Xiaomi Roars Quietly Into EVs, China Corporates & Regulators Visit NYC, Week in Review

4 Min. Read Time

Week in Review

- Asian equities were mixed for the week as Japan and China markets underperformed and India outperformed.

- Global CEOs including AMD’s Lisa Su, Apple’s Tim Cook, AstraZeneca’s Pascal Soriot, and Blackstone's Stephen Schwarzman convened for the 2024 China Development Forum in Beijing and some went on to meet personally with President Xi along with Dutch Prime Minister Mark Rutte.

- For the internet sector, food delivery and local services giant Meituan gained on better-than-expected earnings while Alibaba shares fell on the retraction of logistics arm Cainiao’s IPO application while the company repurchases shares from existing holders and awaits an improvement in market conditions to proceed with the listing.

- China’s industrial profits increased +10% year-over-year (YoY) for the January-February period after a YoY decrease of -2% in January.

Friday’s Key News

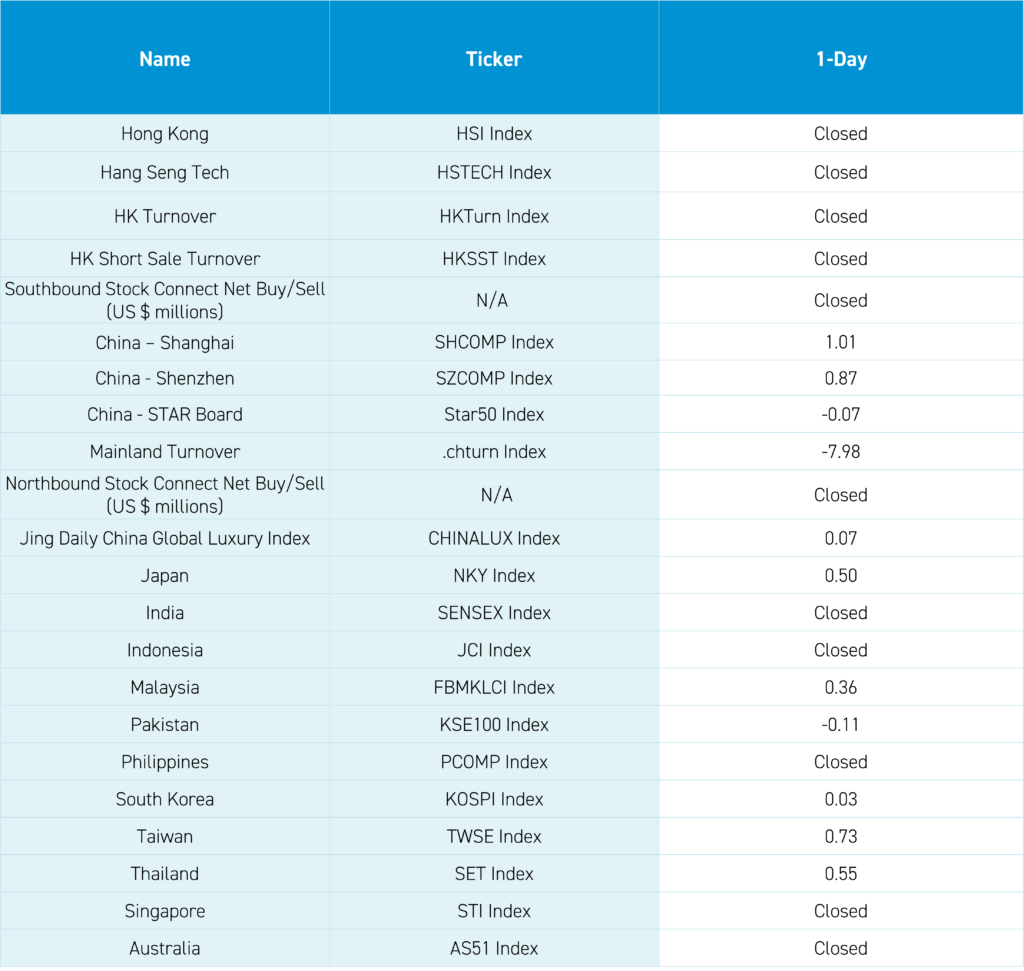

The Asian markets that were not closed for Good Friday ended the month and quarter higher on understandably light volume.

The Shanghai Composite ended the quarter (year-to-date) positive, gaining +0.53% in US dollar terms and +2.23% in Renminbi terms, rallying from its February 5th low following the Mainland’s snowball (derivative contract) meltdown. Shenzhen, the Hang Seng, and the Hang Seng Tech indexes are still negative year-to-date, having not quite reached positive territory, though hopefully the upward trend continues.

It was a light news day, though the National People’s Congress Standing Committee Chairman Zhao Leji did give the keynote address at the Boao Forum. In his remarks, he reiterated the government’s commitment to opening and providing access to China’s economy and capital markets to foreign companies and investors.

