China Technology’s Outperformance vs. US Tech Since February Widens

3 Min. Read Time

Key News

Asian equities had a strong day as Middle East tensions eased, except for Mainland China, which underperformed.

Hong Kong had a strong day after the China Securities Regulatory Commission (CSRC), China’s SEC, announced policies aimed at bolstering Hong Kong’s status as a financial hub. The measures seek to broaden Stock Connect rules related to ETFs and REITs that trade in RMB and facilitate more IPOs from “leading enterprises”.

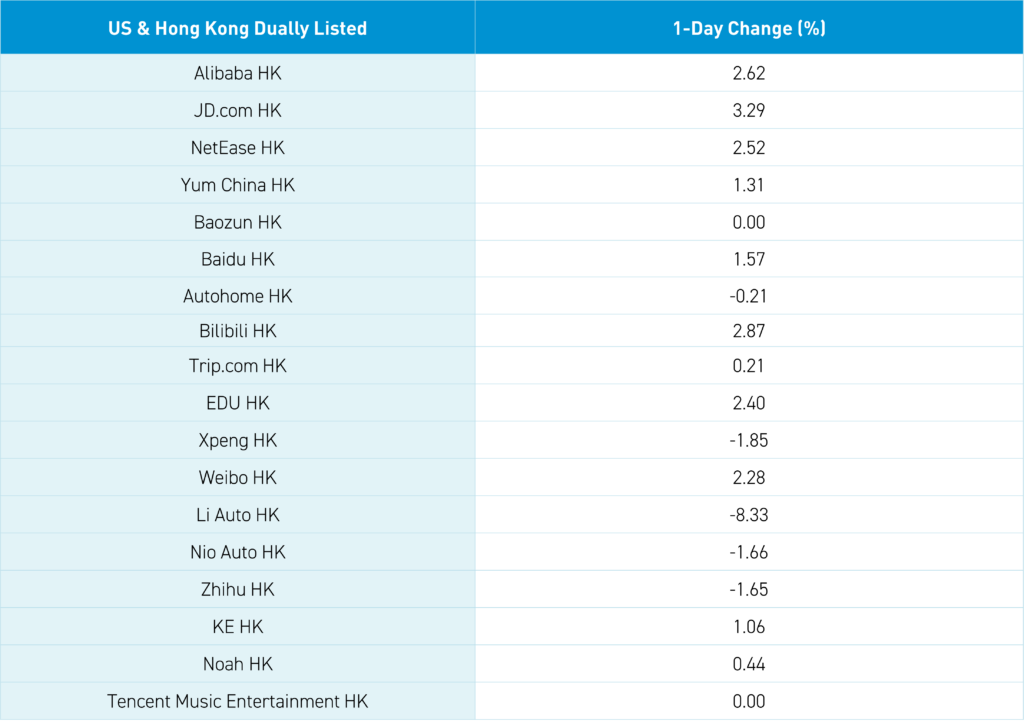

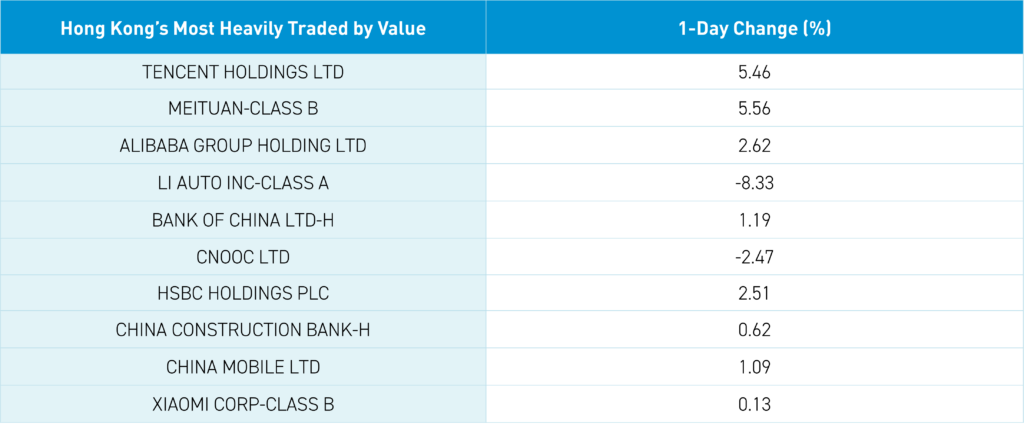

Hong Kong’s market was led by higher internet stocks. The most heavily traded stocks by value were Tencent, which gained +5.46% as the company announced May 21st as the release date of the widely anticipated game Dungeon & Fighter, Meituan, which gained +5.56% on another $4 million stock buyback, Alibaba, which gained +2.62%, Li Auto, which fell -8.33% on more price cuts for electric vehicles and light initial demand for a new model, and the Bank of China, which gained +1.19%. It is also worth noting that Tencent bought back another 3.2 million shares today. Other internet stocks rose as well, including Kuaishou Technology, which gained +1.92%, NetEase, which gained +2.52%, JD.com, which gained +3.29%, Baidu, which gained +1.57%, and Trip.com, which gained +0.21%.

