Tencent, Pinduoduo & Kuaishou Q4 Results Review!

5 Min. Read Time

Tencent Q4 Review

- Q4 2023 Revenue and adjusted EPS slightly missed, but otherwise, a strong quarter with management keeping costs down and rewarding shareholders with a large dividend and buyback.

- Revenue increased by +7% to RMB 155.1B from Q4 2022’s RMB 144.9B and expectations of RMB 157B

- Revenue from value-added services (i.e. games) declined by -2% to RMB 69.079B from RMB 70.147B

- Revenue from online advertising increased +21% to RMB 29.8B from 24.66B

- Revenue from FinTech/Business Services increased +15% to RMB 54.4B from RMB 47.244B

- Adjusted Net income increased +44% to RMB 42.6B from Q4 2022 RMB 29.7B and expectations of RMB 41.9B

- Adjusted EPS increased +46% to RMB 4.44 from Q4 2022 RMB 3.04 and expectations of RMB 4.45

- Increased dividend +43% to HK $ 3.40 from 2022’s HK $ 2.40

- Doubling stock repurchase plan to HK $ 100B from 2023’s HK $ 49B

PDD Q4 Review

- PDD absolutely crushed earnings estimates, though it is interesting that there was no breakout of Temu’s results.

- Revenue increased by +123% to RMB 88.881B from Q4 2022's RMB 130.5B and expectations of RMB 79.8B

- Revenues from online marketing services increased by 57% to RMB 48.675B from RMB 31.023B

- Revenues from transaction services increased by +357% to RMB 40.205B from RMB 8.796B

- Adjusted Net income increased by 110% to RMB 25.476B from Q4 2022's RMB 12.1B and expectations of RMB 16.7B

- Adjusted EPS increased to RMB 17.32 from Q4 2022's RMB 8.34 and expectations of RMB 11.28

Kuaishou Q4 Review

- Similar to Bytedance/TikTok, the online video content provider has delved into E-Commerce with its 382 million daily users. Fiscal Year 2023 is the company’s first profitable/positive year on both adjusted net income and adjusted EPS. Revenue was a very slight miss, though both adjusted net income and adjusted EPS beat.

- Revenue increased by +15.1% to RMB 32.5B from Q4 2022's RMB 28.3B and expectations of RMB 32.6B

- Online marketing revenue increased by +20.6% to RMB 18.2B from Q4 2022’s RMB 15B

- Live streaming revenue was flat at RMB 10.048B from Q4 2022’s RMB 10.034B

- Adjusted Net income increased to RMB 4.3B from Q4 2022's RMB loss -45mm and expectations of RMB 3.2B

- Adjusted EPS was RMB 0.95 from Q4 2022's RMB loss -0.01, and expectations of RMB 0.70

- Purchased back 51mm shares in 2023, spending HK $2.551B

Asian equities were largely higher on light volumes in advance of today’s US Fed interest rate update, while Japan was on holiday for the Vernal Equinox.

