Bilibili & Full Truck Alliance Beat Expectations, WuXi Hit By Potential US Policy

5 Min. Read Time

Key News

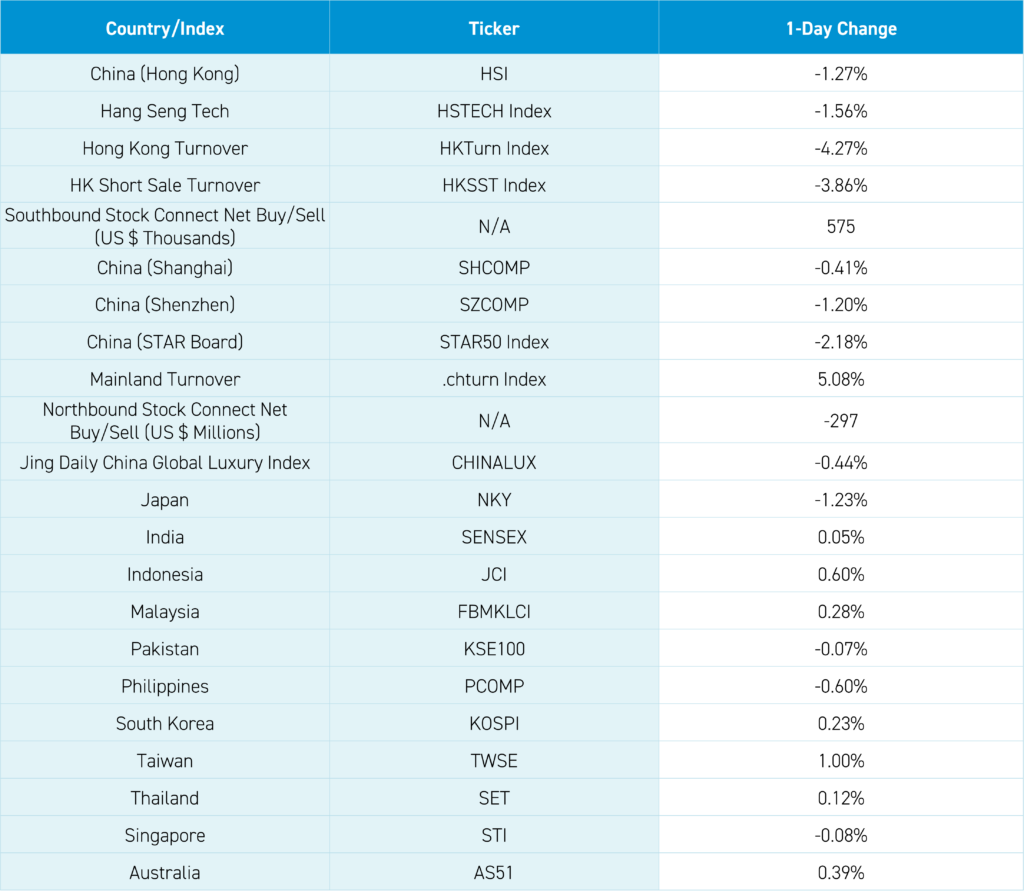

Asian equities were largely higher except for Japan, China, and Hong Kong. It was a fairly quiet night as the "Two Sessions" important policy meetings in China roll on.

February Export/Import data beat expectations. Exports increased by +7.1% year-to-date (YTD) versus last year versus an expected increase of only +1.9%. Meanwhile, imports increased +3.5% versus an expected +2%. This is a promising sign for the global economy!

