Alibaba Joins Tencent’s Buyback Bonanza

3 Min. Read Time

Key News

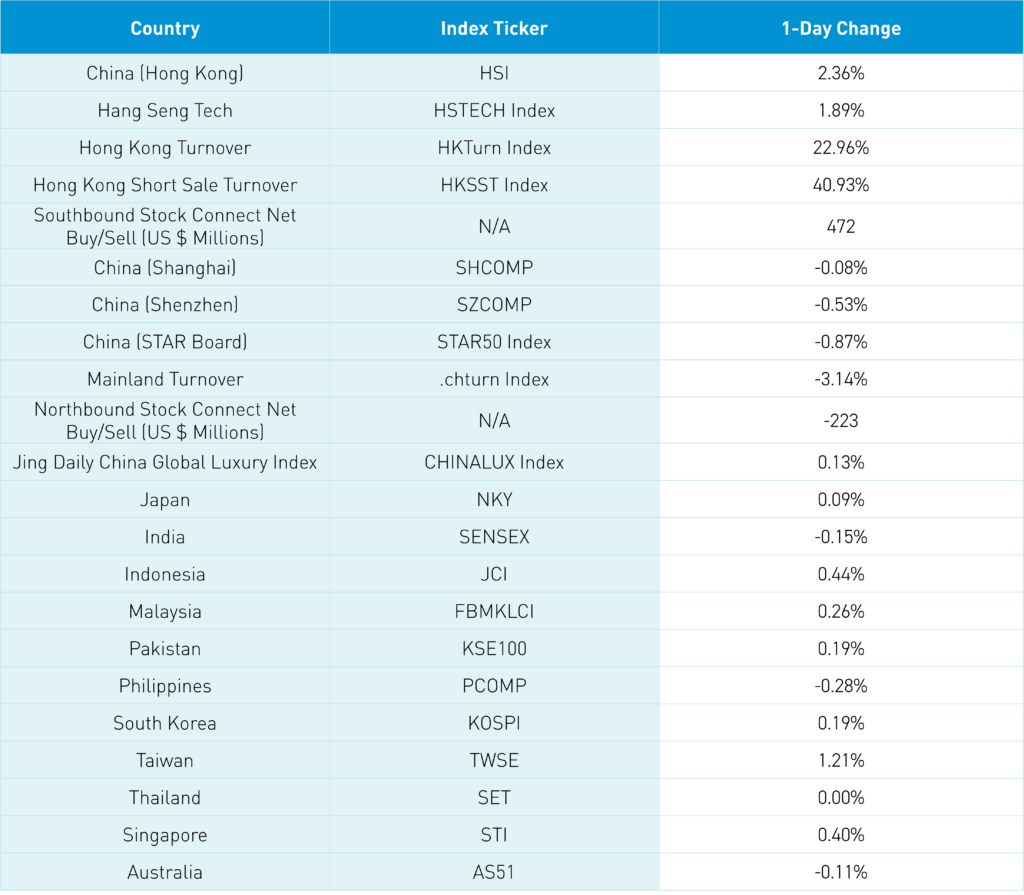

Asian equities were mixed as Hong Kong and Taiwan outperformed.

Hong Kong investors were in a good mood following the four-day weekend as the market played catch up following the Mainland’s positive move and better-than-expected PMIs.