The Hang Seng Tech Index is beating the Nasdaq 100 by more than 10% since its low on February 2nd, through last Friday. But, you will really only read about that here! Yes, it is only two-and-a-half months of outperformance, but we will take it!

The market did not care about the House passing a bill including the TikTok forced sale, though, even after it passes the Senate and is signed into law, it will be challenged in court, where it will likely be overturned. It is amazing to me that the media does not mention TikTok’s parent Bytedance is owned by US private equity firms, who control three of the five board seats and have invested in the company on behalf of US pensions, endowments, and foundations.

There has also been scant media coverage of economic meetings between the US and China at the International Monetary Fund (IMF). The Chinese Navy is hosting a four-day meeting with thirty global senior Navy leaders and Secretary of State Blinken, who is headed to China on Wednesday.

The Loan Prime Rate (LPR) was left unchanged, as had been expected.

Shanghai and Shenzhen bounced around the room to close the session lower, as China’s 10-year Treasury Yield closed at a new low that was last seen in April of 2002 (2.24%). There was no evidence of activity by the National Team (institutional investors associated with China’s sovereign wealth). Their favored ETFs saw below average volumes. After the close, the State Council announced a special study to support the capital markets, including fraud prevention, and “promot[ing] listed companies to enhance their awareness of repaying investors”. The top-down encouragement of companies to pay dividends and buy back stocks should capture investors’ attention.

Remember, the National Team is not buying the Chinese stock market. They are buying the companies that have the most influence and weight in China indexes. This is why mega-caps should be where investors focus their attention among Mainland China-listed stocks. It is not about 300 stocks or 600 stocks because those smaller companies do not have any impact on the index!

