“Two Sessions” Drives Technology & Healthcare Rally, Defending PDD & TikTok, Week in Review

5 Min. Read Time

Week in Review

- Asian equities were mostly higher this week as Taiwan outperformed the region, and Mainland China outperformed Hong Kong, which was lower.

- JD.com, Full Truck Alliance, and Bilibili all reported Q4 earnings this week that were significantly ahead of analysts’ expectations.

- Shares of contract medical research firms WuXi Biologics and WuXi AppTec were volatile again this week as a Senate Committee advanced a bill that would prohibit US healthcare providers from employing their services if they accept Medicaid and Medicare, though it remains unlikely that the proposal will become a law.

- China’s “Two Sessions” important policy meetings continued all week and included a positive press conference from the heads of various financial oversight agencies.

Friday's Key News

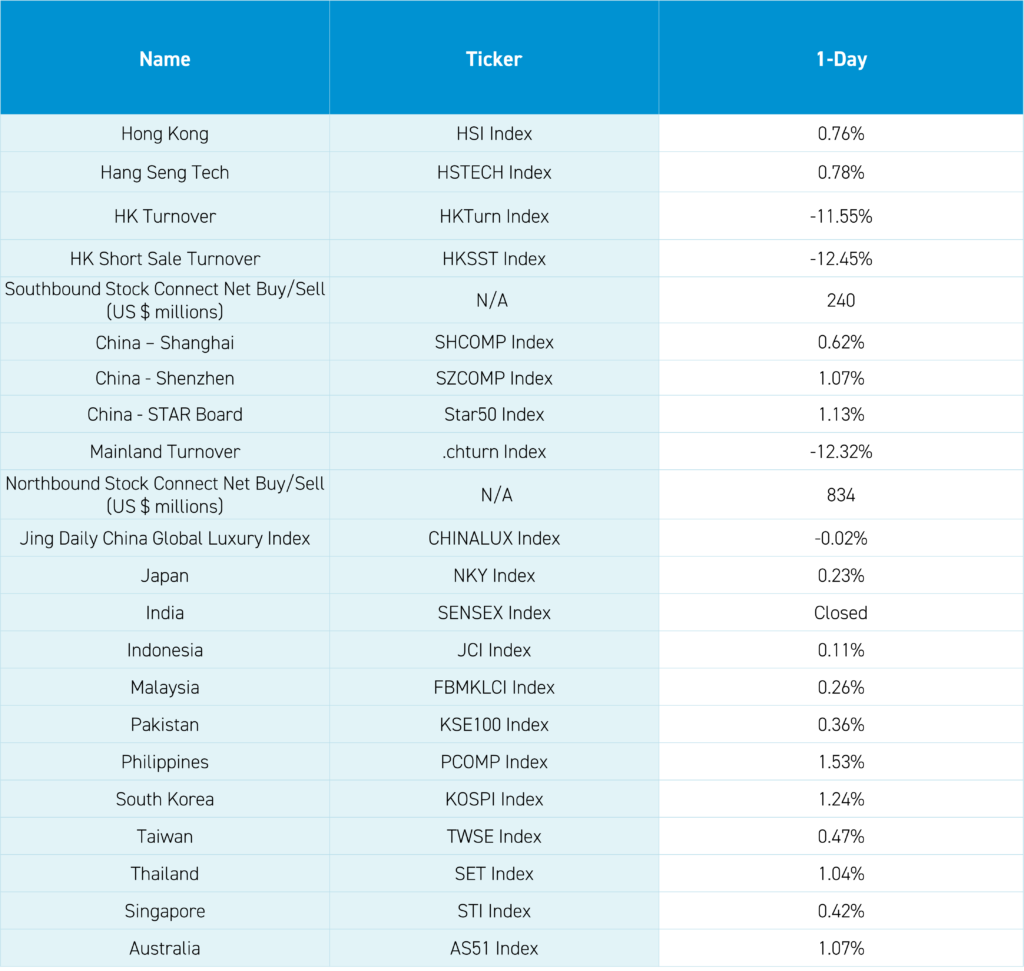

Asian equities cheered Fed Chair Powell’s testimony, as South Korea outperformed while India was closed for Mahabharat, “the Great Night of Shiva,” a significant Hindu festival celebrated annually in honor of Lord Shiva.