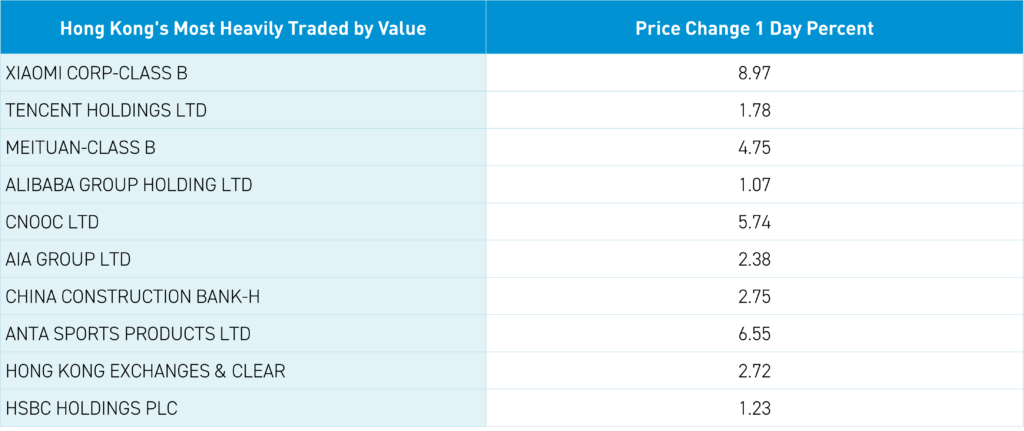

Xiaomi gained +8.97% after its successful foray into electric vehicles (EVs). Its competitors in the space were mixed overnight. Li Auto was up +1.98% and XPeng fell -5.61%. It is remarkable to think how the mobile phone and electronics company pivoted to EVs while Apple drained billions in their effort. It is too bad they didn’t partner!

Brilliance China Auto gained +25.93% on strong financial results and an unexpectedly large dividend payout that forced shorts to cover. We continue to advocate for Hong Kong-listed companies to pay dividends in order to hurt short sellers and raise the cost of shorting. NetEase fell -6.88% after two new games missed expectations while the company reminded investors that minors will have limits on playing time during the upcoming holiday.

Mainland investors bought a net $472 million worth of Hong Kong-listed stocks and ETFs via Southbound Stock Connect. Following Xiaomi's strong day, Hong Kong’s most heavily traded stocks by value were Tencent, which gained +1.78% as the company bought back another 3.23 million shares, Meituan, which gained +4.75%, Alibaba, which gained +1.07%, and CNOOC, which gained +5.74%.

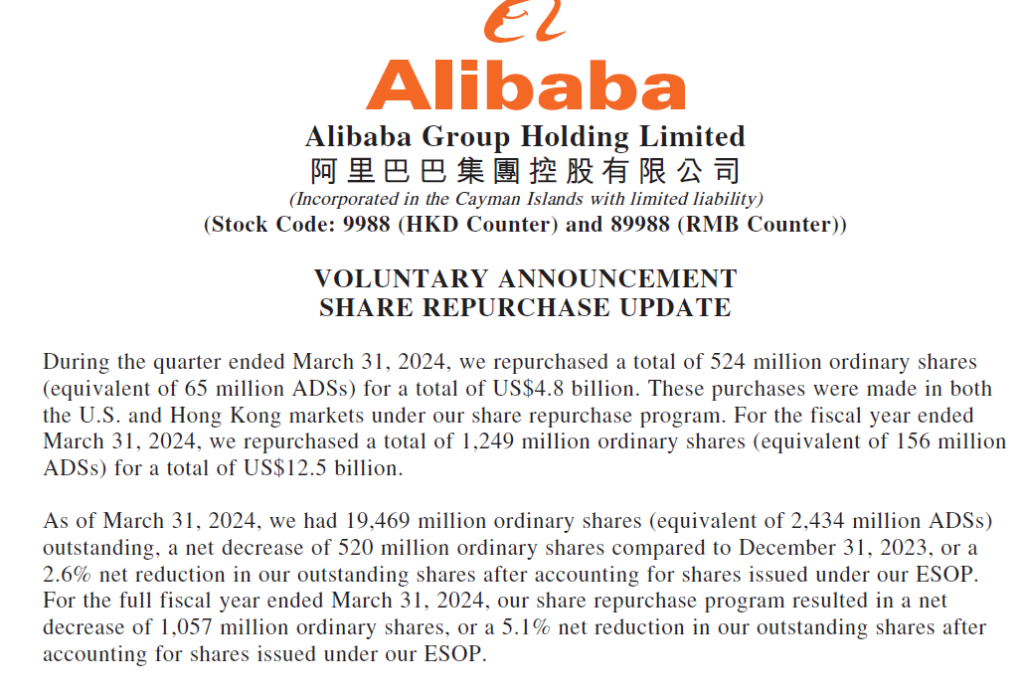

After the Hong Kong close and before the US open, Alibaba filed with the Hong Kong Stock Exchange that, during Q1 2024, the company spent $4.8 billion buying back 65 million ADRs, representing 2.6% of shares outstanding! From Q1 2023 to Q1 2024 the company has bought 1.057 billion shares (5.1% of shares outstanding). Impressive!

