Premier Li’s Government Work Report Recap

3 Min. Read Time

Key News

Below are the key points from Premier Li’s government work report readout last night, which was attended by 5,100 delegates comprised of the National People's Congress (NPC) and the Chinese People's Political Consultative Conference (CPPCC), in Beijing for the “Two Sessions”:

- Premier Li acknowledged economic challenges and stated, “We have faced multiple challenges in the past year… after three years of the pandemic, the economic recovery has been difficult.”

- The 2024 GDP target is “around” 5% versus 2023’s 5.2%, which increased to RMB 126T from 2022’s RMB 114T and 2021’s RMB 114T

- Budget deficit of 3% versus 2023’s 3.8% and expectations between 3.2% and 3.5%

- Fiscal policy support includes RMB 1T ($139B) special Treasury bonds for “major national strategies” and RMB 3.9T ($541B) local government special bonds to offset the decline in land sales, which are identical amounts to 2023

- Plan to create 12 million new jobs

- The urban unemployment rate is expected to be 5.5% from 2023’s 5.2%

- CPI target of 3% as pork prices are expected to rise

- Reduce energy consumption per unit of GDP to 2.5%

- “A proactive fiscal policy should be moderately strengthened.”

- “A prudent monetary policy should be flexible, appropriate, and effective.”

- Key tasks include “expanding domestic demand, reforming the tax system, supporting EVs, biotech, and airplane manufacturing, while addressing risks in real estate."

The 3% budget deficit underwhelmed investors, though other measures met expectations. The cancellation of Premier Li’s post-Two Sessions Q&A is a disappointment. In his speech, he acknowledged the challenges China’s economy faces. Remember, the policies to achieve these goals will begin to be released. While there is no “policy bazooka,” which has some doubting these targets can be met, we will see further articulation of supportive measures soon. After the close, the National Development and Reform Commission (NDRC) published its draft of the 2024 National Economic and Social Development Plan. The draft focuses on “the prevention and control of major economic and financial risks,” which includes “the stable and healthy development of the real estate market” and “modern industrial system with technological innovation.” I am very interested in the domestic consumption focus and how it will be supported.

