President Xi Meets with US CEOs

3 Min. Read Time

Key News

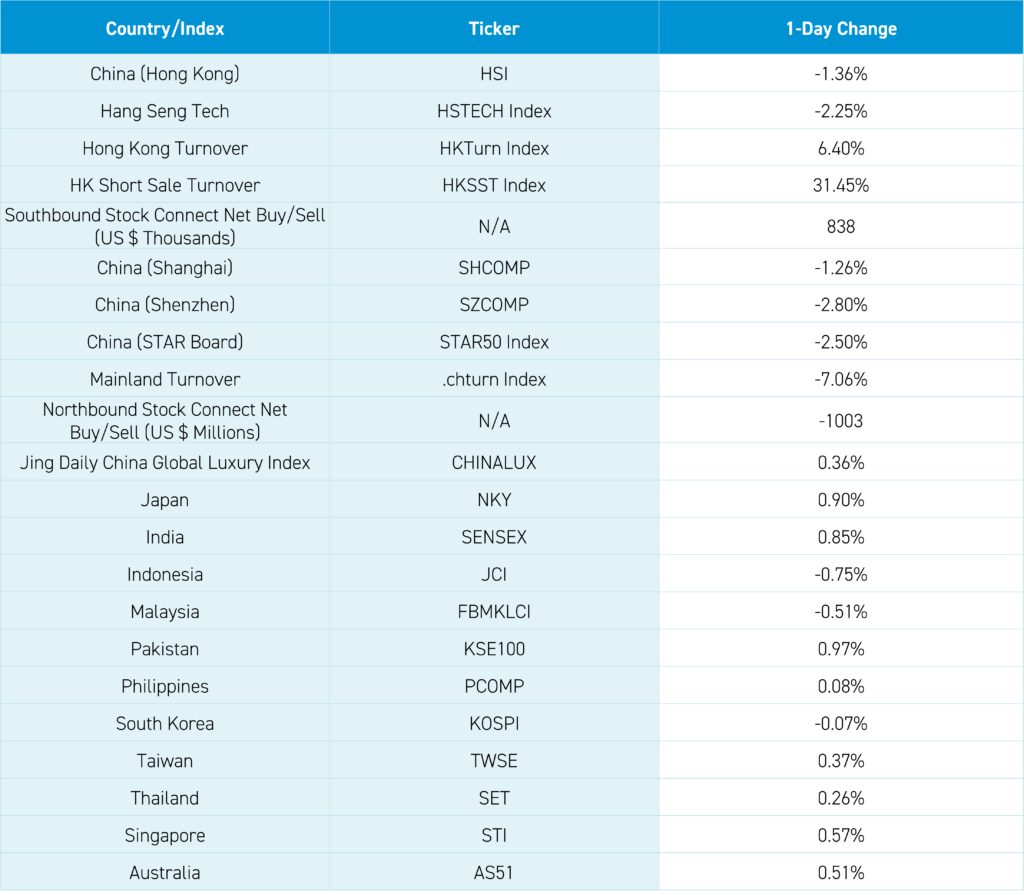

Asian equities were mixed overnight, as Japan, Taiwan, and India posted small gains while Hong Kong, Mainland China, and South Korea were off. There were several positives from a big-picture perspective, while single stock developments disappointed.

President Xi had a busy day meeting Dutch Prime Minister Mark Rutte, with, I assume, semiconductor chips as topic #1. The Netherlands has restricted exports of ASML chip-making equipment to China-based customers. President Xi also met with US CEOs, including Blackstone’s Stephen Schwarzman, Qualcomm’s Cristiano Amon, FedEx’s Raj Subramaniam, and Chubb’s Evan Greenberg. I’ll link to the official readout on Twitter (@ahern_brendan). President Xi stated, “Sino-US relations are one of the most important bilateral relations in the world.” During the hour-and-a-half meeting, President Xi acknowledged “issues with the domestic economy” while restating the opportunity in China and included a Q&A with the executives. Hopefully, more details will be revealed! It feels like the event was put together on short notice, which may explain why more executives weren’t there, having planned to leave China on Tuesday.