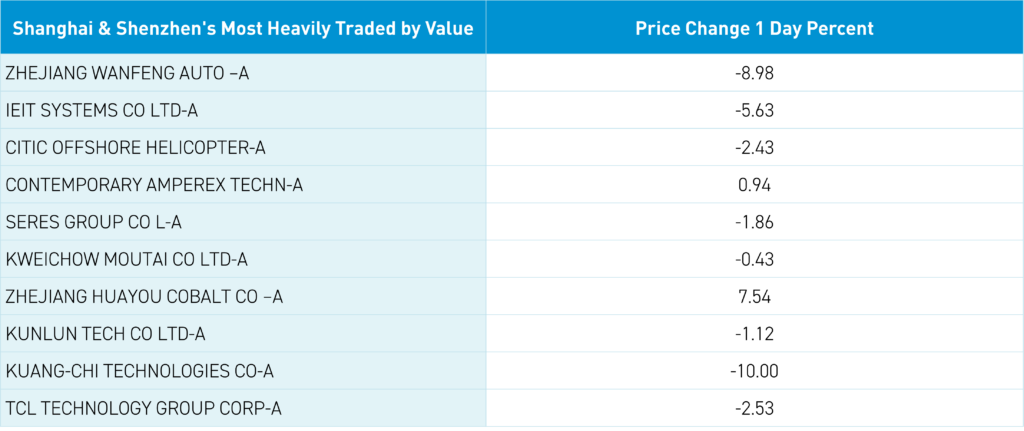

Mainland China bounced around the room, as foreign selling weighed on morning trading as the market slipped and closed in negative territory. Defensive/value plays outpaced growth stocks as Middle East tensions lifted energy stocks. Meanwhile, lithium plays lifted materials and benefited from March EV sales. Mainland-listed real estate development was the worst-performing subsector, led lower by Vanke, which fell -5.35% on an analyst downgrade and a public spat with a local partner. However, redeeming a bond early is a good sign.

The National Development and Reform Commission (NDRC) held a meeting with several companies, including JD Group, Midea, Haier, and Gree, on “large-scale equipment updates and consumer goods replacement.” I was surprised their stocks did not see a more significant reaction.

CNY and the Asia Dollar Index were weaker versus the US dollar. Hog prices increased +2% month over month in March, which should lead to a CPI increase.