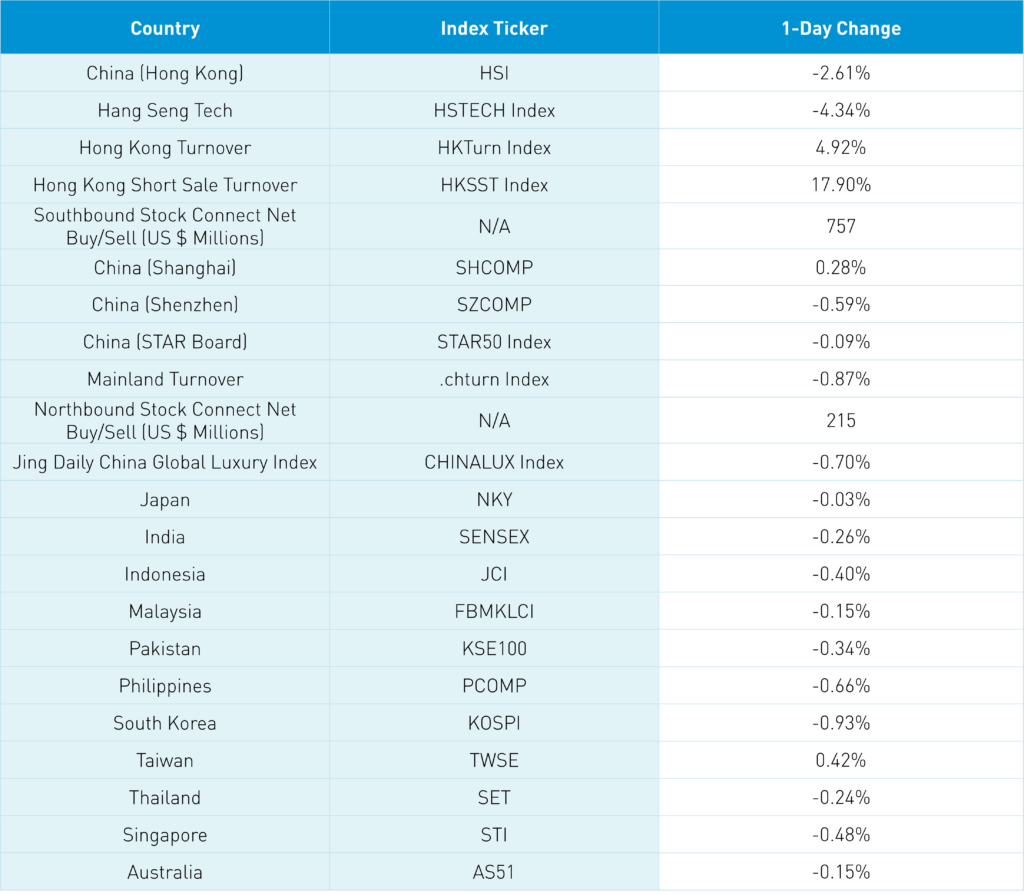

Asian equities were largely lower following an off day in the US. Mainland China overcame earlier losses as the National Team bought predominantly large/mega-cap Shanghai-listed stocks that kept indices positive. Two of their favorite ETFs, with tickers 510300 CH and 510310 CH, saw volume changes of 175% and 881% day-over-day. Volumes were high, though breadth (advancers versus decliners) was off. Hong Kong opened lower as buyers stayed on the sidelines.

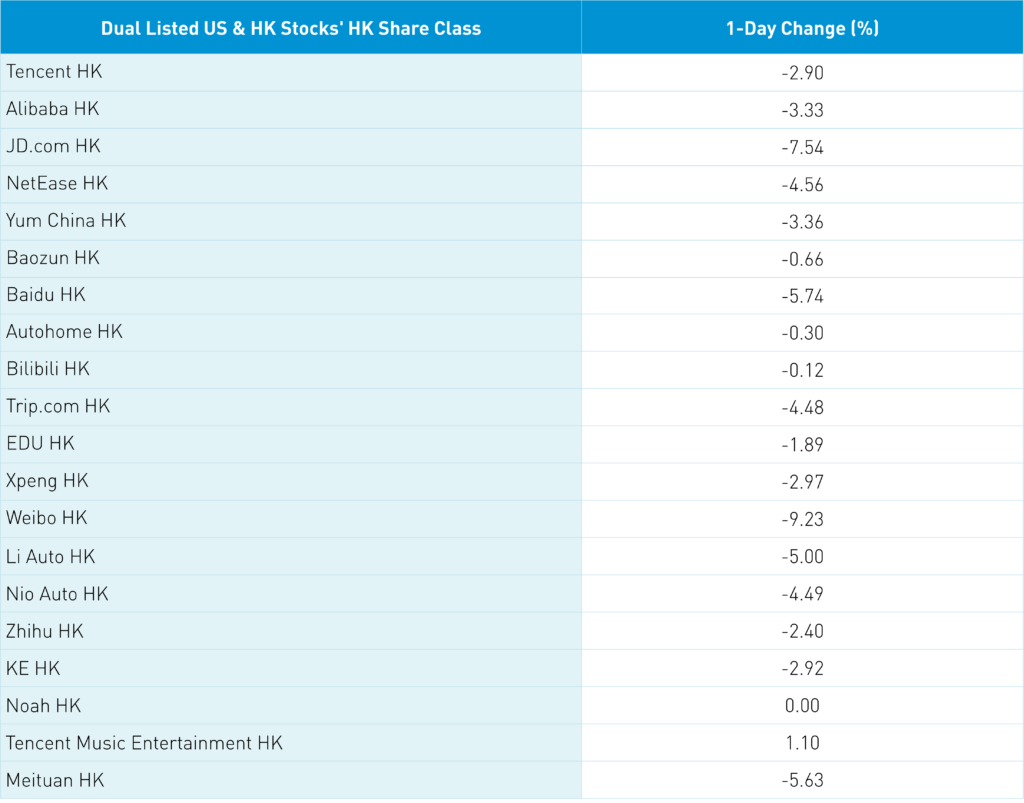

Mainland investors bought the dip via Southbound Stock Connect with a very healthy $757 million worth of net buying. Maybe they recognize that policy articulation should be a catalyst? Hong Kong short volumes jumped, though the Hong Kong Tracker ETF was the most heavily shorted security by value. This indicates a large buy into the ETF as market makers need to hedge by selling shares while they create more shares. Apple’s ecosystem fell on the reports their February sales were off, though the sales would be impacted by China’s New Year. Hard to buy a phone while in Thailand! With that said, Apple does face stiff local competition. NIO reported its earnings after the Hong Kong close as revenue beat estimates though adjusted net income and adjusted EPS missed.