January/February Industrial Profits increased to 10.3% year-over-year (YoY) compared to January’s -2.3% YoY (due to the Chinese New Year holiday, January & February were combined). Within the industrial profits measure, manufacturing increased +17.4% YoY.

The US dollar appreciated overnight, weighing on Asian currencies less Japan Yen and the Philippine Peso. The Bank of Japan’s afternoon press conference led to a sudden Yen strengthening versus Asian currencies, which was blamed for the late afternoon plunge in Mainland Chinese equities. Also blamed for the Mainland’s late afternoon fall, which made an off day much worse, was the expiration of Mainland ETFs’ options, though I’ve never heard of ETF options roll causing an issue.

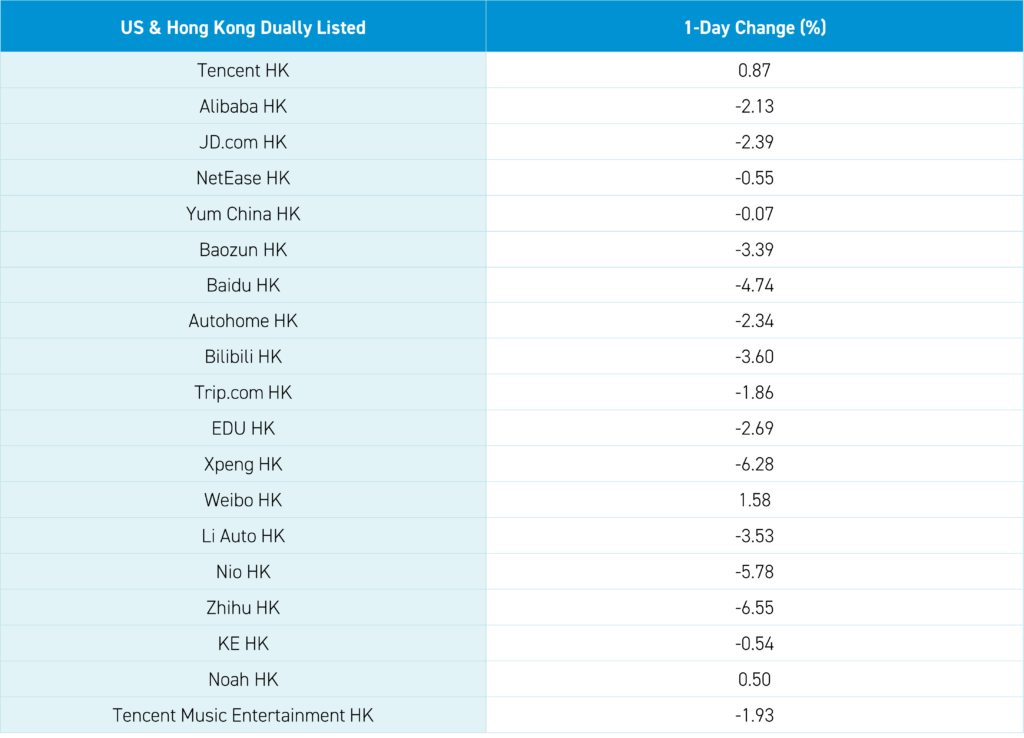

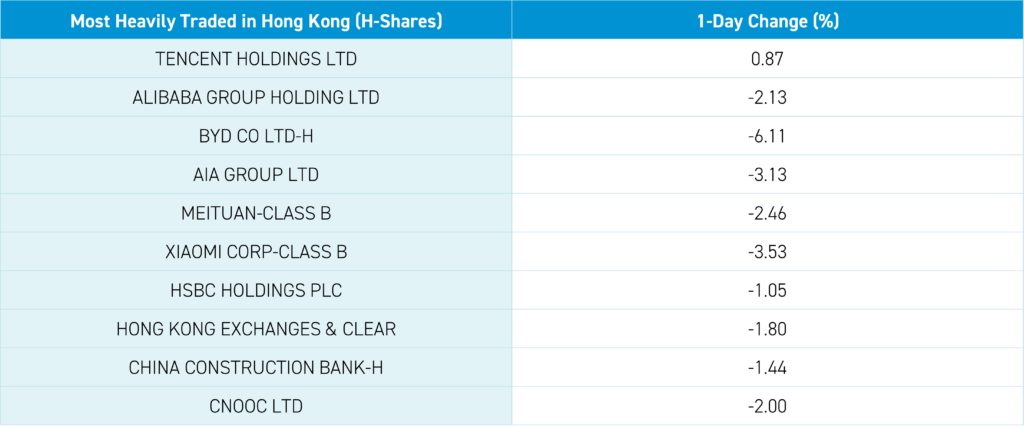

Northbound Stock Connect was a large net sell off -$1 billion, though that trading was a morning phenomenon. Stock-specific issues weighed on Hong Kong. Alibaba fell -2.13% after pulling the IPO of their logistics arm Cainiao and buying out minority shareholders. IPOs are best done at market highs versus market lows, which is a simple explanation. The news also weighed on Hong Kong Exchanges, which fell -1.8% despite a pickup in Hong Kong IPOs this week. Meanwhile, BYD fell -6.11% after posting strong results that missed analyst expectations, though investors' concerns about a price war are a factor. BYD's 2023 revenue increased +42% YoY, its EPS increased +81%, and its net income increased +81%, which looks pretty good to me.

Baidu fell -4.74% after local media reported that the company’s agreement to use its AI chat bot "Ernie Bot" by Apple iPhones in China had not been finalized. Using Baidu AI in China and Google AI in the US makes sense to me, as opposed to plowing huge sums of cash into AI and large language models like ChatGPT, which might be commoditized over time. Reports of weak Apple February iPhone weighed on the Apple ecosystem, especially tech and semis. Mainland investors bought the dip in Hong Kong with a healthy $848 million worth of net buying. Tencent gained +0.87%, as Hong Kong’s most heavily traded stock by value.

