Q1 GDP Beats, German Chancellor Visits China

2 Min. Read Time

Key News

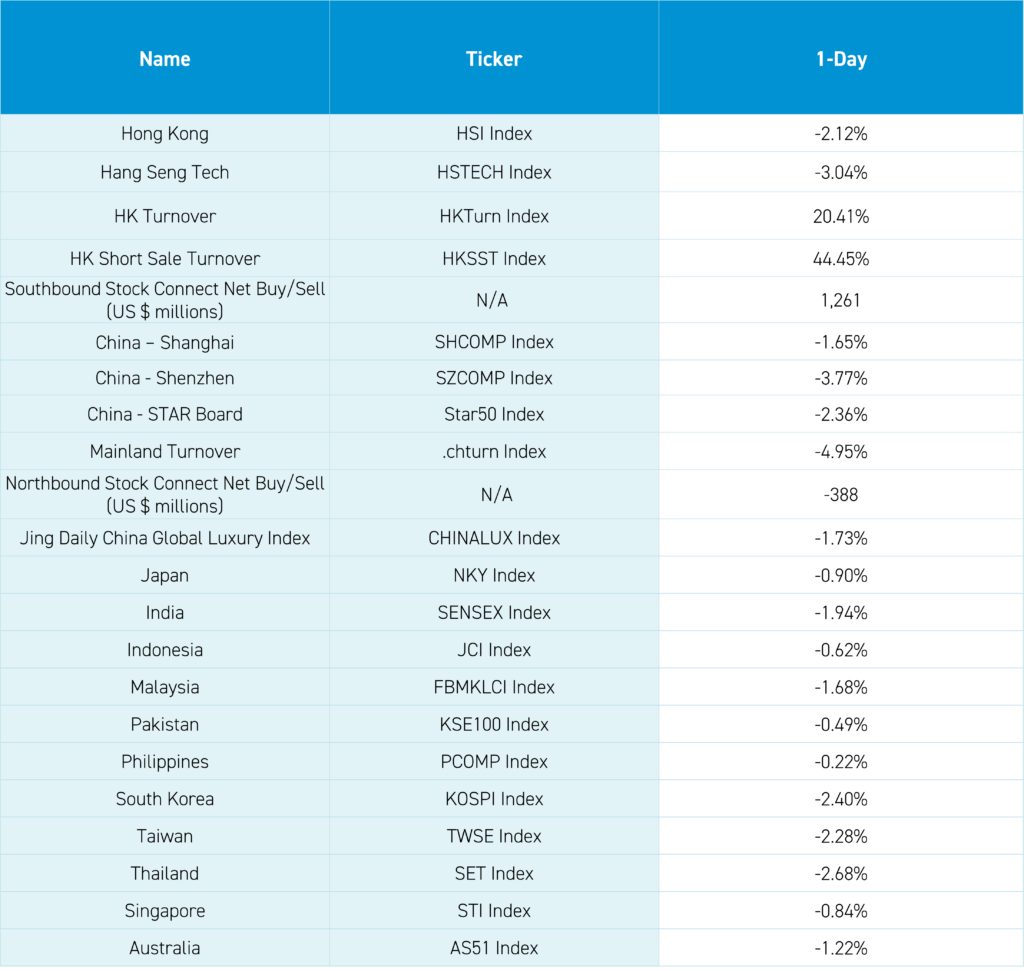

Asian equities were a sea of red overnight on the Iran strikes and mixed macroeconomic data releases.

