Meituan Crushes Analyst Estimates, Alibaba’s Must-Read Regulatory Filing, Week in Review

5 Min. Read Time

Week in Review

- Asian equities were mixed this week as Japan outperformed on the BOJ’s dovish rate hike, and China’s markets corrected somewhat after gains last week.

- It was a busy week for earnings, with better-than-expected Q4 reports from Tencent Music, Tongcheng Elong Travel, and PDD. Meanwhile, Kuaishou, Xpeng, and Tencent reported mixed results.

- January-February industrial production exceeded expectations, according to an official release Monday, while real estate sales and investment came in lighter than expected as demand remains sluggish in the sector.

- Apple CEO Tim Cook was in China this week to open the country’s largest Apple store and discuss AI integrations with Baidu, while the US Department of Justice launched an antitrust lawsuit against the company back at home.

Meituan Q4 Results Overview

Local services and food delivery giant Meituan reported Q4 financial results that beat most estimates on the top and bottom lines. The bottom line, earnings per share (EPS), beat was most notable as many analysts had expected the company's margins to suffer from increased user subsidies to provide an edge in its competition with Douyin (China's TikTok).

% changes are year-over-year (YoY)

- Revenue increased 22.6% to RMB 73.695B from RMB 60.1B versus estimate RMB 72.6B

- Adjusted net income increased 427% to RMB 4.374B from RMB 829mm versus estimate RMB 2.89B

- Adjusted EPS RMB 0.70 from RMB 0.13 versus estimate RMB 0.42

Friday’s Key News

Asian equities were mixed overnight despite the US dollar’s strength as all Asian currencies were down versus the dollar, except for the Yen and the Hong Kong Dollar, which is pegged.

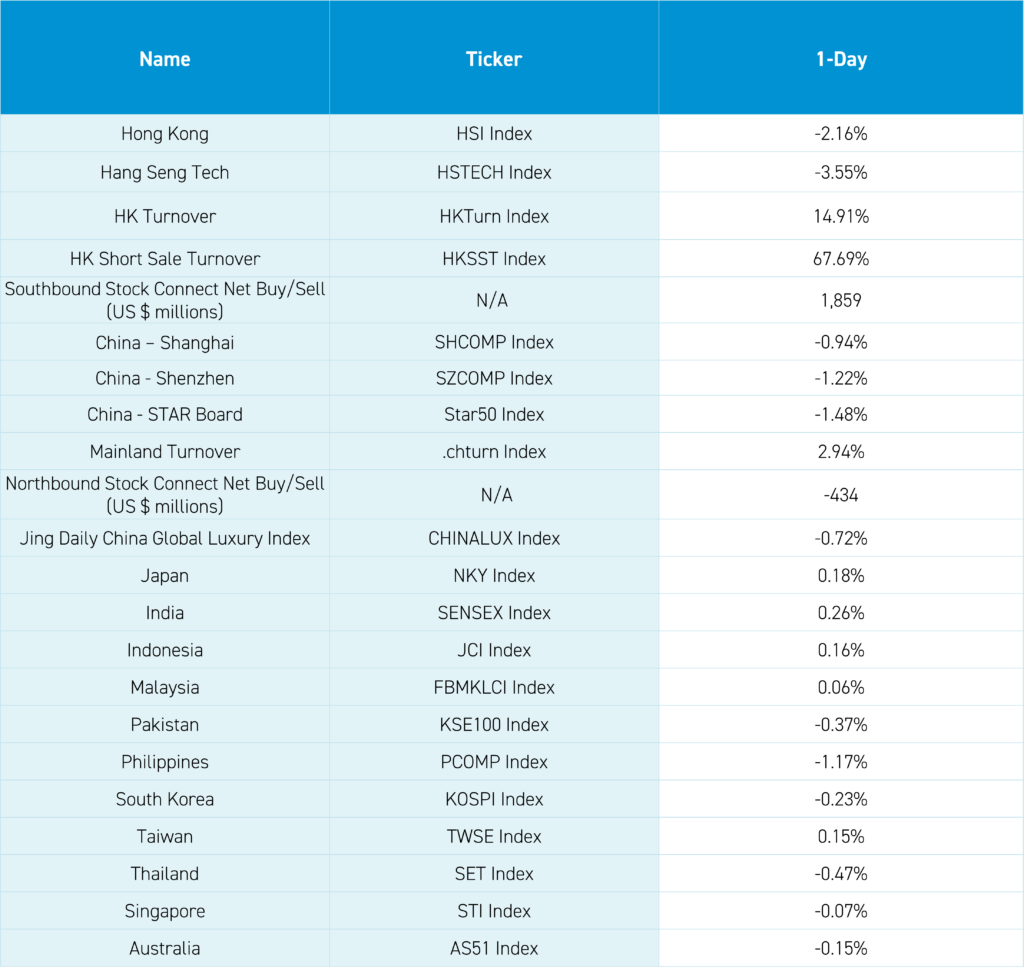

Mainland China and Hong Kong were lower on several macro and micro factors. China’s currency, the Renminbi (CNY), was off -0.42% versus the US dollar, closing at 7.22 CNY per USD as the 7.20 level was breached.