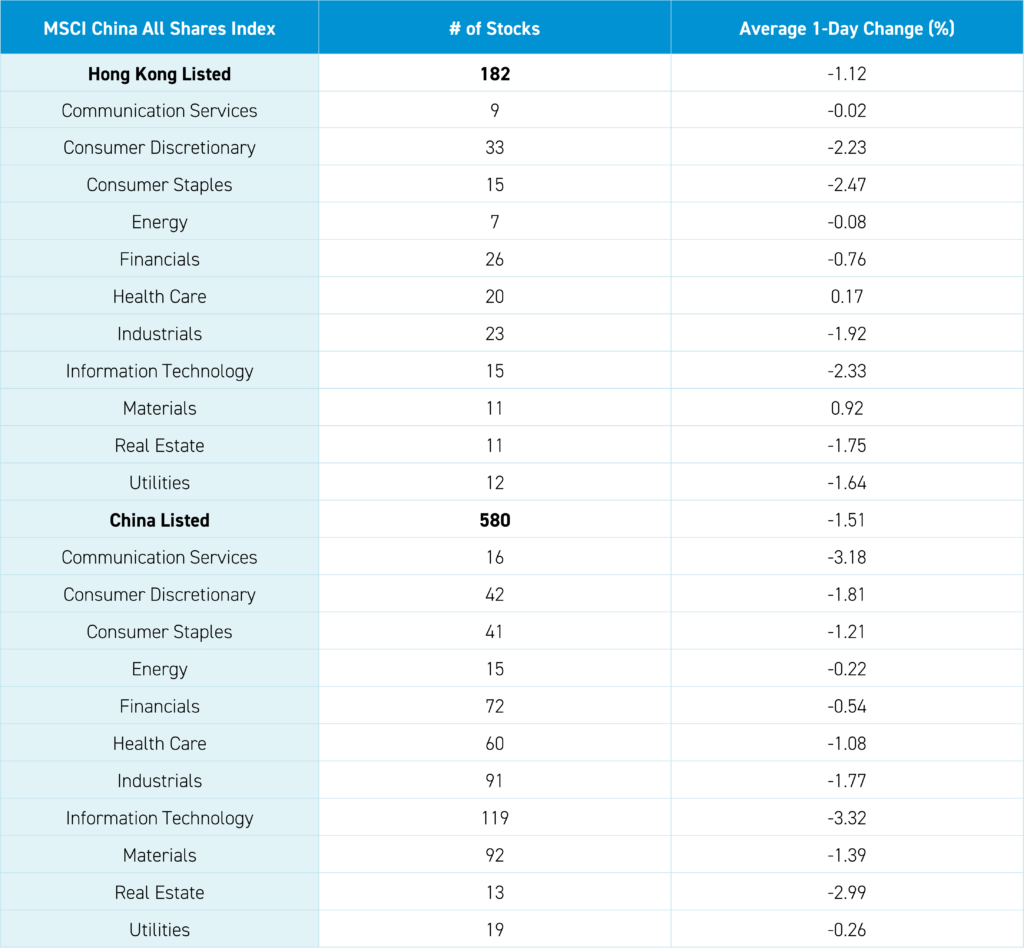

The Hang Seng and Hang Seng Tech indexes fell -1.36% and -2.25%, respectively, on volume that increased +6.4% from yesterday, which is 118% of the 1-year average. 148 stocks advanced, while 333 declined. Main Board short turnover increased +31.45% from yesterday, which is 133% of the 1-year average, as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, with the growth factor and small caps falling less than the value factor and large caps. Materials and healthcare were the only positive sectors, gaining +0.92% and +0.17%, respectively. Meanwhile, Consumer Staples fell -2.47%, Technology fell -2.33%, and Consumer Discretionary fell -2.23%. The top-performing subsectors were food, healthcare equipment, and consumer durables. Meanwhile, autos, technical hardware, and capital goods were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $838 million worth of Hong Kong-listed stocks and ETFs, including Tencent, the Hong Kong Tracker ETF, and the Bank of China were moderate net buys. Meanwhile, Yanzhou Coal, SMIC, and Meituan were very small net sells.

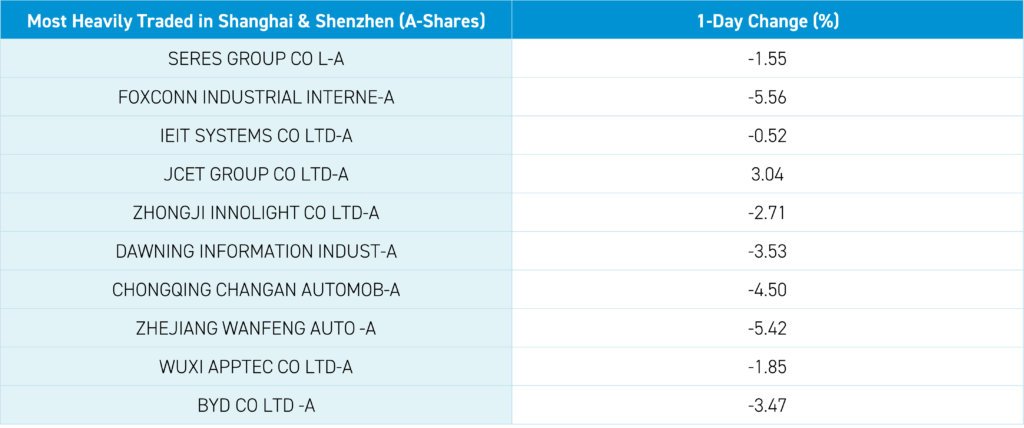

Shanghai, Shenzhen, and the STAR Board fell -1.26%, 2.80%, and -2.50%, respectively, on volume that declined -7.06% from yesterday, which is 102% of the 1-year average. 694 stocks advanced, while 4,300 declined. All factors were negative. The value factor and large caps falling less than the growth factor and small caps. All sectors were negative, as Technology fell -3.29%, Communication Services fell -3.16%, and Real Estate fell -2.96%. The top-performing subsectors were precious metals, banking, and household appliances. Meanwhile, internet, software, and business services were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$1 billion worth of Mainland-listed stocks, including China Merchants Bank, Sevenstar, and Ping An Insurance, which were small net buys. Meanwhile, CATL, JCET, and Accelink were small net sells. CNY and the Asia Dollar Index were off versus the US dollar. Treasury bonds rallied while copper and steel were off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.22 versus 7.21 yesterday

- CNY per EUR 7.82 versus 7.83 yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.31% yesterday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.45% yesterday

- Copper Price -0.10%

- Steel Price -1.32%