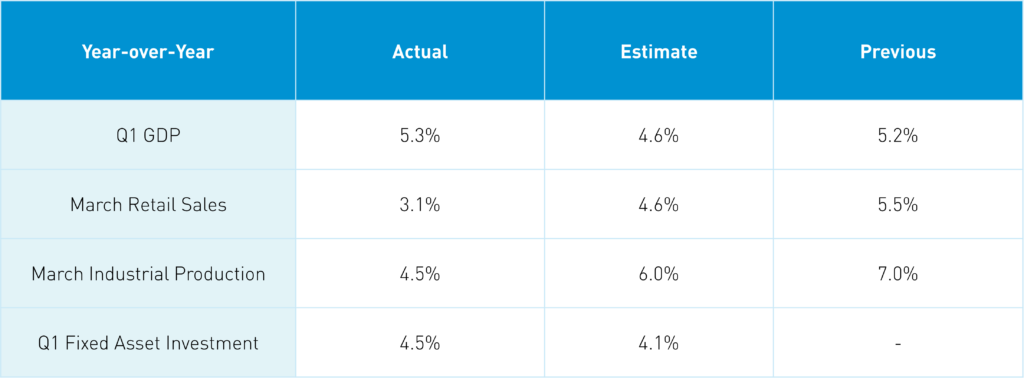

China released Q1 GDP overnight, which beat estimates along with fixed asset investment. However, retail sales came in short of expectations, suggesting that there is more work to be done to stimulate domestic consumption. Markets reacted negatively to this release overall as the year-over-year retail sales figure probably represents one of the first periods in which we can confidently say that the COVID impact has faded, so it was likely heavily scrutinized. After the release, there was some commentary overnight that China’s labor market has improved somewhat, with hiring accelerating in the first quarter, which is positive and could trickle down to improved retail sales down the road. We need to wait and see as economic growth remains fragile after having been supported by export manufacturing in the first few months, which is waning with an increase in excess capacity. Priority #1 for economic chiefs should be domestic consumption!

The Renminbi (CNY), China’s currency, was flat overnight despite the economic release. Bloomberg had an article noting that the currency is becoming more expensive to short, as the PBOC’s interventions to maintain its value have slowed. The central bank likely believes the currency can appreciate somewhat on its own.

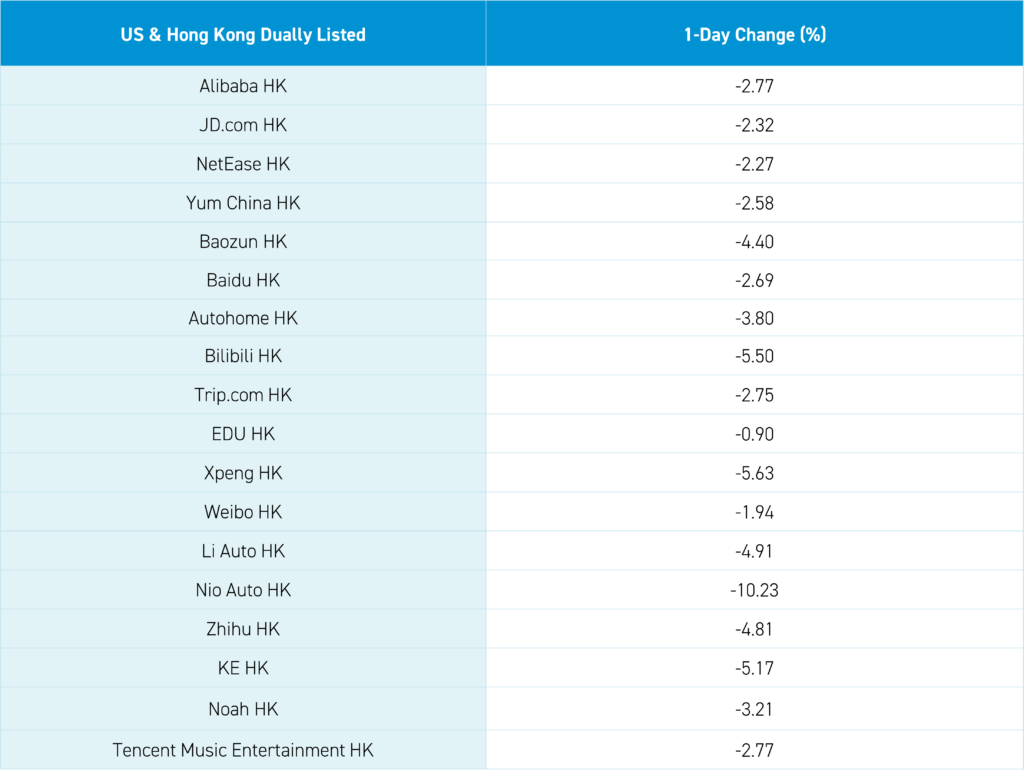

Baidu announced that its ERNIE AI-powered chat bot has crossed the 200 million user mark. However, this did not help the company’s stock, which fell -3% along with the broader technology and internet sectors. Energy and defensive plays outperformed again overnight as a risk-off atmosphere appears to be enveloping global markets.

