Services PMI Beats, Biden & Xi Discuss The San Francisco Vision

3 Min. Read Time

Key News

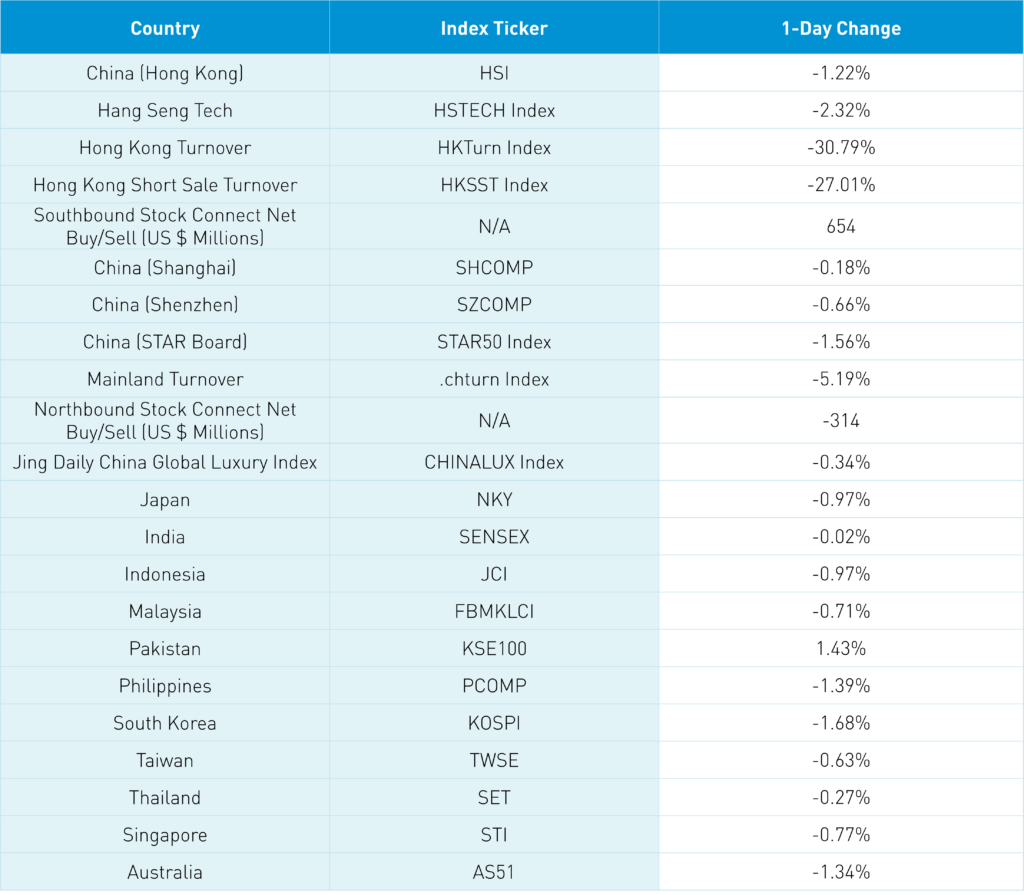

Asian equities were a sea of red overnight as strong US economic data lowered US Fed cut probabilities, along with spiking oil prices on Middle East tensions.

Taiwan was hit with a very strong earthquake, though thankfully, the loss of life appears limited thus far.

Markets were quiet overnight in advance of Hong Kong’s holiday tomorrow for the Ching Ming Festival. Mainland China is also off Thursday and Friday for Tomb Sweeping Day. Both markets were in a risk-off/profit-taking mood as they brushed aside a better-than-expected March Caixin Services PMI of 52.7 versus expectations of 52.5 and February’s 52.5.

President Biden and President Xi spoke for nearly two hours for the first time since their November San Francisco meeting, discussing a number of issues, including fentanyl precursors, Taiwan, and Ukraine, with both calling the conversation “candid and constructive.” Interestingly, the China release noted the implementation of the “San Francisco Vision” to enhance communication between the two militaries, drug control, AI, and climate change.

Janet Yellen leaves for China tomorrow, ruining someone’s four-day holiday plans, followed by Secretary of State Blinken in the coming weeks.