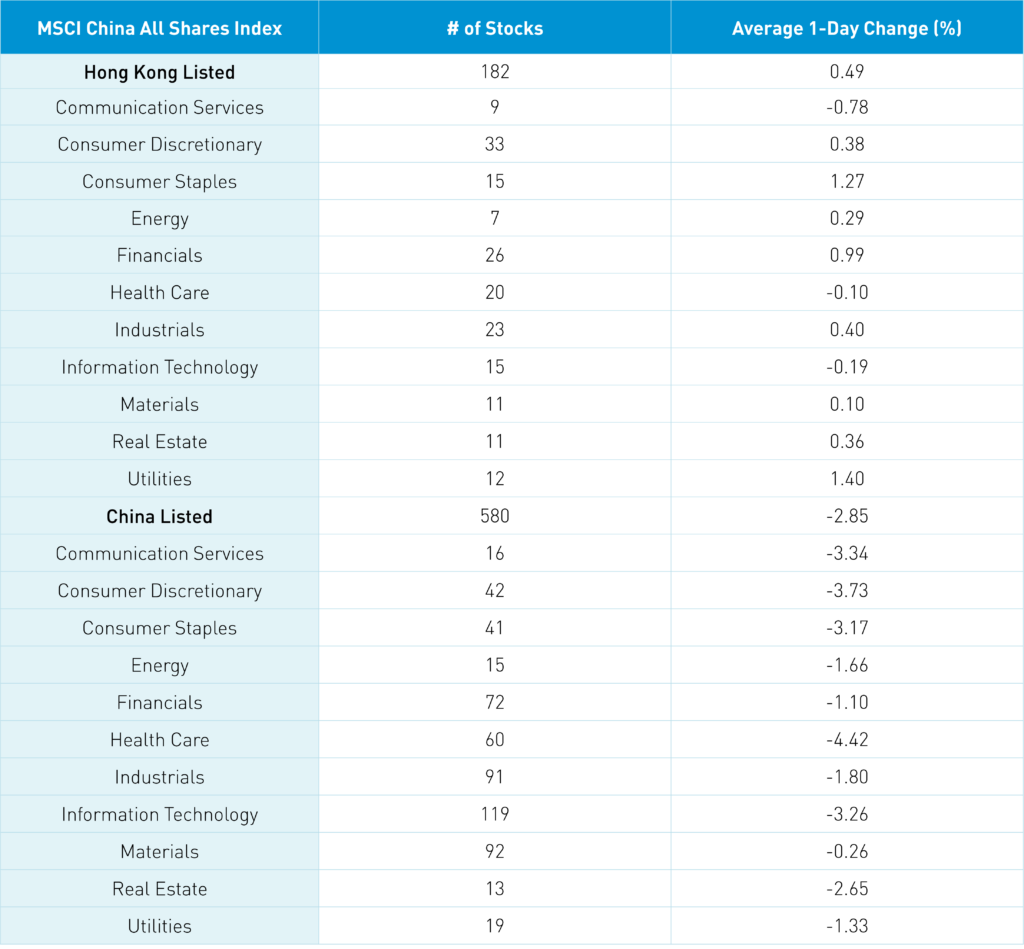

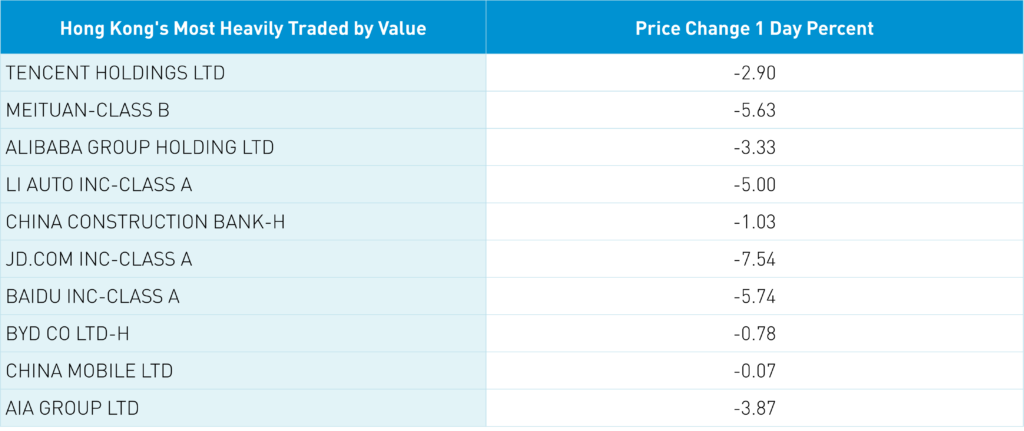

The Hang Seng and Hang Seng Tech indexes fell -2.61% and -4.34%, respectively, on volume that increased +4.92% from yesterday, which is 89% of the 1-year average. 44 stocks advanced, while 453 stocks declined. Main Board short turnover increased by +17.9% from yesterday, which is 132% of the 1-year average as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative though large caps and the value factor falling less than the small caps and the growth factor. All sectors were negative, including Health Care, which fell -4.42%, Consumer Discretionary, which fell -3.73%, and Communication Services, which fell -3.34%. All subsectors were negative too. Southbound Stock Connect volumes were moderate as Mainland investors bought a healthy $757 million worth of Hong Kong-listed stocks and ETFs, including Tencent, China Mobile, and CNOOC, which were moderate net buys. Meanwhile, China Shenhua, PetroChina, and Meituan were small net sells.

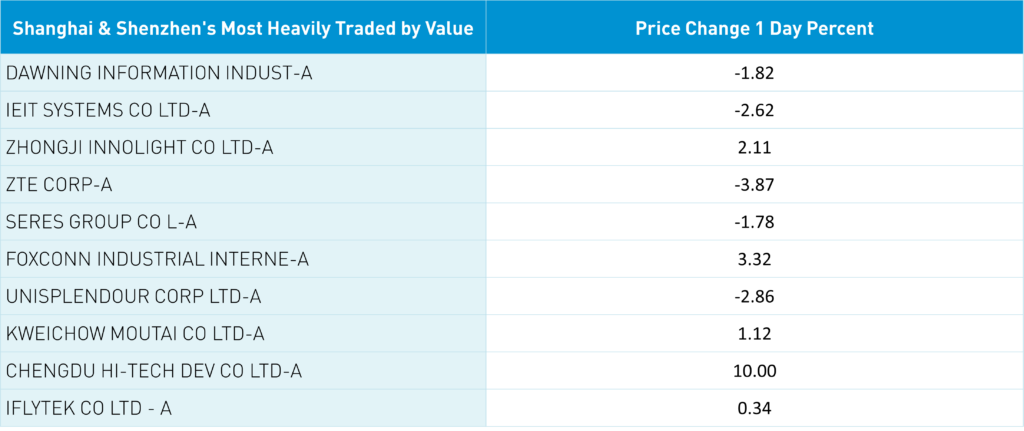