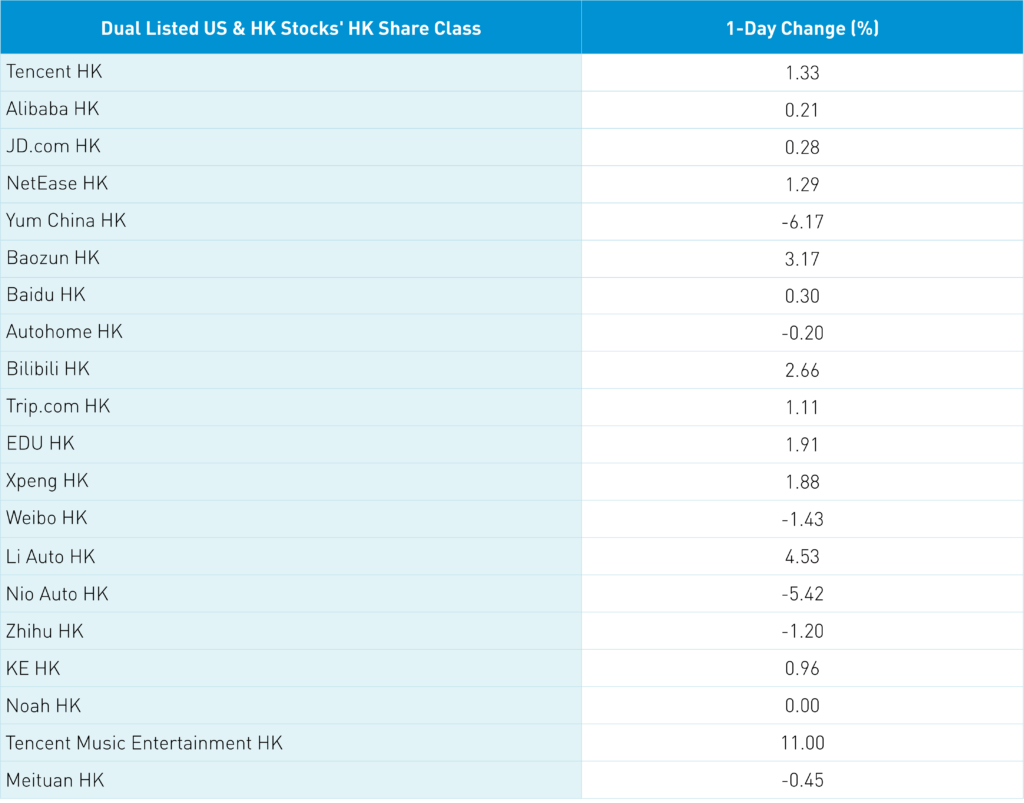

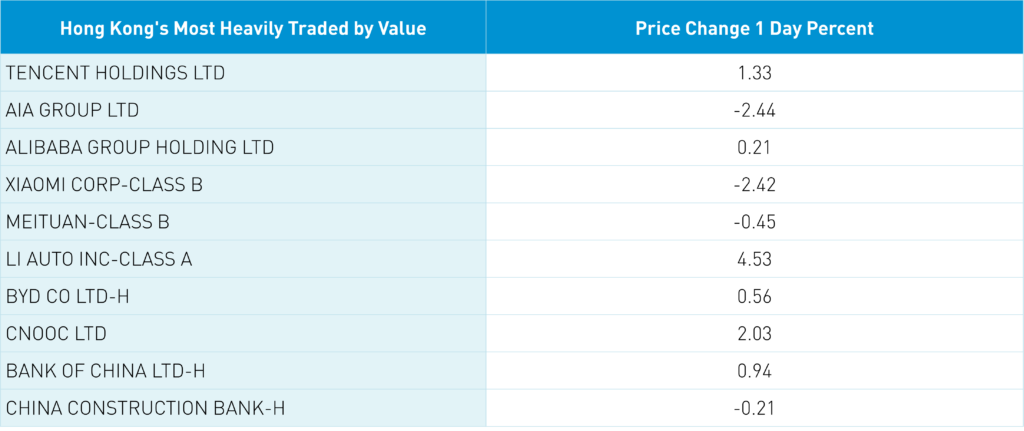

Hong Kong and Mainland China posted small gains with several micro/individual stock moves, while several macro events were non-factors. Hong Kong’s most heavily traded stocks were Tencent, which gained +1.33% in advance of today’s post-close results, AIA, which fell -2.44%, Alibaba, which gained +0.21%, Xiaomi, which fell -2.42%, and Meituan, which fell -0.45% in advance of Friday’s Q4 financial results. Li Auto jumped +4.54% after a recent slide on an analyst downgrade.

Sports apparel maker Li Ning gained +5.67% after its Q4 beat expectations, while founder, Olympic champion, and namesake Li Ning said there are no immediate plans to take the company private.

Yum China fell -6.17% on an analyst downgrade. Prada was down -2.28% after Kering’s Gucci brand revenue warning. China Unicom gained +2.15% after reporting financial results.