German Chancellor Olaf Scholz is in Beijing Meeting with senior officials to discuss how China can help pressure Russia to end its war in Ukraine and come to the negotiating table. China’s unique relationship with Russia places the nation in an advantageous position to exert influence. China has so far remained neutral regarding the conflict and refrained from supplying weaponry. Scholz having a dialogue with Chinese leaders is positive for a variety of reasons. However, whether trade will be on the agenda for his current visit remains to be seen.

China released a draft proposal to further tighten its emissions caps, which, if implemented, would be the first major upgrade of its climate policy in many years. The move could boost prices in China’s burgeoning emissions trading system.

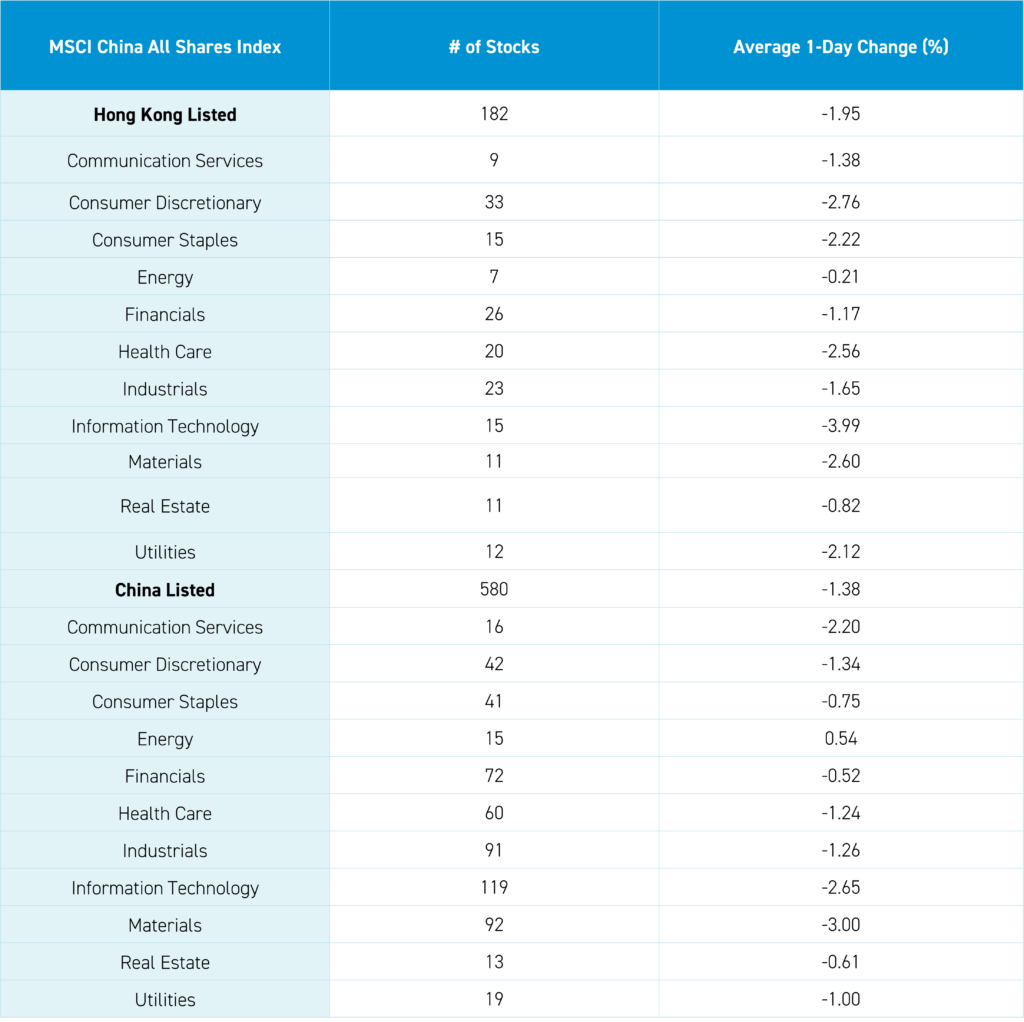

The Hang Seng and Hang Seng Tech indexes fell -2.12% and -3.04%, respectively, on volume that increased +20% from yesterday. Mainland investors bought a net $1.3 billion worth of Hong Kong-listed stocks and ETFs via Southbound Stock Connect overnight. The top-performing sectors were Energy, which fell -0.21%, Real