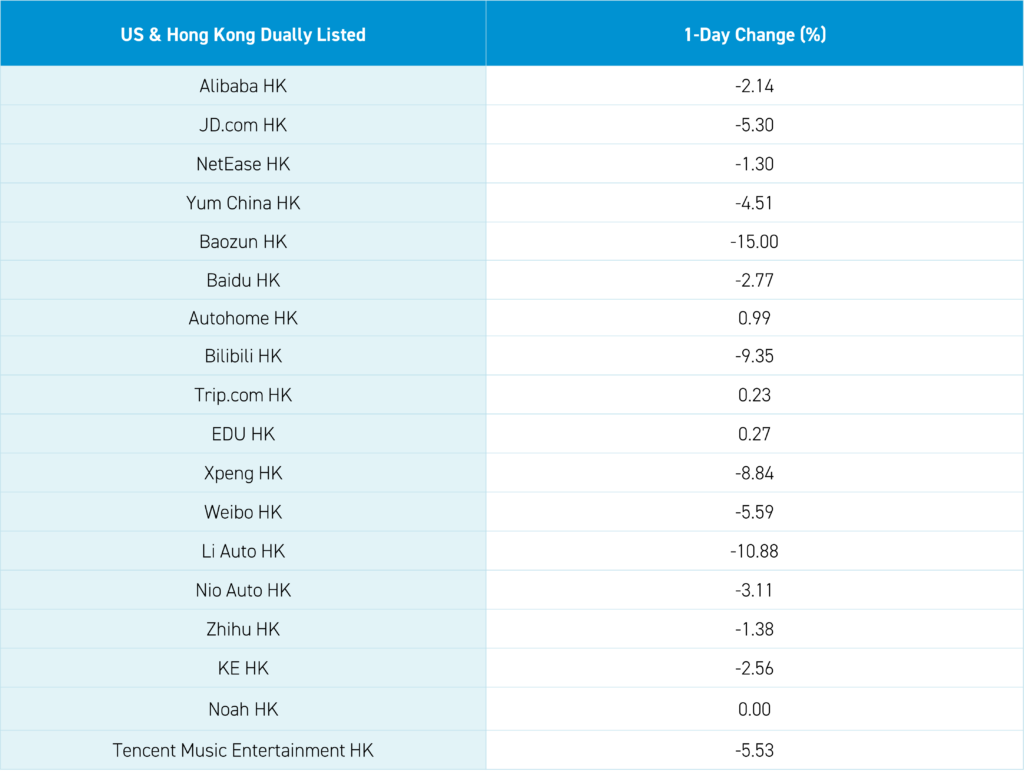

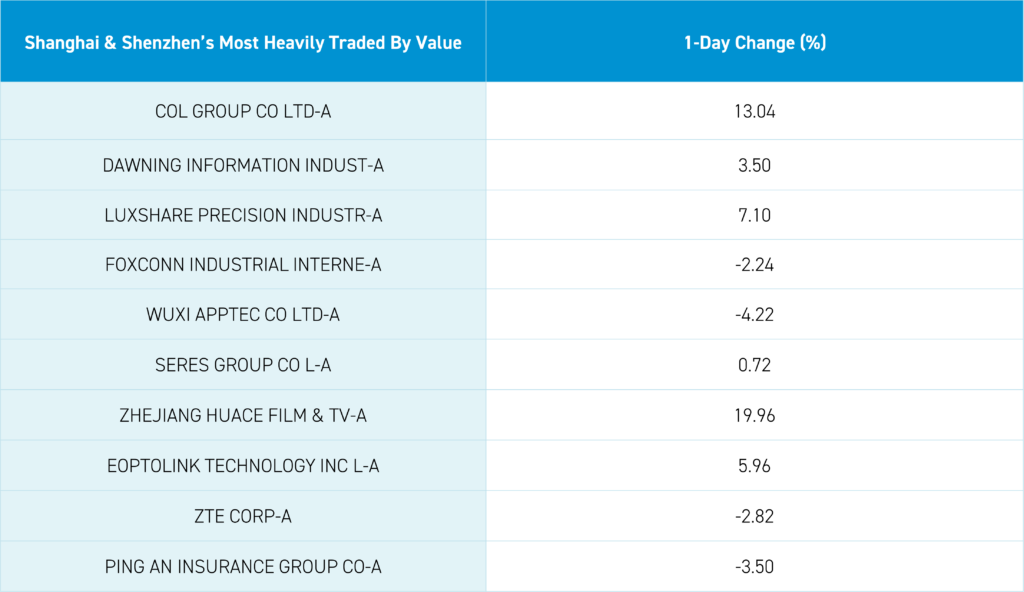

After yesterday’s close, insurance giant Ping An, a significant Hong Kong and Mainland index weight, released disappointing financial results. Its Hong Kong share class fell -5.77% while the Mainland (A share) share class fell -3.50%. The news weighed on the financial sector. Meanwhile, Alibaba’s Bilibili stake sale sparked fears that both Alibaba and Tencent could sell down other minority stakes in various businesses. The bigger question is what Alibaba will do with the proceeds. They could return them to shareholders, which would be a good outcome.

PDD’s amazing financial results led to some profit-taking and maybe some rotation toward other e-commerce stocks.

Li Auto fell -10.88% after its new model’s disappointing results continued to weigh on the electric vehicle (EV) ecosystem.

Technology was off broadly. Some pointed to a Bloomberg News report on Congressional testimony that Semiconductor Manufacturing International (SMIC), which fell -5.5%, broke US law for selling chips to Huawei. Both companies are restricted from US capital markets, so I am not sure if US law applies. The irony is that the US’ new rules are forcing Chinese semiconductor companies to innovate. Recently, a bill was introduced in the House that would ban US mutual funds from investing in Chinese stocks. The probability that the bill will become law is very low, in my opinion, though it sums up the mood in DC. This is all happening in Congress even though US businesses continue to profit in China, as evidenced by Apple CEO Tim Cook’s China visit.

Tim Cook will be joined by dozens of US executives for a meeting with President Xi later this year. Xi’s speech at the Asia Pacific Economic Cooperation (APEC) Summit indicated a significant change in China’s attitude toward foreign investors and corporations.

Mainland investors bought the dip in Hong Kong to the tune of $1.9 billion. Meanwhile, Mainland China was off as foreign investors sold a net -$434 million worth of Mainland stocks. However, the National Team’s favorite ETF, with the ticker 510300 CH, saw a volume increase to 1.45 million shares from yesterday’s 619,000, and their other favorite, which has the ticker 510310 CH, saw a volume increase to 1.7 million from yesterday’s 322,000.