Mainland China and Hong Kong posted gains on decent breadth and volume. News coming from the “Two Sessions” was likely a factor in today’s trading. Technology outperformed in Mainland China, where it gained +3.29%, and Hong Kong, where it gained +3.14%. The Ministry of Industry and Information Technology (MIIT) Minister Jin Zhuanglong stated that China needs to “advance the construction of 5G, computing power and other information facilities.” It would be easy to say the government is reacting to US export bans by supporting local players at the expense of Western companies, though the release did not mention the US.

Healthcare jumped in Mainland China, where it gained +0.26%, and Hong Kong, where it gained +1.77%, as the Minister of Civil Affairs Lu Zhiyuan spoke on “how to deal with the aging population” with policies coming to “improve social security… improve elderly care service system… improve the health support system…” He acknowledged that 21.1% of the population (297 million people) are over the age of 60, and 15.4% (217 million) are over the age of 65 versus the US 21.47%. Wuxi Biologics gained +2.11%, and Wuxi AppTec gained +4.00% as traders realized the proposed ban is far from law and, I assume, would be challenged in court. I expect we will also see policies announced to address China’s low birth rate.

Luo wen, the Director of General Administration for Market Regulation, spoke on leveling the playing field and opening markets for foreign companies operating in China.

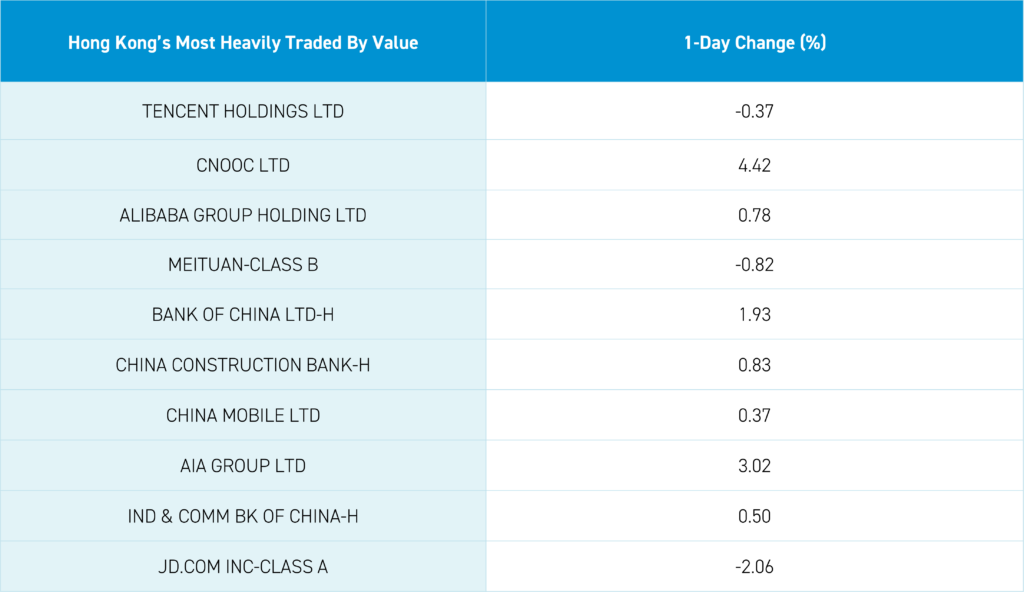

Hong Kong’s most heavily traded stocks were Tencent, which fell -0.37% despite seeing its fourth straight day of net buying by Mainland investors via Southbound Stock Connect, energy giant CNOOC, which gained +4.42%, Alibaba, which gained +0.78%, Meituan, which fell -0.82%, and the Bank of China, which gained +1.93%. Mainland investors bought a net $240 million worth of Hong Kong-listed stocks and ETFs, which is a decent amount. Mainland China had a good day as well, with no signs of the National Team, though Northbound Stock Connect volumes were high, with a healthy $843 million worth of net buying. The two Mainland-invested China equity ETFs favored by the National Team had light volume today, indicating a lack of National Team intervention. China will report the consumer price index (CPI) and the producer price index (PPI) today. The inflation gauges are expected to be 0.30% and -2.5%, respectively. I expect a higher CPI as hog prices, which make up a significant percentage of China’s CPI, have increased in February. Hog futures prices on the Dalian Commodity Exchange fell from 16,500 a year ago to only 14,355 in early February, but have rebounded to 15,095.

