Q4 Results from XPeng, TME, and Tongcheng Travel

4 Min. Read Time

Key News

Asian equities were mainly lower on light volumes.

Japan, after the week’s first widely watched central bank meeting, saw the Bank of Japan raise interest rates to 0.1% from 0% for the first time in seventeen years. Meanwhile, Hong Kong and Mainland China both fell as investors wait for additional interest rate guidance from the US Fed, ECB, and Bank of England this week.

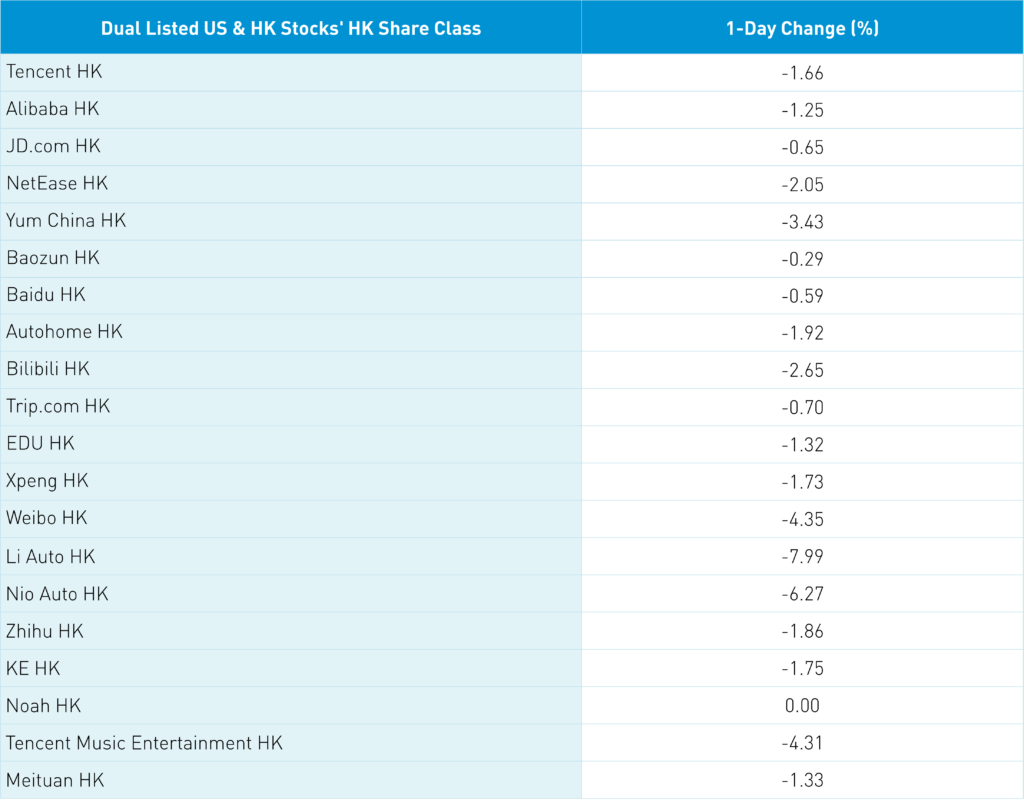

Li Auto was down -7.99% on an analyst downgrade as their new MEGA minivan release resulted in fewer orders than expected, weighing on the EV ecosystem. After the Hong Kong close and before the US market opened, XPeng missed revenue expectations of RMB 13.28B, with reported revenues of RMB 13.05B, but narrowed its loss better than expected. Nvidia added XPeng, BYD, and GAC Aion, along with the previously announced Li Auto and Zeekr, as clients to their new "Drive Thor" centralized car computer, according to Yicai.

While Hong Kong-listed internet stocks were lower. Tencent Music Entertainment reported Q4 financial results after the Hong Kong close and prior to the US market opening, beating on revenue, adjusted net income, and adjusted EPS.

Online travel agency Tongcheng Elong Travel also reported earnings after the Hong Kong market closed, with Q4 results that beat on revenue, adjusted net income, and adjusted EPS.

JD.com was down -0.63%, but the company should benefit from the new policy support geared towards household appliance trade-ins and upgrades, a direction laid out during last week's "Two Sessions" policy meetings.

Wuxi AppTec was down -7.49% on a disappointing 2024 outlook as the healthcare sector underperformed in both Hong Kong and Mainland China. It is important to note that 65% of Wuxi's revenue generated in the US is threatened by Congressional action. The lack of Western media coverage of what’s occurring to this company seems very unusual as Congress acts as judge, jury, and executioner of a company while providing ZERO evidence.