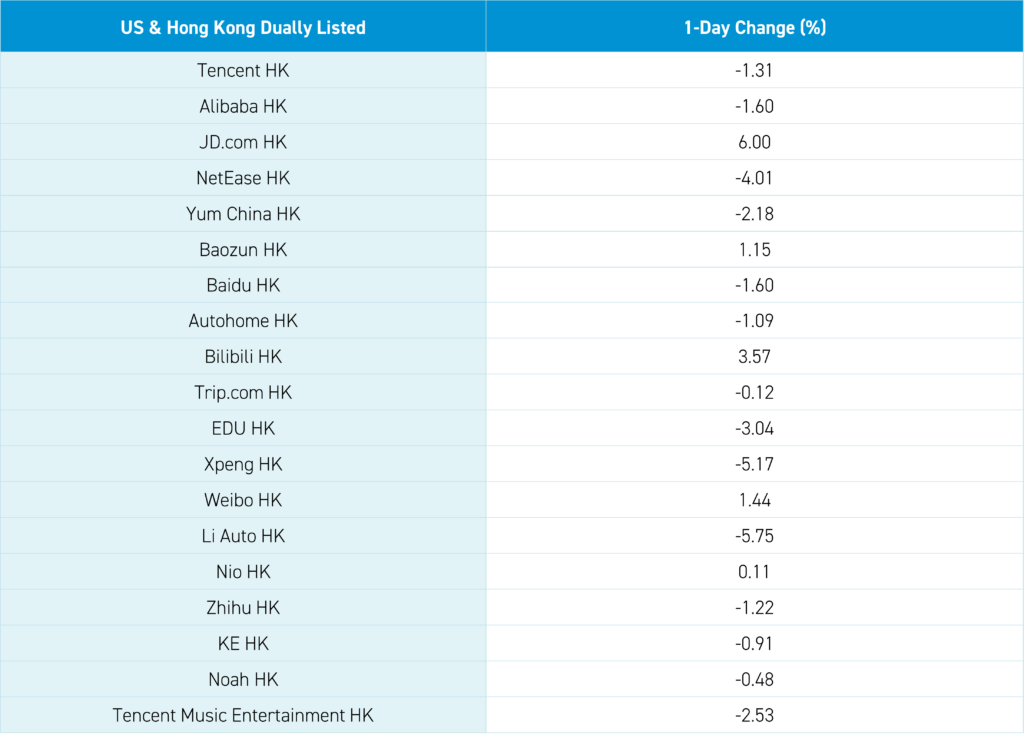

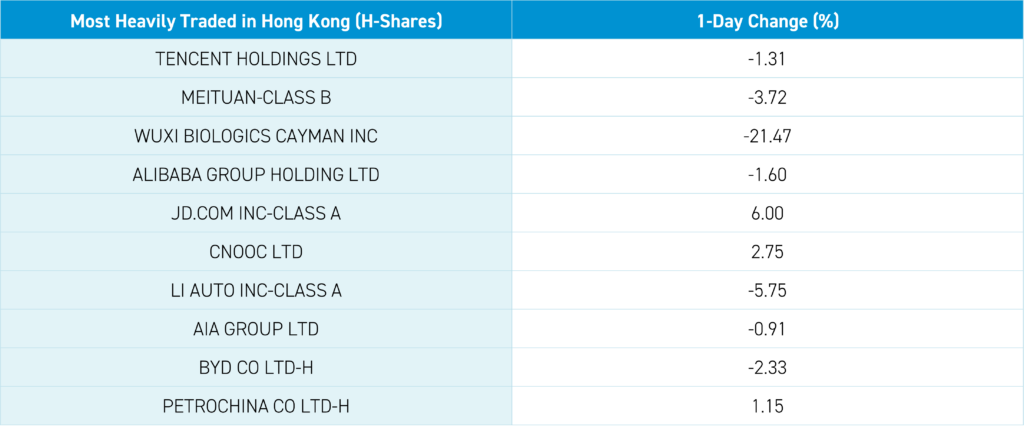

JD.com gained +6% in Hong Kong after reporting great results yesterday. Hong Kong and Mainland China slipped in afternoon trading as several macroeconomic headlines weighed on investor sentiment.