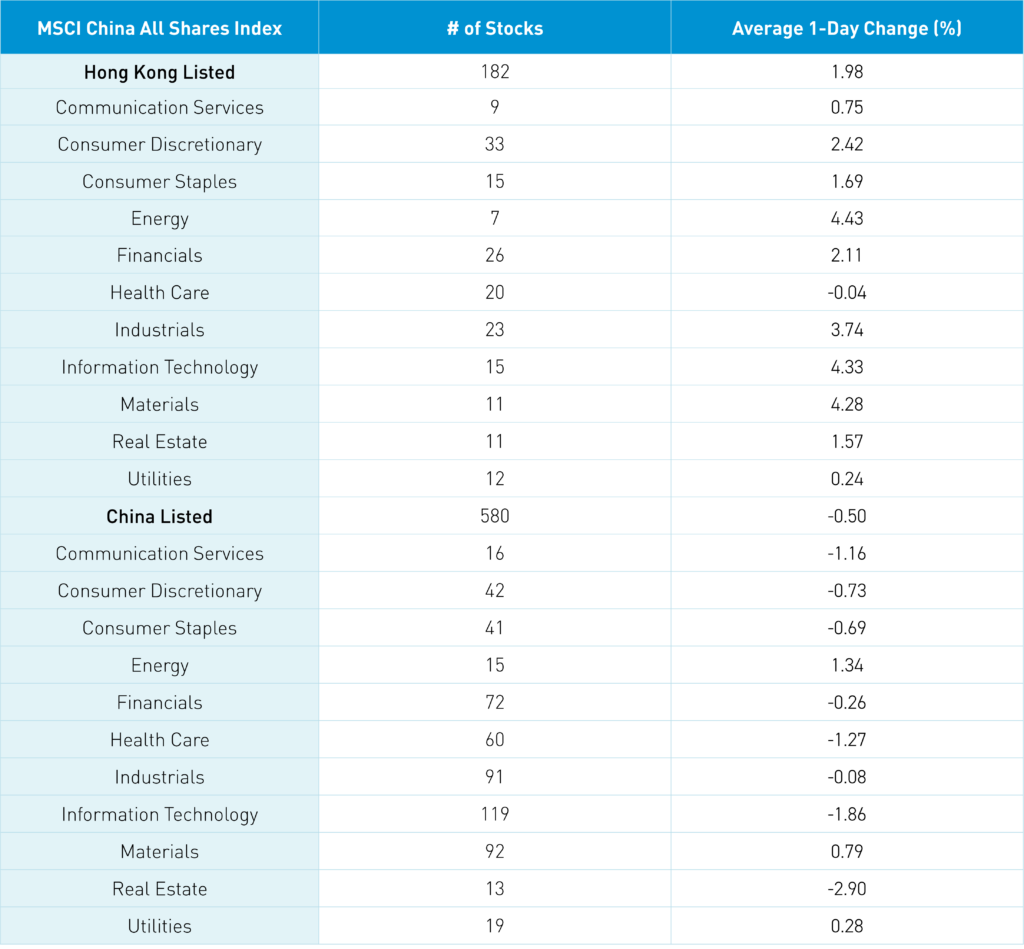

The Hang Seng and Hang Seng Tech indexes gained +2.36% and +1.89%, respectively, on volume that increased +22.96% from last Thursday, which is 148% of the 1-year average. 329 stocks advanced, while 158 declined. Main Board short turnover increased by +40.93% from last Thursday, which is 159% of the 1-year average, as 19% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps outperformed the growth factor and small caps. Meanwhile, the top-performing sectors were Energy and Technology, which both gained +4.33%, along with Materials, which gained +4.28%. Meanwhile, Health Care was off -0.04%. The top-performing subsectors were energy, technical hardware, and materials. Meanwhile, food and healthcare equipment were among the worst-performing subsectors. Southbound Stock Connect volumes were very high as Mainland investors bought a net $472 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which was a moderate net buy, and CNOOC and Li Auto, which were small net buys. Meanwhile, Xiaomi was a large net sell and Sciclone Pharma and Xpeng small net sells.

Shanghai, Shenzhen, and the STAR Board fell -0.08%, -0.53%, and -0.87%, respectively, on volume that decreased -3.14% from yesterday, which is 111% of the 1-year average. 2,231 stocks advanced, while 2,663 fell. The value factor and large caps fell less than the growth factor and small caps. The top-performing sectors were Energy, which gained +1.34%, Materials, which gained +0.79%, and Utilities, which gained +0.28%. Meanwhile, Real Estate fell -2.9%, Technology fell -1.86%, and Health Care, which fell -1.27%. The top-performing subsectors were shipping, fine chemicals, and oil & gas. Meanwhile, cultural media, computer hardware, and software were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$223 million worth of Mainland stocks, including CATL, which was a large net buy, Inovance and Wuliangye, which were small net buys. Meanwhile, Kweichow Moutai and Sungrow Power were moderate net sells.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.23 yesterday

- CNY per EUR 7.77 versus 7.79 yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.31% yesterday

- Yield on 10-Year China Development Bank Bond 2.42% versus 2.43% yesterday

- Copper Price +0.38%

- Steel Price +1.70%