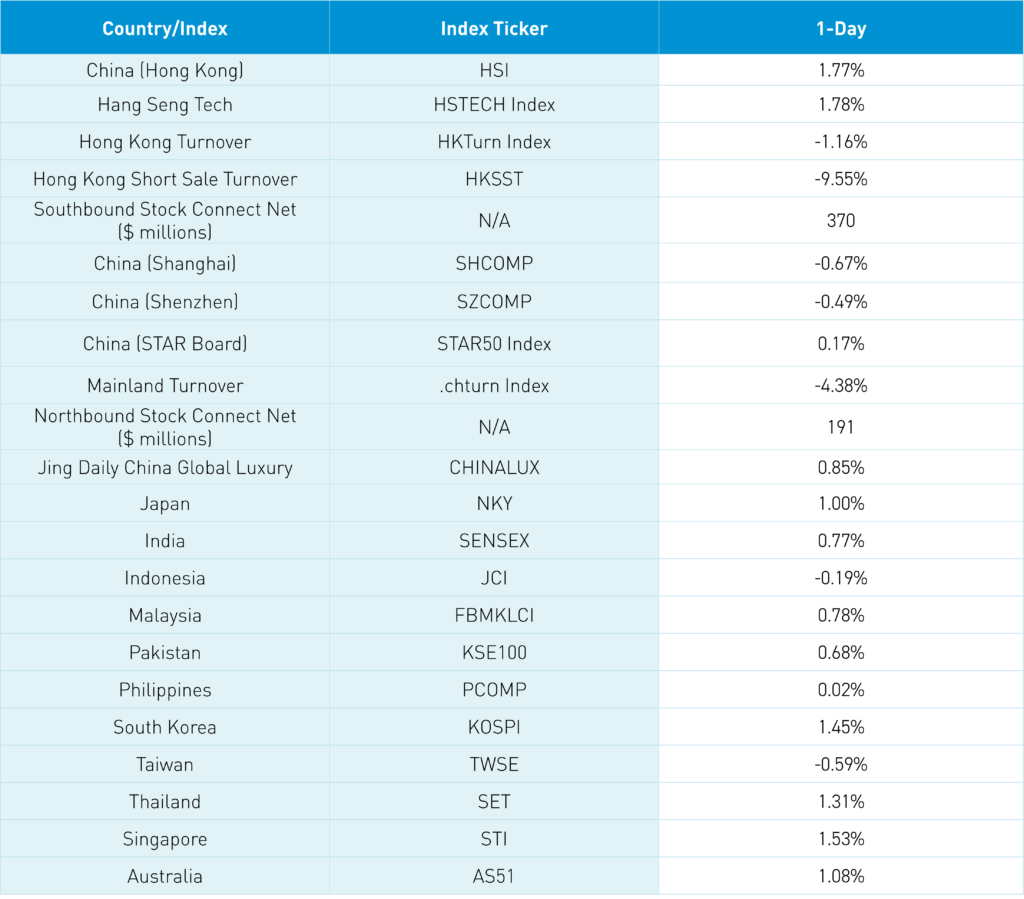

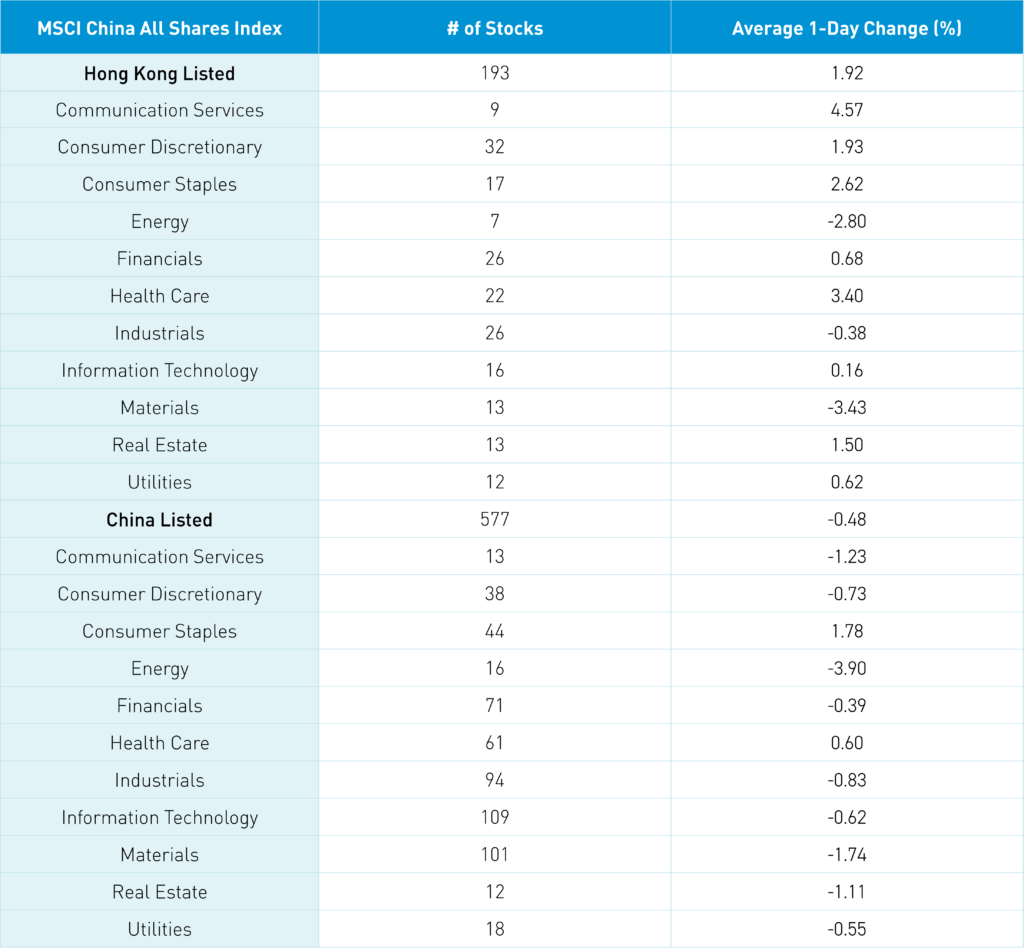

The Hang Seng and Hang Seng Tech indexes gained +1.77% and +1.78%, respectively, on volume that decreased -1.16% from Friday, which is 108% of the 1-year average. 337 stocks advanced, while 141 declined. Main Board short turnover declined -9.55% from Friday, which is 112% of the 1-year average, as 19% of turnover was short turnover (remember HK short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Communication Services, which gained +4.57%, Health Care, which gained +3.40%; and Consumer Staples, which gained +2.62%. Meanwhile, Materials fell -3.43%, Energy fell -2.8%, and Industrials fell -0.38%. The top-performing subsectors were software, retailing, and food/beverages, while materials, energy, and auto were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $370 million worth of Hong Kong-listed stocks and ETFs.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.67%, -0.49%, and +0.17%, respectively, on volume that decreased -4.38% from Friday, which is 96% of the 1-year average. 2,016 stocks advanced, while 2,911 declined. The growth factor and small caps outperformed the value factor and large caps. Consumer Staples and healthcare gained +1.79% and +0.60%, respectively, while energy was down by -3.89%. Meanwhile, Materials fell -1.74%, and Communication Services fell -1.22%. The top-performing subsectors were motorcycle, agriculture, and soft drinks. Meanwhile, energy equipment, coal, and precious metals were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $191 million worth of Mainland stocks. CNY and the Asia Dollar Index were off slightly versus the US dollar. Treasury bonds rallied. Copper was higher while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY Per EUR 7.70 versus 7.71 yesterday

- Yield on 1-Day Government Bond 1.30% versus 1.33% yesterday

- Yield on 10-Year Government Bond 2.24% versus 2.25% yesterday

- Yield on 10-Year China Development Bank Bond 2.31% versus 2.32% yesterday

- Copper Price +1.39%

- Steel Price -0.16%