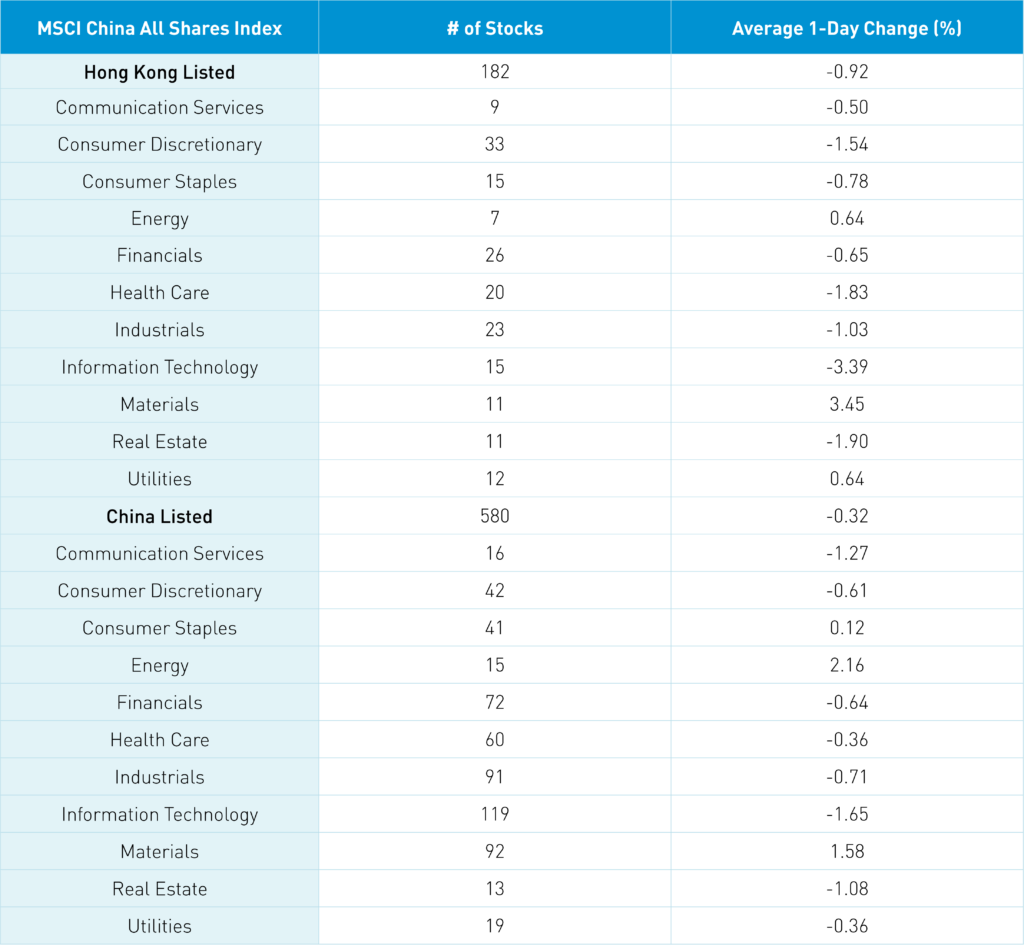

Energy and materials were the two best-performing sectors in Hong Kong and Mainland China, led by higher oil and gold prices.

Tesla’s disappointing sales announced yesterday weighed on the electric vehicle (EV) ecosystem. However, after the close, the China Passenger Car Association reported retail sales of passenger new energy vehicles (NEVs), which include hybrid and fully electric vehicles, increased by +28% year-over-year and by +80% month-over-month to 698,000 units, which brings the year-to-date sales to 1.758 million.

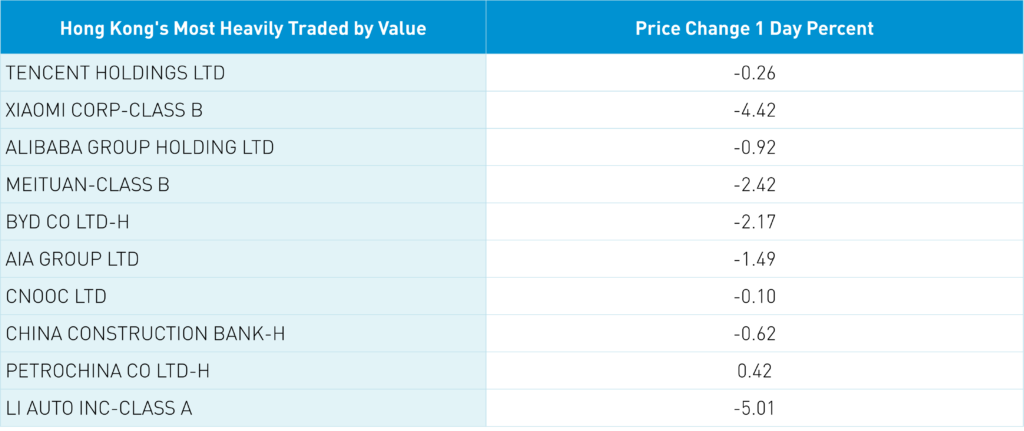

Hong Kong's growth stocks were off, led by the most heavily traded stock by value Tencent. Tencent gained only +0.26% despite today’s buyback of 3.25 million shares. Xiaomi fell -4.42% despite strong sales of their new EV. Alibaba fell -0.92% despite yesterday’s announcement they bought 524 million ordinary shares, the equivalent of 65 million ADRs, for $4.8 billion in Q1 2024. This buyback brings Alibaba's 1-year purchase to 1.249 billion shares (156 million ADRs), for a total of $12.5 billion. Alibaba’s buyback has reduced its shares outstanding by 3.9% in Q1 2024 and 5.1% for the year ended March 2024. Meituan and BYD closed lower by -2.42% and -2.17%, respectively.