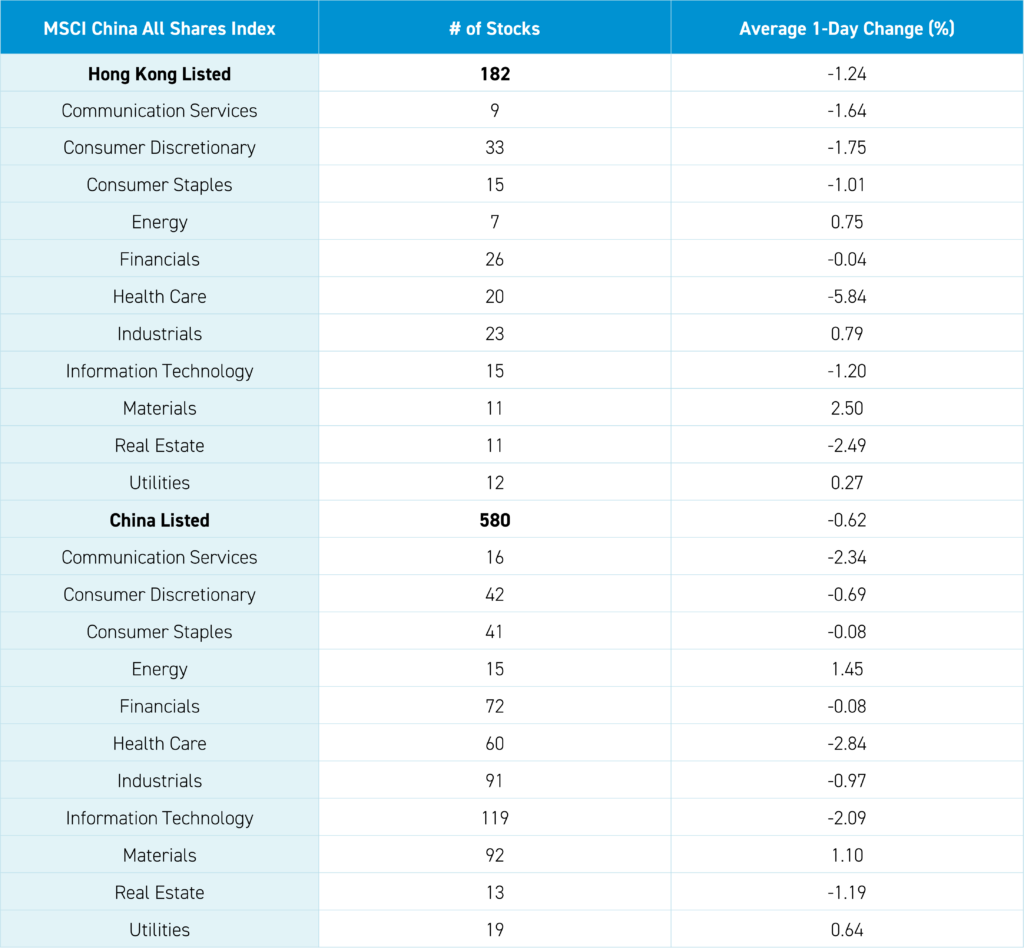

Health care was the worst-performing sector in both Hong Kong and Mainland China, falling -5.83% and -2.81% in each market, respectively, as a US Senate advanced a bill that would bar Chinese biotech companies from doing business with health care providers that accept medicaid and medicare. However, as discussed below, it has a LONG way to go before coming law. Meanwhile, concerns about EU tariffs on Chinese electric vehicles (EVs) weighed on the ecosystem in both Hong Kong and Mainland China. Foreign Minister Wang Yi’s press conference noted the increase in US government actions against China despite progress made at APEC. The market lacked a catalyst to overcome the negative headlines that weighed on sentiment.

After the Hong Kong close, Bilibili and Full Truck Alliance reported their Q4 financial results, discussed below. The National Team likely intervened in the afternoon as two of their favorite ETFs saw spikes in volume during the afternoon dip, indicating the continued effort to stabilize the market. Mainland investors bought the dip in Hong Kong via Southbound Stock Connect, as Tencent posting its third net buying day via Southbound Stock Connect, though, yes, it was a small amount. Tencent has seen net selling year to date.

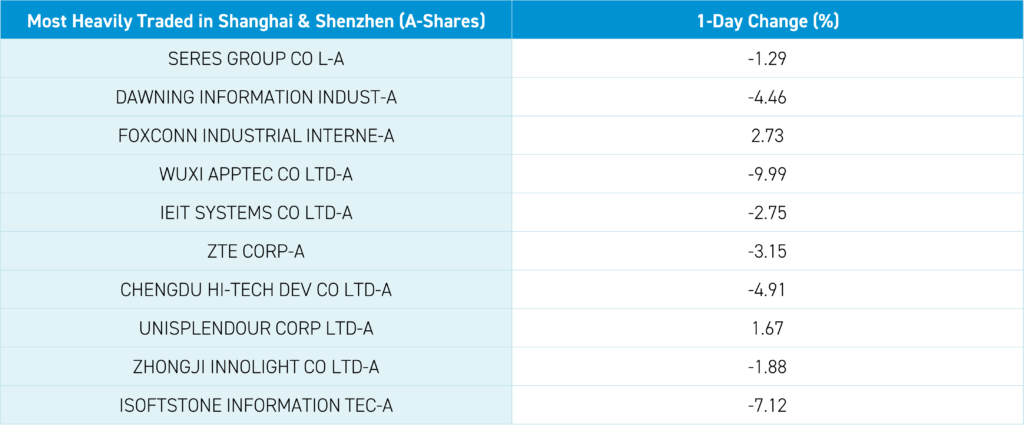

The US Senate Homeland Security Committee passed a bill that would bar WuXi Biologics, WuXi AppTec, and other Chinese biotech companies from doing business with US government-funded healthcare providers to prevent the companies from sending US citizens’ DNA data to the Chinese government. That’s not a typo! The bill has a long way to go before it is law, as the House and Senate would have to pass it, and then the President has to sign it into law. The Wuxi companies are domiciled in the Cayman Islands and have facilities pretty much everywhere (the US, Ireland, Germany, etc.).

