Markets Pause on Headlines

4 Min. Read Time

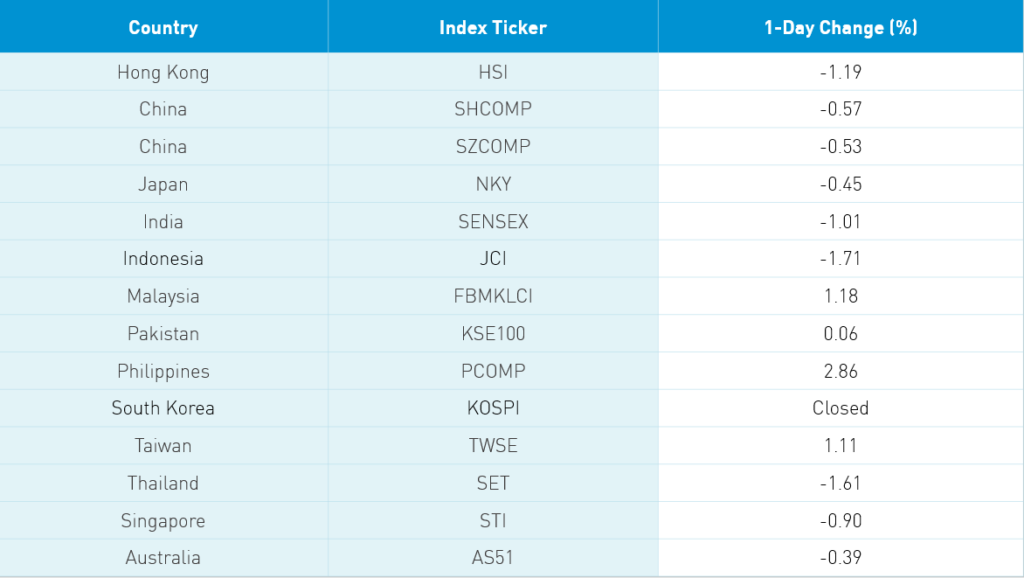

Key News

Asian equities were largely lower in a quiet night of trading as President Trump’s defunding of the WHO, the fall in oil prices, and disappointing US earnings weighed on market sentiment. South Korea was closed for their election. Mainland China had small boost mid-morning as the PBOC cut the Medium-term Lending Facility by 0.2% to 2.95%, which implies an April 20th cut in the Loan Prime Rate. Although it was no surprise, the move came early as it was expected to occur on Friday when China reports Q1 GDP, industrial production, and retail sales. The cut led to an injection of $14B into the banking system.

The Mainland rally was short-lived as home appliance maker Gree (000651 Ch) -3.54%, the Mainland’s most heavily traded stock today, announced a Q1 earnings warning due to an inability to install appliances during the quarantine. The company projects a net profit fall of 77% year over year. The warning weighed on discretionary names such as competitor Midea Group (000333 CH) -0.55%. It is worth noting that foreign investors were buyers of the popular stocks on weakness via the Northbound Connect trading venue. Energy names were weak on oil’s drop as Hong Kong-listed oil giants were the three worst performers within the Hang Seng. Real estate was off in both the Mainland and Hong Kong on disappointing sales results. One broker said several real estate firms were accused of colluding on pricing a land deal in Shanghai though I failed to see that verified elsewhere. The three most heavily traded stocks in Hong Kong were Tencent 0.0%, Alibaba’s HK listing +0.46% and smart phone manufacturer Xiaomi +2.95% which announced a 24mm share stock buyback program.

Overnight, I received an interesting report on active managers’ performance. Within the EM space, active managers largely underperformed due to a low China country weight versus the benchmark as the country held up better than most. We have noted that a re-rating of China positions amongst active EM managers could be a beneficial tailwind. Another factor was the outperformance of growth versus value. Emerging Market indexes are split almost 50/50 between growth and value from a sector perspective. We all know the last decade has been a growth market, which explains an element of EM’s underperformance. If we eliminate the value sectors from EM, low and behold EM isn’t that bad! The commodities bear market for the last decade hasn’t helped EM and neither has a strong dollar. Obviously, I can’t predict if growth will continue to outperform, but there are arguments for why due to the global quarantine. For instance, asset-light companies are more likely to be able to work from home. Only time will tell!

H-Share Update

The Hang Seng opened higher but slid the remainder of the day -1.19%/-290 index points to close at 24,145. Volume was above the 1-year average and up slightly from yesterday while breadth was awful with only 5 advancing stocks and 42 decliners. The index was led lower by AIA -2.23%/-54 index points, HSBC -2.05%/-41 index points. Energy giant CNOOC was the day’s worst performer -5.18%/-23 index points. The three worst performers were all energy stocks. Shenzhou International was the best performer +2.81%/+6 index points followed by Apple supplier Sunny Optical +1.36%/+3 index points. Hong Kong-domiciled companies outperformed Chinese companies -0.97% versus -1.25% using the HS HK 35 and HS China Enterprise Indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.9% led lower by energy -4.03%, real estate -3.64%, staples -1.67%, industrials -1.48%, financials -1.03%, communication -0.31% and health care -0.09%. Tech had a strong day +1.51%, discretionary +0.74% and utilities +0.18%. Mainland investors were active buyers of Hong Kong stocks via the Southbound Connect trading venue though top volume companies Sunac and Tencent saw sellers outpace buyers by a small margin. China Construction Bank had 6 to 1 buyers. Mainland investors bought $201mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 9.5% of Hong Kong’s turnover.

A-Share Update

Shanghai & Shenzhen opened lower, staged a midday comeback, lost steam and then stalled out as markets slid into the close. Shanghai and Shenzhen were off –0.57% and -0.53% as volume picked up +8% from yesterday, which is above the 1-year average. Breadth was off with 1,075 advancing stocks and 2,620 declining as small and mid-caps held up slightly better than large caps. The Mainland stocks within the MSCI China All Shares Index fell -0.57% with only tech positive +0.46%. Real estate was the worst sector -1.51%, discretionary -1.34%, materials -1.02%, energy -0.9%, staples -0.75%, financials -0.73%, utilities -0.67%, industrials -0.48%, health care -0.31% and communication -0.24%. Foreign investors were active buyers of Mainland stocks via the Northbound Connect trading venue with Shanghai volumes light while Shenzhen volumes surprisingly higher. Remember Shanghai is mostly large caps and State-Owned Enterprises while Shenzhen is mostly private companies with some large but mainly mid and small-cap companies. MSCI inclusion stock Kweichow Moutai was bought 3 to 1 though Ping An was sold 2 to 1 on Shanghai. Foreign investors were buyers of Gree and Midea on weakness. Foreign investors bought $475mm worth of Mainland stocks today as Northbound Connect trading accounted for 5.1% of the Mainland’s turnover.

Last Night’s Prices & Yields

- CNY/USD 7.07 versus 7.05 yesterday

- CNY/EUR 7.70 versus 7.72 yesterday

- Yield on 1-Day Government Bond 0.49% versus 0.63% yesterday

- Yield on 10-Year Government Bond 2.55% versus 2.56% yesterday

- Yield on 10-Year China Development Bank Bond 2.84% versus 2.85% yesterday

- Commodities on the Shanghai & Dalian Exchanges were lower with Dr. Copper -0.48%