Yesterday, Alibaba released a US regulatory filing that included a very interesting line following their annual report filing with the SEC. I have not seen any comments from a sell-side analyst, trading desk, or news outlet on this. The filing chronicled the company’s inclusion in the Holding Foreign Companies Accountable Act (HFCAA) and the company's addition to the SEC’s list of American Depository Receipts (ADRs) that could be banned because their auditors’ books had not been audited by the Public Company Accounting Oversight Board (PCAOB). In response to the Holding Foreign Companies Accountable Act (HFCAA), Chinese law was changed in August 2022 to allow the companies’ auditors, all subsidiaries of the US “Big Four” accounting firms, to provide access to the PCAOB inspectors. As a result, the PCAOB inspectors have visited China twice for auditor inspections. After the first visit in December of 2022, they announced two auditors they visited passed their review, though there were deficiencies that needed to be fixed. They have already fined two of the auditors for these deficiencies. However, the board has yet to comment on their latest inspections. Yesterday, Alibaba noted that “we do not expect to be identified as a Commission-Identified Issuer following the filing of this annual report.” HFCAA says that a company could be banned if it fails an audit review for three years in a row. Conversely, this is the third year an audit review is feasible, as the PCAOB said the 2021 filings would be counted as passing. Therefore, Alibaba thinks they should be removed from the SEC’s list. Why is this a big deal? For professional investors, holding a stock that could be delisted, even if that risk is small, is very difficult, if not impossible. Obviously, many professional investors can hold Alibaba’s Hong Kong share class, but not every US investor can access overseas stocks. The removal of Alibaba from the list could be a positive catalyst for the stock as the delisting risk has effectively been eliminated. You heard it here first.