Hong Kong-listed Xiaomi dove into the electric vehicle (EV) industry with the launch of the SU7 sedan for $29,900 with 50,000 orders received in the first ½ hour and 88,898 in the first 24 hours.

The non-listed Huawei reported that its 2023 net profit increased +65% year-over-year (YoY) to $1.9 billion, according to Bloomberg. The Wall Street Journal stated that the company's consumer business group, which includes smartphones, increased +17% YoY. Five years of US technology sanctions have forced the company to innovate, creating a formable Apple competitor.

Agriculture giant Syngenta pulled its Shanghai IPO application, though I wonder whether the decision is related to regulators wanting to limit IPOs (i.e. supply) to support the Mainland market.

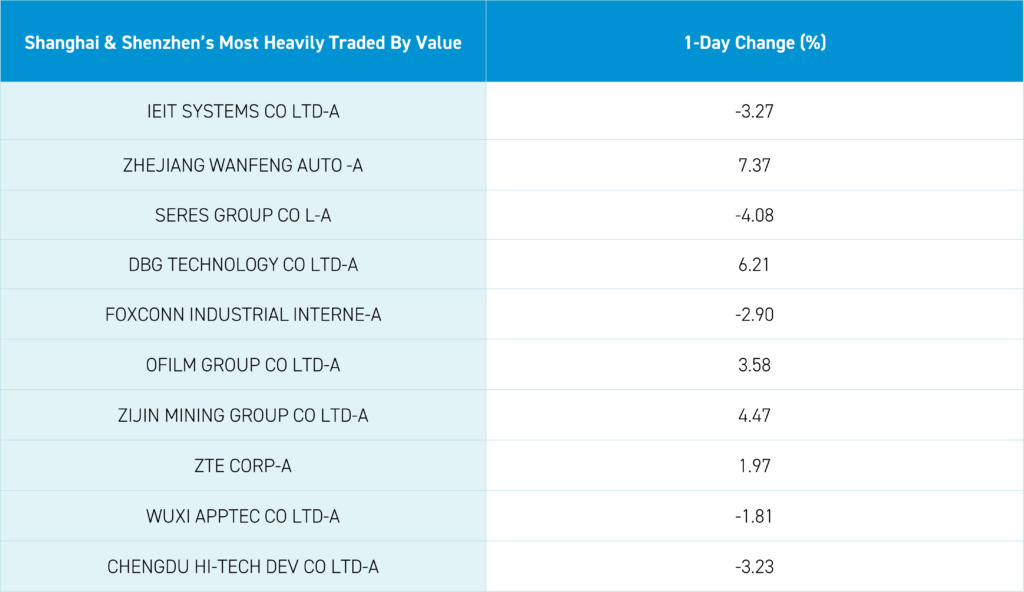

Although Shanghai and Shenzhen posted small gains today, Real Estate vastly underperformed on SOE developer Vanke’s -46% net income decline YoY, which sent shares lower by -2.6% and the company’s bond, which came due in 2027, fell by RMB -0.95 to 79.74.

The National Team’s favorite ETFs had light volumes. Northbound Stock Connect was closed.

China removed tariffs on Australian wine yesterday as the two countries’ diplomatic relations have slowly mended. Perhaps just in time for a good Aussie red with Easter ham? Have a great holiday weekend!

Yesterday, I attended a roadshow in NYC with Shanghai and Shenzhen listed companies. Officials from both exchanges and the Vice Chairman from China’s security regulator the China Securities Regulatory Commission (CSRC). This was some impressive coordination! The Vice Chair of the CSRC stated that the country’s commitment to foreign investors and companies remains strong. He pointed out that Chinese culture prefers “subtle signals” rather than just coming out saying it, as he referenced President Xi’s visit to German conglomerate BASF’s factory in China and his Wednesday meeting with US CEOs. We have pointed out in the past that President Xi’s visit to San Francisco to meet with President Biden was a very significant event indicating a change in tone toward the West. The time is ripe for US-China economic deals, though US domestic policies and the election are front and center. It was great to hear from several companies in which we are invested: Mindray Bio-Medical, Inovance Technology, Yunnan Energy New Material, Tianqi Lithium, Roborock Technology, Ping An Group, Haier Smart Home, Sany Heavy Industry, and Hengrui Pharmaceuticals. There will be more to come on this.

The US equity market resilience despite higher US interest rates has been great though a bit puzzling to me. Yes, the US economy is doing well, which should help US stocks and earnings. I read a lot of good research, but Société Générale’s Albert Edwards wrote a great piece titled “Have you heard the joke about the Fed’s “Restrictive monetary policy”? Without giving away his research for free, I will simply state that he points out that the US money base is growing despite talk of quantitative tightening due to the Fed’s money market operations, which are pumping liquidity into the system. I would think this explains bitcoin and US tech stocks rising. I would suspect that high US interest rates have kept the dollar strong, which also helps US stocks as foreign investors continue to pile in. Jared Dillian, Lehman’s ex head ETF trader and a great macroeconomic thinker and writer, recently wrote about the effect of the US government’s spending on propping up the US GDP and inflating employment numbers, as the US’ state and local governments are hiring though growing US government debt. It makes you wonder what a US GDP and US employment ex US government spending numbers would be? I’ve been shocked the US media does not talk about US government spending contribution to US inflation due to the crowding out effect. My take is that high interest rates have kept the dollar strong, while liquidity has kept US markets higher. I am happy to solicit any feedback or thoughts. If you hit reply to this email, I will respond!