Real estate underperformed as the CSRC accused Evergrande of fraud. Remember, real estate is now a tiny sector, having been kicked out of most indices. Evergrande’s US Dollar bond due in 2025 fell -$0.01 to $1.74, though off its Jan 31 low of $1.03.

LONGi Green Energy was down -2.4% after announcing layoffs due to overcapacity in solar.

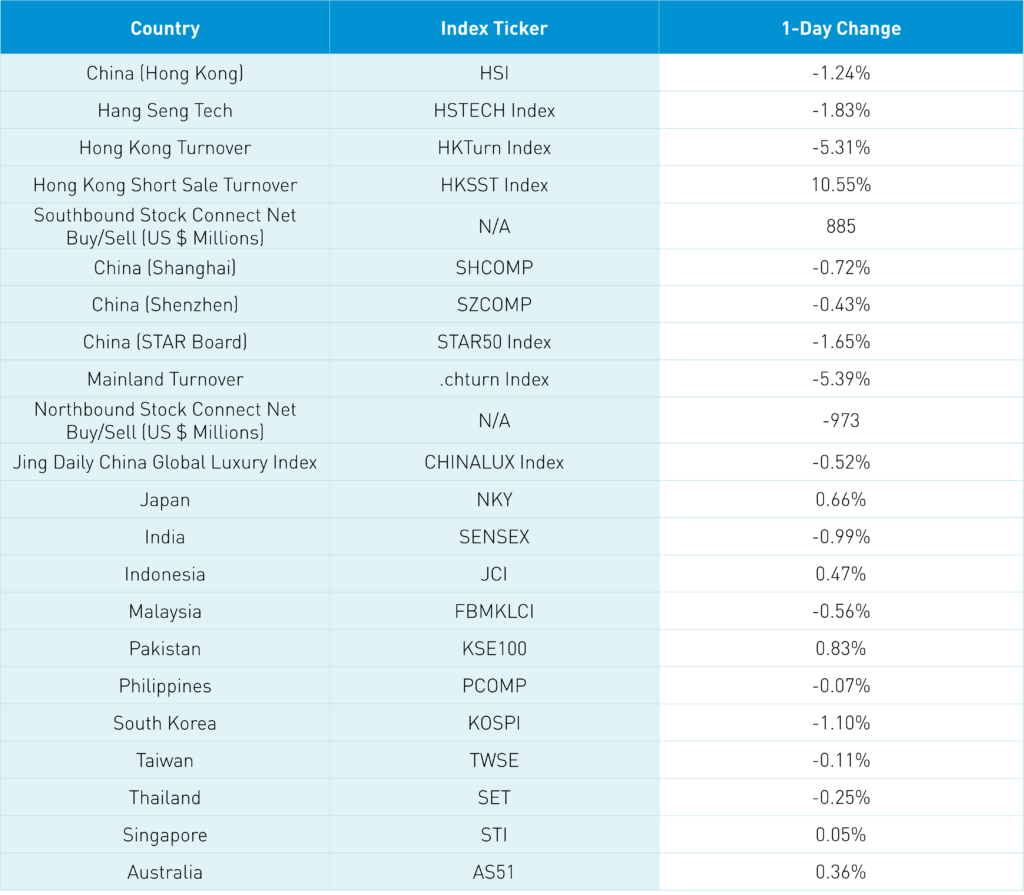

Mainland investors bought the Hong Kong dip, buying a healthy $885mm of Hong Kong stocks via Southbound Stock Connect. Foreign investors sold a healthy -$885mm of Mainland stocks via Northbound Stock Connect. The National Team took the day off as their two favorite ETFs saw light volumes though both saw volume spikes as the Mainland market fell in the afternoon.

The widely followed Bank of America Fund Manager Survey states the two most popular/crowded trades are long the US tech Magnificent 7 and short China. It is interesting that after January’s China derivative-induced meltdown, there remains little interest despite the market’s rally from the lows. A Mainland China/Hong Kong stock grind higher is fine by me.

Tomorrow morning will be busy with Tencent, Kuaishou, and Pinduoduo reporting Q4 financial results. Here's what to watch for:

Tencent – Q4 Revenue growth estimate implies 9% growth YoY.

- Revenue in Q4 2022 was RMB 144.9B, and expectations for this quarter are RMB 157B

- Adjusted Net income in Q4 2022 was RMB 29.7B, and expectations for this quarter are RMB 41.9B

- Adjusted EPS in Q4 2022 was RMB 3.04, and expectations for this quarter are RMB 4.45

Pinduoduo – Q4 Revenue growth estimate implies 101% growth YoY.