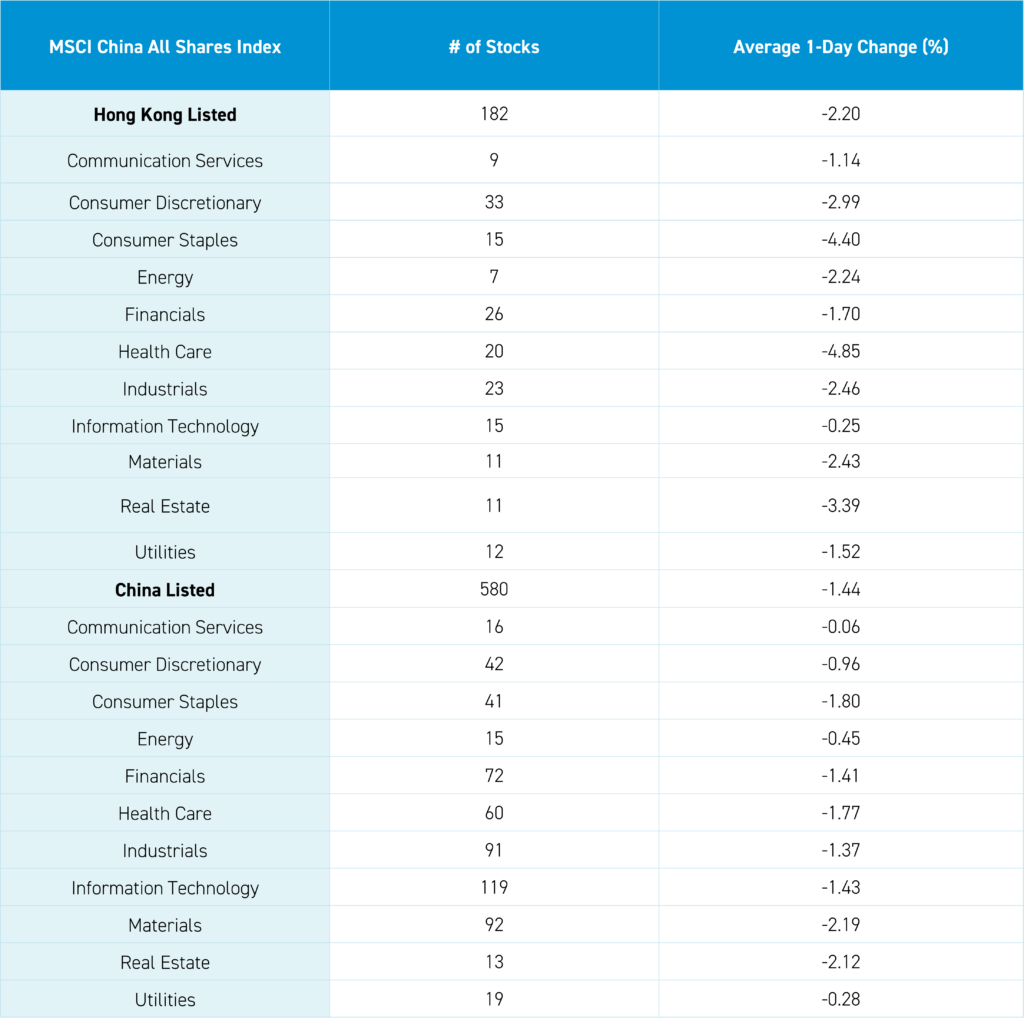

The Hang Seng and Hang Seng Tech indexes fell -2.16% and -3.55%, respectively, on volume that increased +14.91% from yesterday, which is 139% of the 1-year average. 73 stocks advanced while 420 fell. Main Board short turnover increased +67% from yesterday, which is 231% of the 1-year average as 29% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative as the value factor and large caps fell less than the growth factor and small caps. All sectors were negative, as Health Care was the worst-performing sector, down -4.85%, Consumer Staples fell -4.4%, and Real Estate fell -3.4%. Telecommunication Services and technical hardware were the only positive subsectors, while pharmaceuticals, food, and autos were among the worst-performing. Southbound Stock Connect volumes were very high as Mainland investors bought a net $1.9 billion worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which was a very large net buy, the Hang Seng China Enterprise ETF, and Tencent, which was a moderate net buy.

Shanghai, Shenzhen, and the STAR Board fell -0.94%, -1.22%, and -1.48%, respectively, on volume that increased +2.94% from yesterday, which is 125% of the 1-year average. 902 stocks advanced, while 4,098 declined. All factors were negative, as the value factor and large caps fell less than the growth factor and small caps. All sectors were negative, as Materials fell -2.19%, Real Estate fell -2.13%, and Consumer Staples, which fell -1.81%. The top-performing subsectors were cultural media, household appliances, and telecommunication. Meanwhile, insurance, base metals, and fine chemicals were among the worst. Northbound Stock Connect volumes were very high as foreign investors sold a net -$434 million worth of Mainland stocks, including Wuliangye, CATL, and Zijin Mining, which were all moderate net buys. Meanwhile, Kweichow Moutai, Changan Auto, and Ping An Insurance were moderate net sales. CNY and the Asia Dollar Index were off versus the US dollar. Treasury bonds were sold. Copper was off while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.20 yesterday

- CNY per EUR 7.82 versus 7.82 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.40% yesterday

- Yield on 10-Year Government Bond 2.31% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.43% versus 2.40% yesterday

- Copper Price -0.48%

- Steel Price 0.70%