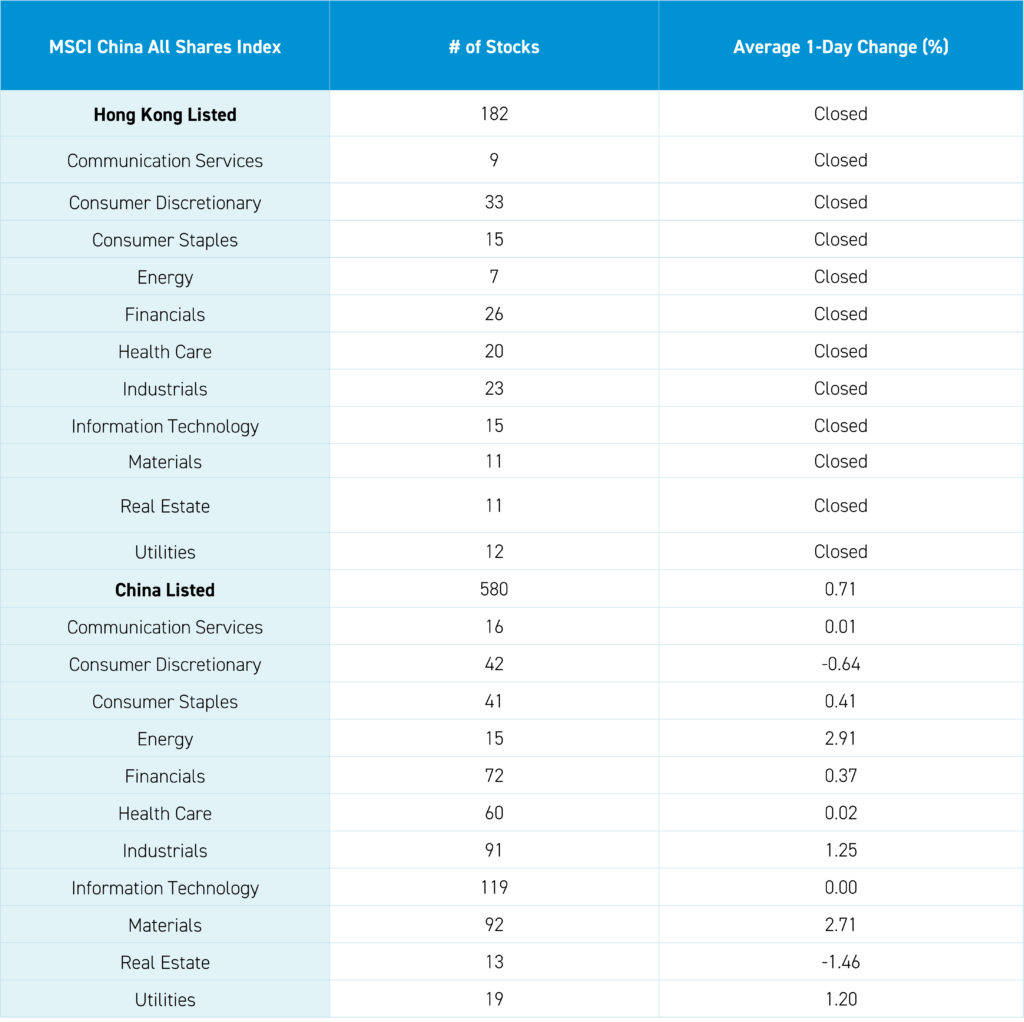

Shanghai, Shenzhen, and the STAR Board diverged to close +1.01%, +0.87%, and -0.87%, respectively, on volume that decreased -7.98% from yesterday, which is 98% of the 1-year average. 3,431 stocks advanced while 1,476 declined. The value factor and large caps outperformed the growth factor and small caps. The top-performing sectors were Energy, which gained +2.91%, Materials, which gained +2.72%, and Industrials, which gained +1.25%. Meanwhile, Real Estate fell -1.45%, Consumer Discretionary fell -0.64%, and Technology was flat. Top-performing subsectors were precious metals, energy equipment, and oil & gas. Meanwhile, autos, real estate services, and internet services were among the worst-performing. Northbound Stock Connect was closed. CNY appreciated versus the US dollar. Treasury bonds rallied. Copper gained while steel was off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.22 versus 7.23 yesterday

- CNY per EUR 7.80 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.51% yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.30% yesterday

- Yield on 10-Year China Development Bank Bond 2.45% versus 2.43% yesterday

- Copper Price +0.21%

- Steel Price -0.72%