Shanghai, Shenzhen, and the STAR Board diverged to close +0.28%, -0.59%, and -0.09%, respectively, on volume that declined -0.87% from yesterday, which is 123% of the 1-year average. 898 stocks advanced, while 4,072 declined. Large caps and the value factor outperformed the growth factor and small caps. The top-performing sectors were Utilities, which gained +1.40%, Consumer Staples, which gained +1.27%, and Financials, which gained +0.99%. Meanwhile, Communication Services fell -0.78%, Technology fell -0.19%, and Health Care fell -0.1%. The top-performing subsectors were precious metals, motorcycles, and banking. Meanwhile, education, chemicals, and internet sectors were among the worst-performing. Northbound Stock Connect volumes were high as foreign investors bought a net $215 million worth of Mainland stocks, including Kweichow Moutai, Zhongji Innolight, and Cypc, which were moderate net buys. Meanwhile, Midea, LONGi Green Energy, and Mindray were small net sells. CNY was flat versus the US dollar. Treasury bonds rallied. Copper gained while steel fell.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.20 yesterday

- CNY per EUR 7.81 versus 7.82 yesterday

- Yield on 10-Year Government Bond 2.31% versus 2.35% yesterday

- Yield on 10-Year China Development Bank Bond 2.42% versus 2.48% yesterday

- Copper Price +0.26%

- Steel Price -0.11%