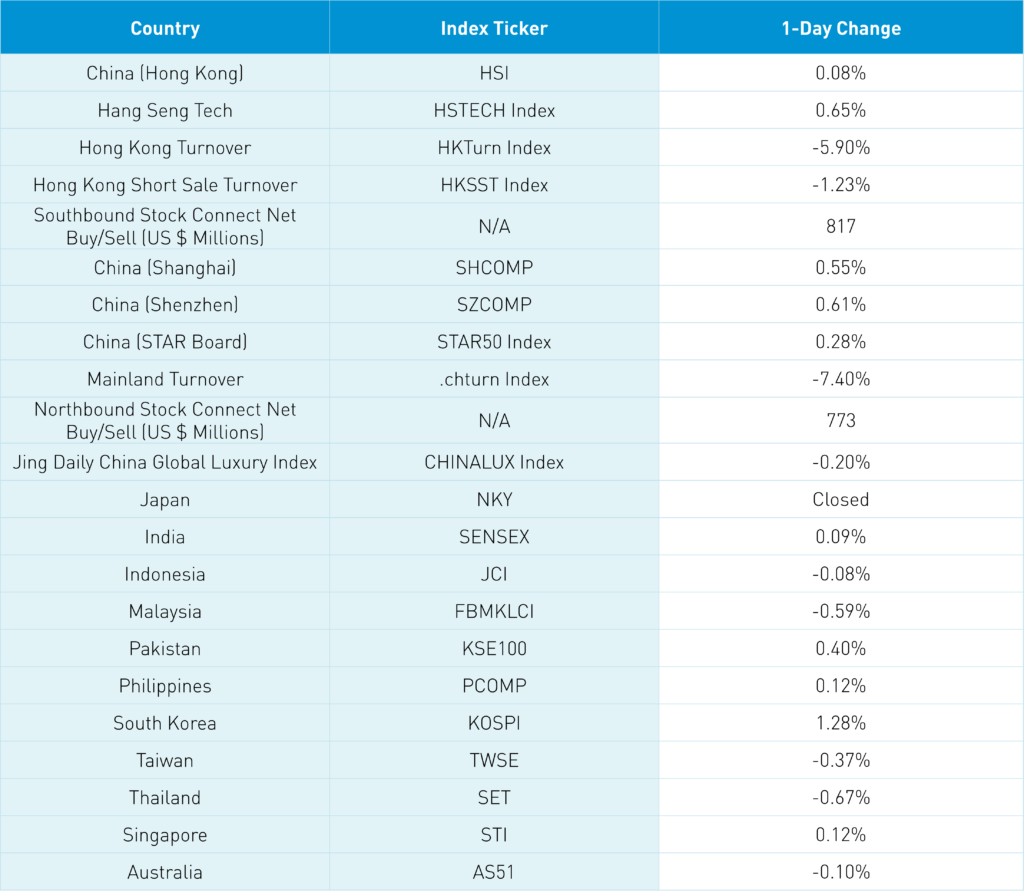

Mainland investors bought a healthy net $817 million worth of Hong Kong-listed stocks and ETFs today via Southbound Stock Connect. Year-to-date, there has been $13.46B of Hong Kong net buying via Southbound Stock Connect, with 25 days of straight net buying. Shanghai and Shenzhen opened lower but grinded higher to close near intra-day highs. The two largest ETFs used by the National Team had light volumes, though the Northbound Stock Connect saw a healthy $773 million worth of net buying. Tim Cook is in Shanghai, where he met BYD’s President Wang Chuanfu. Can you imagine if Apple had partnered with BYD on US-made EVs?

The 5-Year Loan Prime Rate, which mortgage rates are based on, was left unchanged at 3.95%, as expected. Tomorrow there will be a press conference and Q&A with the National Development and Reform Commission (NDRC), the Ministry of Finance, and the PBOC on financial policy. The unemployment rate for those between the ages of 16 and 24 who are not in school was 15.3%.

Chinese Foreign Minister Wang Yi is in Australia where he met with Penny Wong, the first senior Chinese official to visit Australia since 2017. There was also some chatter the Biden Administration might expand bans to Huawei’s semis ecosystem, though it is nothing new.

It was a busy morning so I was up especially early. I was shocked that as Tencent’s results were coming out, financial TV stayed focused on Nvidia’s event. Not surprising, but it is also why I am bullish.

