one will bite the hand that feeds them. Exhibit A would be the US-China Economic and Security Council, which reports to Congress. If you look at their work, you can understand why Congress is so anti-China. If you look at their board, you will notice that absolutely no US businesses with China revenues are represented. The Chairwoman is “currently a psychotherapist in private practice,” though she previously worked for a Republican senator. Meanwhile, the Vice Chair is an ex-staffer for Nancy Pelosi. The Senior Policy Advisor to the Chief Executive Officer of Palantir is also on the board. Palantir is a government-contracting technology company, so their interests are clear. It is a pathetic joke that US multinationals that generate hundreds of billions of revenue in China have zero representation. Where are the people from the US Chamber of Commerce or Council om Foreign Relations? Will any reporter write about this? Nope. But you do not have to trust me and can do your own research.

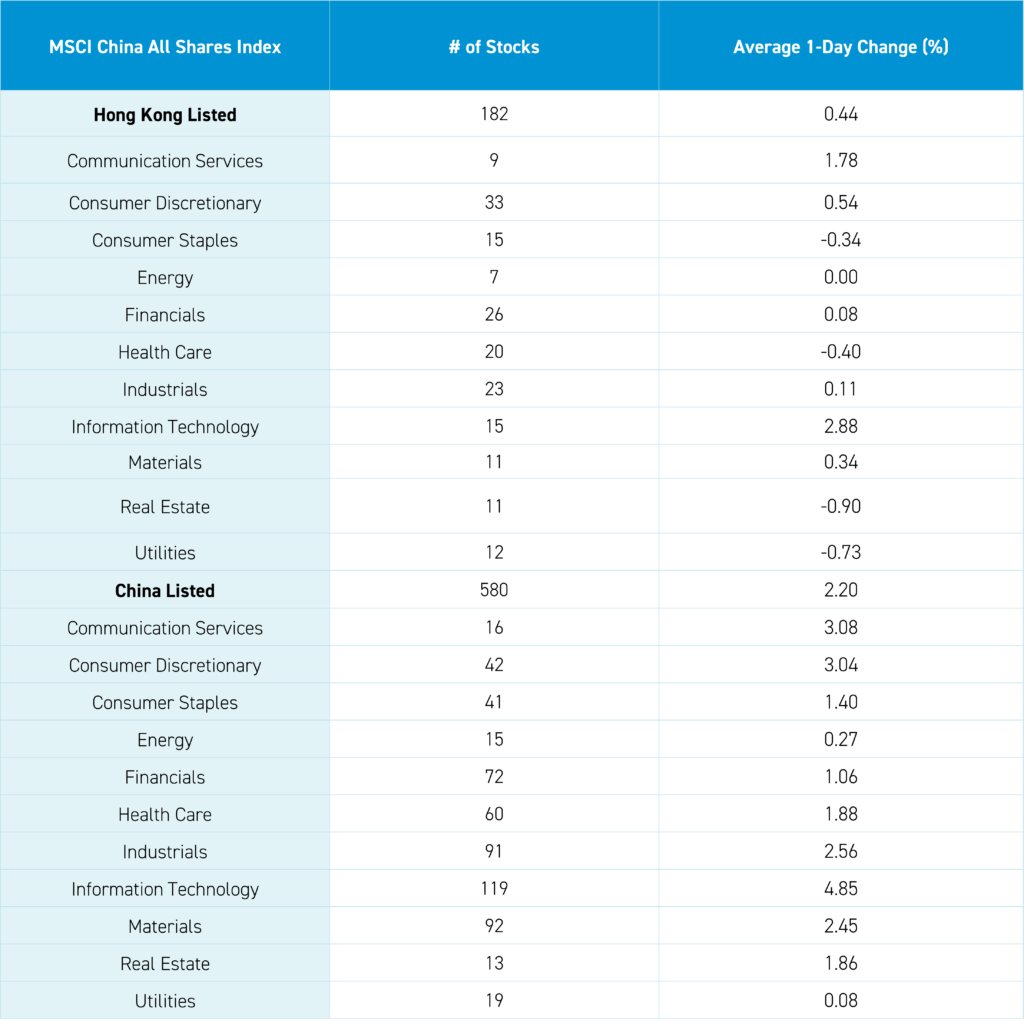

The Hang Seng and Hang Seng Tech indexes gained +0.47% and +1.66%, respectively, on volume that declined -6.40% from yesterday, which is 123% of the 1-year average. 269 stocks advanced, while 214 declined. Main Board short turnover declined -32.46% from yesterday, which is 116% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Materials, which gained +2.22%; Consumer Discretionary, which gained +1.93%; and Technology, which gained +1.54%. Meanwhile, Health Care fell -2.31%, Real Estate, which fell -1.47%, and Consumer Staples, which fell -1.06%. The top-performing subsectors were retail, materials, and semiconductors. Meanwhile, media, real estate, and foodstuffs were among the worst-performing. Southbound Stock Connect volumes were high as mainland investors bought a net $425 million worth of Hong Kong-listed stocks and ETFs, including Meituan, which was a moderate/large net buy, and CNOOC, and Xpeng, which were small net buys. Meanwhile, Tencent, HSBC, and Hong Kong Exchanges were small net sells.

Shanghai, Shenzhen, and the STAR Board gained +0.39%, +1.08%, and +0.98%, respectively, on volume that increased +0.18% from yesterday, which is 122% of the 1-year average. 3,363 stocks advanced, while 854 declined. The growth factor and large caps outperformed the value factor and small caps. The top-performing sectors were Technology, which gained +2.88%, Communication Services, which gained +1.79%, and Consumer Discretionary, which gained +0.54%. Meanwhile, Real Estate fell -0.9%, Utilities fell -0.72%, and Health Care fell -0.39%. The top-performing subsectors were computer hardware, software, and communication equipment. Meanwhile, education, chemicals, and diversified financials were among the worst-performing. Northbound Stock Connect volumes were high as foreign investors sold a net -$740 million worth of Mainland stocks, including Midea, Zijin Mining, and Ping An Insurance, which were small net buys. Meanwhile, LONGi Green Energy, broker East Money, and O-Film were moderate net sells. CNY and the Asia Dollar Index both fell slightly versus the US dollar. Treasury bonds fell. Copper gained, while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.20 versus 7.19 yesterday

- CNY per EUR 7.78 versus 7.77 yesterday

- Yield on 1-Day Government Bond 1.44% versus 1.45% yesterday

- Yield on 10-Year Government Bond 2.37% versus 2.34% yesterday

- Yield on 10-Year China Development Bank Bond 2.50% versus 2.46% yesterday

- Copper Price +0.25%

- Steel Price -0.18%