Travel stocks were a bright spot in advance of the holiday weekend, with Trip.com up +0.37% and Tongcheng Elong Travel up +0.24%, though the Mainland-listed China Tourism Group fell -1.39%. It is amazing to me that JD.com fell -1.25% after being named in the NDRC statement on consumer upgrade support.

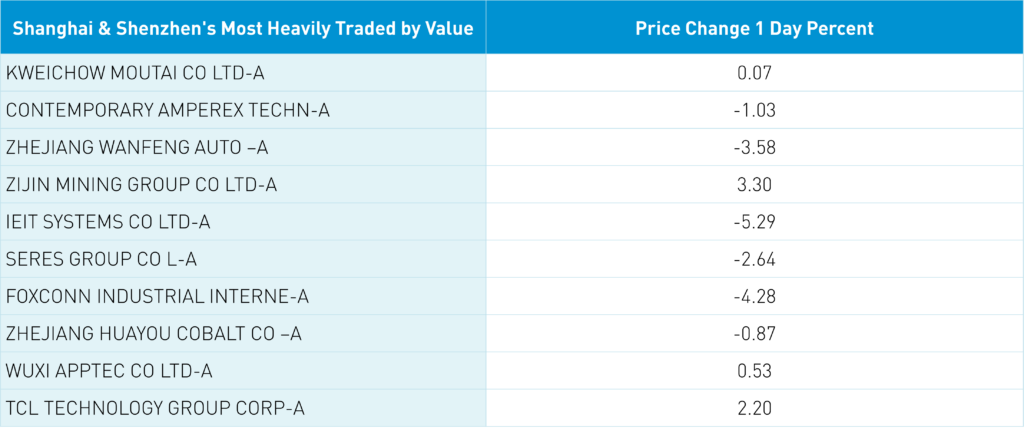

Mainland investors bought the Hong Kong dip with a healthy $654 million worth of net buying via Southbound Stock Connect. Mainland China opened lower and stayed there as Hong Kong's value plays outperformed. Foreign investors sold a net -$314 million worth of Mainland-listed stocks and ETFs via Northbound Stock Connect. Mainland’s most heavily traded stock overnight was Kweichow Moutai, which pulled a James Bond by gaining +0.07% after reporting a net income increase of +17% YoY and rumors famous investor and entrepreneur Dong Yongping may have sold shares despite his denial on social media.

China Last Night will take a break tomorrow for market holidays in both Hong Kong and Mainland China, but we’ll be back on Friday.

The Hang Seng and Hang Seng Tech indexes fell -1.22% and -2.32%, respectively, on volume that decreased -30.79% from yesterday, which is 102% of the 1-year average. 160 stocks advanced, while 304 declined. Main Board short turnover declined -27.01% from yesterday, which is 116% of the 1-year average, as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps fell less than the growth factor and small caps. The top-performing sectors were Materials, which gained +3.45%, Energy and utilities, which both gained +0.64%. Meanwhile, Technology fell -3.39%, Real Estate fell -1.9%, and Health Care fell -1.83%. The top-performing subsectors were materials, business services, and energy. Meanwhile, technical hardware, autos, and media were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $654 million worth of Hong Kong-listed stocks and ETFs, including Xiaomi, Bank of China, and Tencent as small net buys. Meanwhile, the Hong Kong Tracker ETF and XPeng were very small net sells.

Shanghai, Shenzhen, and the STAR Board fell -0.18%, -0.66%, and -1.56%, respectively, on volume that decreased -5.19% from yesterday, which is 105% of the 1-year average. 1,632 stocks advanced, while 3,293 declined. The value factor and large caps fell less than the growth factor and small caps. The top-performing sectors were Energy, which gained +2.15%, Materials, which gained +1.58%, and Consumer Staples, which gained +0.12%. Meanwhile, Technology fell -1.66%, Communication Services fell -1.27%, and Real Estate fell -1.08%. The top-performing subsectors were energy equipment, precious metals, and base metals. Meanwhile, software, communication equipment, and internet were among the worst-performing subsectors. Northbound Stock Connect volumes were light as foreign investors sold a net -$314 million worth of Mainland-listed stocks, including Foxconn, CATL, and Wuxi AppTec, which were moderate net buys. Meanwhile, Zijin Mining was a moderate net sell, Kweichow Moutai and BYD were small net sells. CNY and the Asia Dollar Index were basically flat versus the US dollar overnight. Treasury bonds rallied. Copper gained while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.23 yesterday

- CNY per EUR 7.79 versus 7.77 yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.42% yesterday

- Copper Price +0.71%

- Steel Price -0.09%