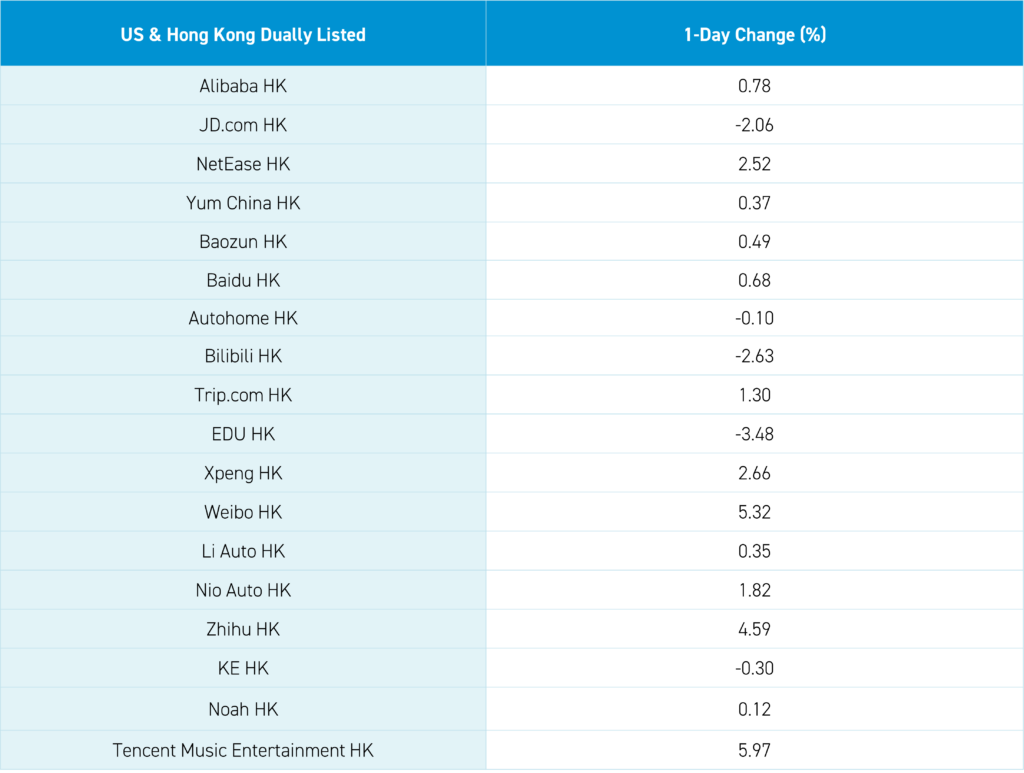

Congress’ TikTok ban is great entertainment, but there is a little thing called the First Amendment. I assume it will pass, get challenged in court, and subsequently be thrown out. This is typical DC theater. Should China view Apple, GM, Exxon Mobil, Starbucks, Boeing, Caterpillar, etc., as foreign adversaries? More importantly, do you want Washington, DC, to help you parent? I despise social media apps, but it is my choice if I let my kids use them.

I absolutely loved CNBC’s interview with Cisco CEO and Business Roundtable Chuck Robbins, who stated US tariffs are hurting US manufacturers because the inputs are made in China. Therefore, US manufacturers are moving out of the US due to the tariffs! So much for the “bring it all back” onshoring. Has DC ever been so disconnected from the business world?