- Revenue in Q4 2022 was RMB 130.5B, and expectations for this quarter are RMB 79.8B

- Adjusted Net income in Q4 2022 was RMB 12.1B, and expectations for this quarter are RMB 16.7B

- Adjusted EPS in Q4 2022 was RMB 8.34, and expectations for this quarter are RMB 11.28

Kuaishou – Fiscal Year 2023 is on track to be the company’s first profitable/positive year on both adjusted net income and adjusted EPS; the Q4 revenue growth estimate implies 15% growth YoY.

- Revenue Q4 2022 RMB 28.3B and expectations of RMB 32.6B

- Adjusted Net income Q4 2022 RMB loss -45mm and expectations of RMB 3.2B

- Adjusted EPS Q4 2022 RMB loss -0.01 and expectations of RMB 0.70

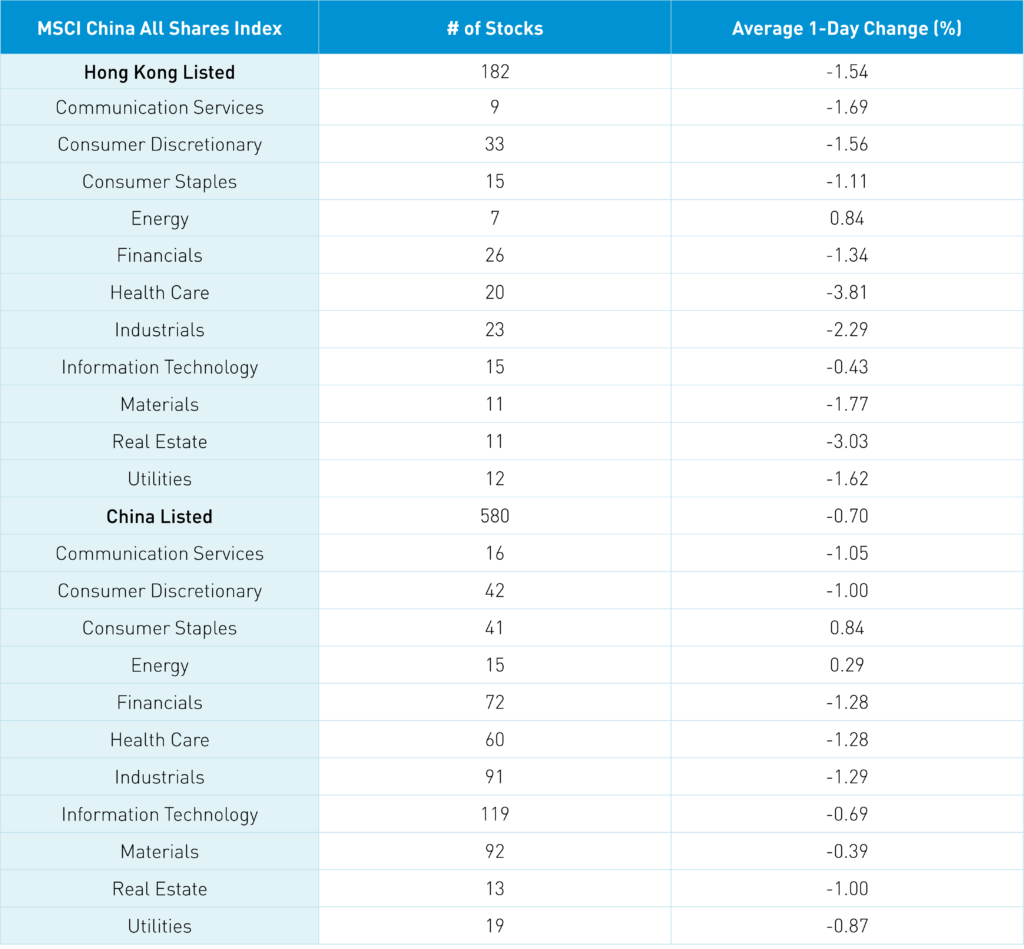

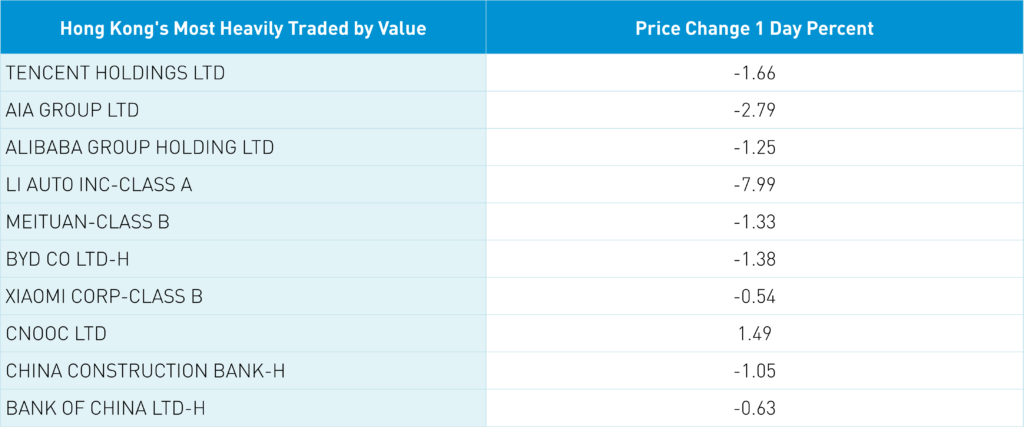

The Hang Seng and Hang Seng Tech indexes fell -1.24% -1.83%, respectively, on volumes that decreased -5.31% from yesterday, which is 92% of the 1-year average. 88 stocks advanced, while 405 declined. Main Board short turnover increased by +10.55% from yesterday, which is 105% of the 1-year average, as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, as the growth factor underperformed the value factor. Energy was the only positive sector, gaining +0.83%. Meanwhile, Health Care fell -3.82%, Real Estate fell -3.03%, and Industrials fell -2.3%. Energy and foodstuffs were the only positive subsectors. Meanwhile, media, pharmaceuticals, and autos were the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a