Despite this, WuXi Biologics (2269 HK) fell -21.47% and WuXi AppTec (2359 HK) fell -20.56% overnight due to their high US revenue exposure. WuXi AppTec’s seven largest shareholders include six US asset managers, according to the latest SEC 13F data. Those six US asset managers’ shareholders lost $231 million today based on their ownership of 154 million shares! Since January 24th, those six US asset managers’ shareholders have lost $693 million on the US Congress' actions! Many US asset managers own the shares, and I don’t have time to calculate them. WuXi AppTec has denied the allegations against it while employing thousands of Americans in its US facilities. It hasn’t sued, which it should, in my opinion.

One must wonder how much of Apple’s recent China market share loss is a consequence of US restrictions on Huawei, which forced the company to innovate and become a formidable opponent. Today’s Wall Street Journal has an article on China’s push for technology independence. Gee, I wonder why? The article briefly acknowledges that the actions result from recent US policies restricting their technology purchases and the US government's spying on China, as revealed by Edward Snowden.

Bilbili Earnings Highlights

Bilibili (BILI US, 9626 HK) calls itself “an iconic brand and a leading video community for young generations in China.” The company allows users, particularly those who enjoy video games, to make videos, watch others play video games, and participate in online group videos. The company released Q4 financial results after the Hong Kong close/US market open. % changes are year-over-year.

- Revenue increased +3% to RMB 6.3B from RMB 6.142B in Q4 2022 versus expectations of RMB 6.322B

- Adjusted net loss declined -58% to RMB 555.8 million versus an expected loss of RMB -632 million

- Adjusted EPS indicated a loss of RMB 1.34, up from a loss of RMB -3.31 in Q4 2022, versus an expected loss of RMB 1.43

- Average daily users increased +8% to 100 million

Full Truck Alliance Earnings Highlights

Full Truck Alliance (YMM US), a “leading digital freight platform,” i.e., the Uber for trucks/shipping in China, released Q4 financial results after the Hong Kong close and before the US market open. % changes are year-over-year.

- Revenue increased +25.3% to RMB 2.408B from RMB 1.922.5B versus expectations of RMB 2.408B

- Adjusted net income increased +64.4% to RMB 733B from RMB 195.7B versus expectations of RMB 636 million.

- Adjusted EPS RMB 0.69 from RMB 0.42Q1 revenue forecast between RMB 2.11B and RMB 2.16B, representing a YoY growth rate of 23.9% to 27.1%.

- The company had repurchased 30.7 million ADRs at a cost of $200 million. The board approved a repurchase program of $500 million.

The Hang Seng and Hang Seng Tech indexes fell -1.27% and -1.56%, respectively, on volume that decreased -4.27% from yesterday, which is 99% of the 1-year average. 153 stocks advanced, while 316 declined. Main Board short turnover declined -3.83% from yesterday, 87% of the 1-year average, as 15% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. The top-performing sectors were Materials, which gained +2.5%, Industrials, which gained +0.79%, and Energy, which gained +0.74%. Meanwhile, Health Care fell -5.84%, Real Estate fell -2.49%, and Consumer Discretionary fell -1.76%. The top-performing subsectors were materials, energy, and capital goods. Meanwhile, pharmaceutical/biotech, auto, and media were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $575 million worth of Hong Kong-listed stocks and ETFs, including CNOOC, which was a large net buy, and Bank of China and WuXi Biologics, which were moderate net buys. Meanwhile, PetroChina, Meituan, and China Mobile were small net sells.

Shanghai, Shenzhen, and the STAR Board fell -0.41%, -1.20%, and -2.18%, respectively, on volume that increased +5.08% from yesterday, which is 113% of the 1-year average. 1,489 stocks advanced while 3,386 declined. The value factor and large caps outperformed the growth factor and small caps. The top-performing sectors were Energy, which gained +1.45%, Materials, which gained +1.1%, and Utilities, which gained +0.64%. Meanwhile, Health Care fell -2.84%, Communication Services fell -2.34%, and Technology fell -2.09%, making up the worst-performing sectors. The top-performing subsectors were precious metals, steel, and oil & gas. Meanwhile, computer hardware, pharmaceuticals, and software were among the worst-performing. Northbound Stock Connect volumes were moderate/high as foreign investors sold a net -$297 million worth of Mainland stocks, including Kweichow Moutai, Cypc, and ZTE, which were small net buys. Meanwhile, CATL, WuXi AppTec, and Sokon were small net sells. CNY was flat versus the US dollar. Treasury bonds fell while copper and steel gained.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.84 versus 7.82 yesterday

- Yield on 10-Year Government Bond 2.27% versus 2.26% yesterday

- Yield on 10-Year China Development Bank Bond 2.38% versus 2.36% yesterday

- Copper Price +0.54%

- Steel Price +0.19%