The Financial Times had an article earlier this week on PDD that accused the company of fraud. The article questions the company's accounting, financial statements, and growth. The company’s auditor is Ernst & Young (EY). There has clearly been a misunderstanding of the company’s business, which is reflected in the article’s nonsensical comparison to eBay. PDD’s historical lack of communication is driven by the founder’s engineering background, though there are signs of improvement. The Financial Times author failed to utilize third-party data providers to verify PDD’s numbers. As we have mentioned in the past, apps sell users’ data and screen scrape websites to measure how many goods are being sold, including e-commerce apps in China. Questmobile, SensorTower, YipitData, and BigOne Lab are a few of the players that aggregate and sell the data to foreign investors, though clearly not to the FT. Having viewed this data, I can tell you PDD has done very well in China, based on metrics such as daily and monthly users, the number of users who have downloaded their app, and time spent on their app. Several of the article’s negatives against the company were the result of US regulations, such as the SEC requiring the company not to report gross merchandise value (GMV), not listing in Hong Kong after China changed its law to allow audit reviews, the move to a Dublin domicile, which was driven by US regulatory scrutiny versus being domiciled in China. To me, the article is more about why we should be diversified and the risks of single-stock investing.

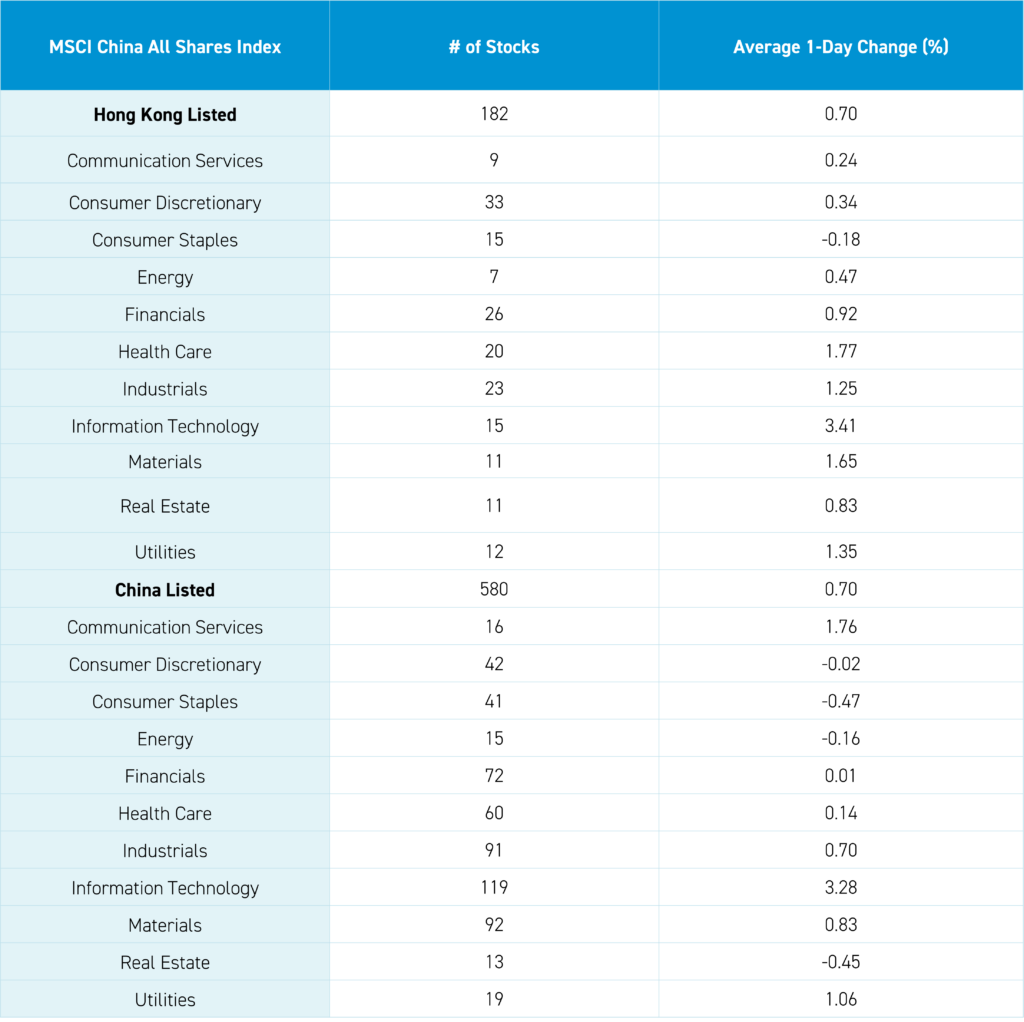

The Hang Seng and Hang Seng Tech indexes gained +0.76% and +0.78%, respectively, on volume that declined -11.55% from yesterday, which is 88% of the 1-year average. 