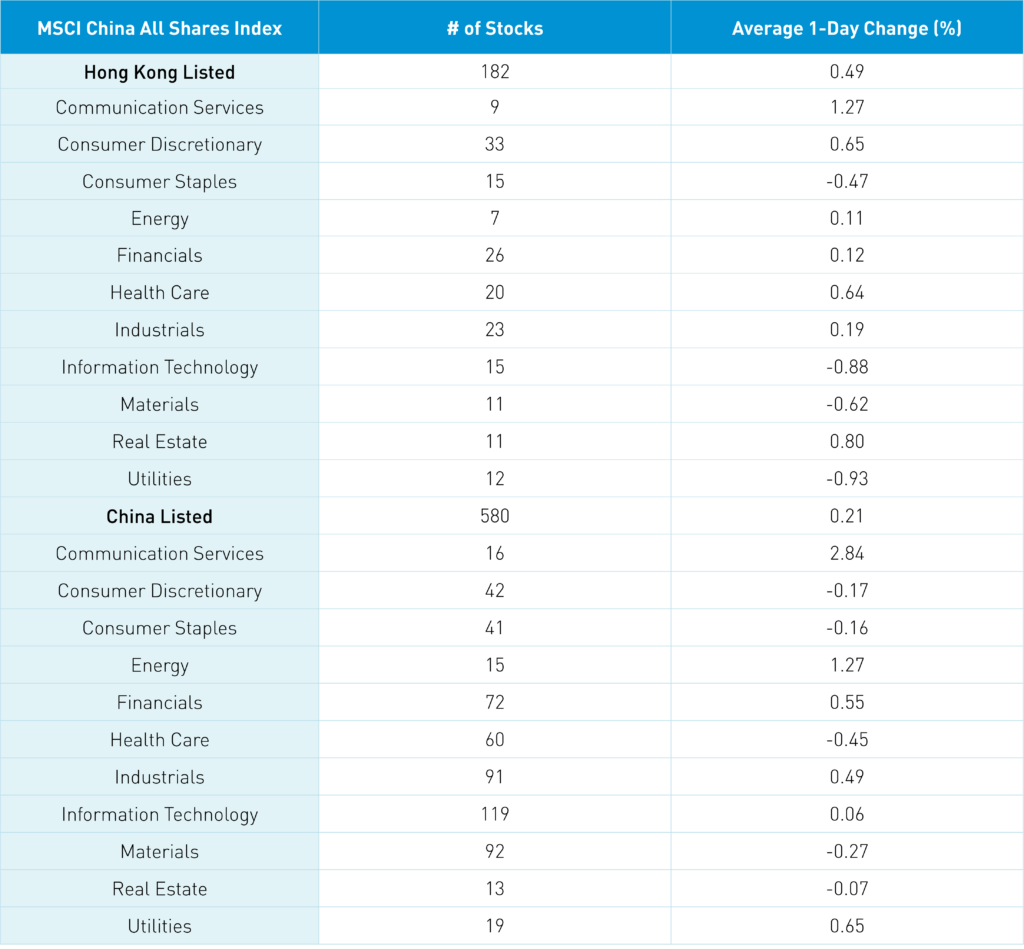

The Hang Seng and Hang Seng Tech indexes gained +0.08% and +0.65%, respectively, on volume that decreased -5.90% from yesterday, which is 87% of the 1-year average. 262 stocks advanced, while 207 declined. Main Board short turnover declined -1.23% from yesterday, which is 104% of the 1-year average, as 21% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and large caps outperformed the value factor and small caps. The top-performing sectors were Communication Services, which gained +1.27%, Real Estate, which gained +0.8%, and Consumer Discretionary, which gained +0.65%. Meanwhile, Utilities fell -0.93%, Technology fell -0.88%, and Materials fell -0.62%. The top-performing subsectors were media, food, and transportation. Meanwhile, consumer services, food and beverages, and insurance were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a healthy net $817 million worth of Hong Kong-listed stocks and ETFs including the Bank of China, China Mobile, and Tencent, which were small net buys. Meanwhile, Meituan, China Shenhua, and China Construction Bank were very small net sells.

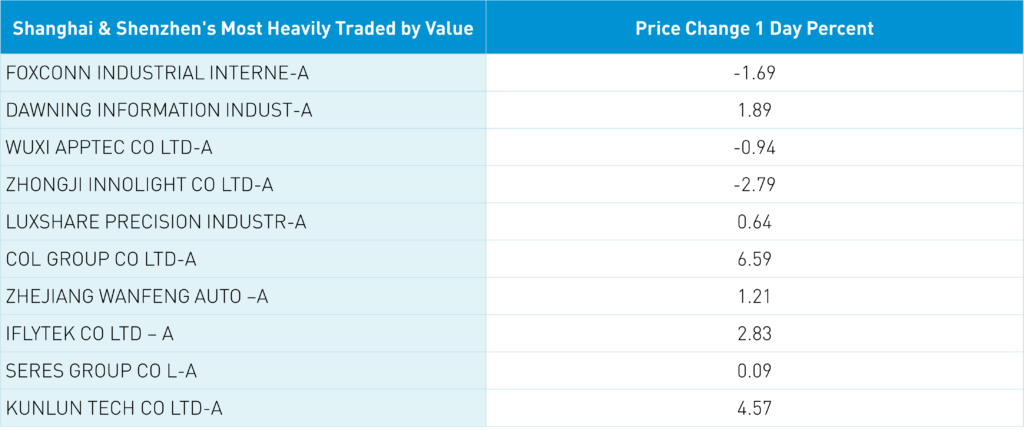

Shanghai, Shenzhen, and the STAR Board gained +0.55%, +0.61%, and +0.28%, respectively, on volume that decreased -7.40% from yesterday, which is 114% of the 1-year average. 3,504 stocks advanced, while 1,316 declined. The value factor and large caps outperformed the growth factor and small caps. The top-performing sectors were Communication Services, which gained +2.86%, Energy, which gained +1.29%, and Utilities, which gained +0.67%. Meanwhile, Health Care fell -0.44%, Materials fell -0.25%, and Consumer Discretionary fell -0.15%. The top-performing subsectors were motorcycles, cultural media, and education. Meanwhile, office supplies, construction, and steel were among the worst-performing. Northbound Stock Connect volumes were high as foreign investors bought a net $773 million worth of Mainland stocks, including Eptolink, which was a small net buy, Midea Group, and Focus Media. Meanwhile, foreign investors were net sellers of Foxconn, moderately, and Sokon and LXJM, which were small net sells. CNY and the Asia Dollar Index were off slightly versus the US dollar while Treasury bonds fell. Copper fell while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.80 versus 7.80 yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.42% versus 2.39% yesterday

- Copper Price -0.89%

- Steel Price +0.96%