Estate, which fell -0.82%, and Financials, which fell -1.17%. Meanwhile, the worst-performing sectors were Information Technology, which fell -3.99%, Consumer Discretionary, which fell -2.76%, and Materials, which fell -2.60%.

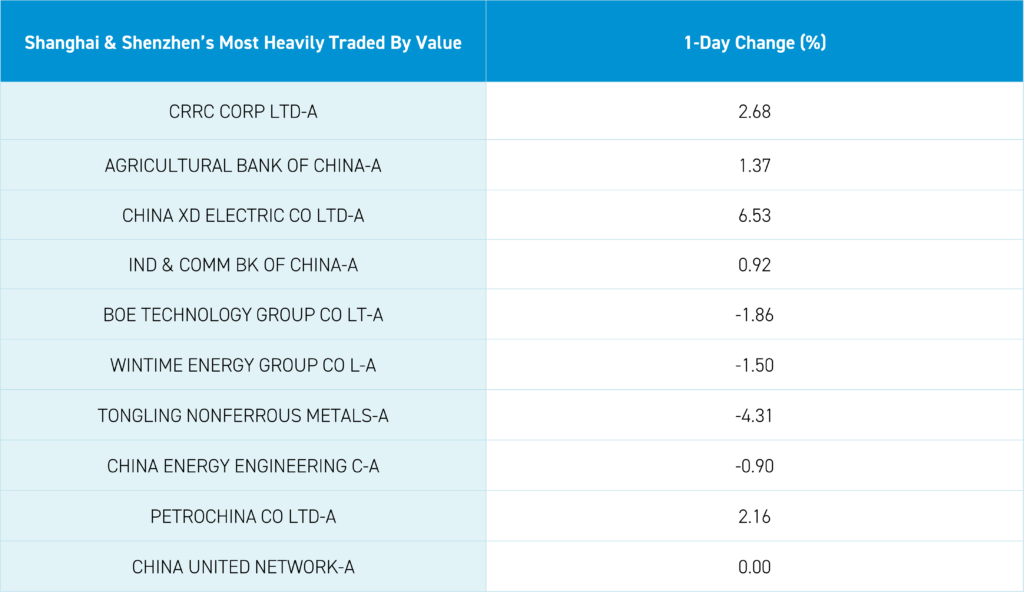

Shanghai, Shenzhen, and the STAR Board all closed lower by -1.65%, -3.77%, and -2.36%, respectively, on volume that decreased -5% from yesterday. Foreign investors sold a net -$388 million worth of Mainland-listed stocks overnight via Northbound Stock Connect. The top-performing sectors were Energy, which gained +0.54%, Financials, which fell -0.52%, and Real Estate, which fell -0.61%. Meanwhile , the worst-performing sectors were Materials, which fell -3.00%, Information Technology, which fell -2.65%, and Communication Services, which fell -2.20%.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY per EUR 7.70 versus 7.69 yesterday

- Yield on 1-Day Government Bond 1.40% versus 1.44% yesterday

- Yield on 10-Year Government Bond 2.27% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.37% versus 2.39% yesterday

- Copper Price -0.48%

- Steel Price -0.14%