353 stocks advanced, while 122 declined. The Main Board short turnover declined -12.44% from yesterday, which is 76% of the 1-year average, as 15% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps outperformed the growth factor and large caps. The top-performing sectors were Technology, which gained +3.41%; Healthcare, which gained +1.77%; and Materials, which gained +1.65%. Meanwhile, Consumer Staples fell -0.18%. The top-performing subsectors were media, semiconductors, and consumer durables. Meanwhile, food, software, beverages, and tobacco were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $240 million worth of Hong Kong-listed stocks and ETFs, including Tencent, which was a small net buy, the Bank of China, and CNOOC.

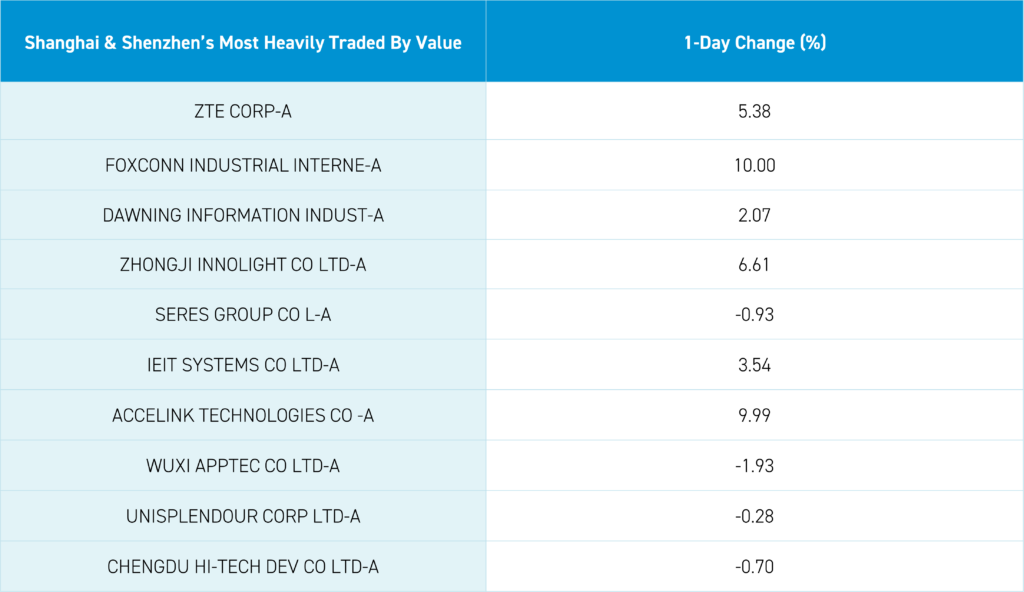

Shanghai, Shenzhen, and the STAR Board gained +0.62%, +1.07%, and +1.13%, respectively, on volume that decreased -12.32% from yesterday, which is 99% of the 1-year average. 3,479 stocks advanced, while 1,340 declined. The growth factor and small caps outperformed the value factor and small caps. The top-performing sectors were Technology, which gained +3.29%, Communication Services, which gained +1.77%, and Utilities, which gained +1.06%. Meanwhile, Consumer Staples fell -0.46%, Real Estate fell -0.45%, and Energy fell -0.15%. The top-performing subsectors were power generation equipment, communication equipment, and computer hardware while catering tourism, office supplies, and coal were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors bought a net $843 million worth of Mainland stocks, including Sungrow Power, Zijin Mining, and LONGi Green Technology. Meanwhile, Kweichow Moutai was a large net sell, and China Merchants Bank and CATL were small net sells. The Asia Dollar Index gained versus the US dollar while CNY was flat. Treasury bonds fell. Copper gained, while steel gave back some of its recent gains.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.87 versus 7.87 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.47% yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.39% versus 2.38% yesterday

- Copper Price +0.73%

- Steel Price -0.51%