healthy net $885 million worth of Hong Kong-listed stocks and ETFs, including the Bank of China, Tencent, and Li Auto, which were moderate net buys. Meanwhile, Kuaishou, China Construction Bank (CCB), and Meituan were slightly sold on a net basis.

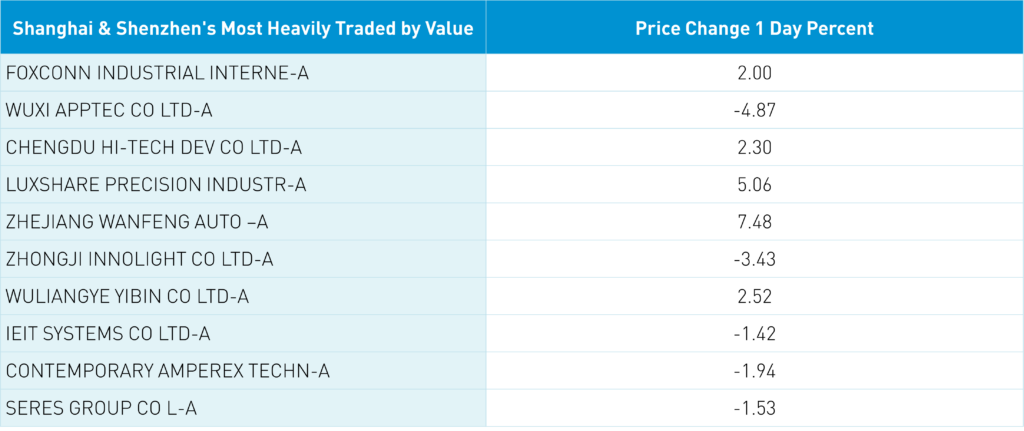

Shanghai, Shenzhen, and the STAR Board fell -0.72%, -0.43%, and -1.65%, respectively, on volume that decreased -5.39% from yesterday, which is 124% of the 1-year average. 2,078 stocks advanced, while 2,785 declined. All factors were negative, as the growth factor fell less than the value factor. Consumer Staples and Energy gained +0.83% and +0.28%, respectively. Meanwhile, Industrials fell -1.29%, and Health Care and Financials both fell -1.28%. The top-performing subsectors were agriculture, coal, and chemicals. Meanwhile, motorcycles, energy equipment, and computer hardware were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$973 million worth of Mainland stocks, including Midea, Wuliangye, and CATL. Meanwhile, Wuxi AppTec was a large net sell, BYD was a moderate net sell, and LONGi Green Technology was a small net sell. CNY and the Asia dollar index were off slightly versus the US dollar. Treasury bonds rallied while copper and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.20 yesterday

- CNY per EUR 7.80 versus 7.84 yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.39% versus 2.41% yesterday

- Copper Price +0.27%

- Steel Price +2.04%