Earnings Take Center Stage, TAL Revenues In-Line

4 Min. Read Time

Key News

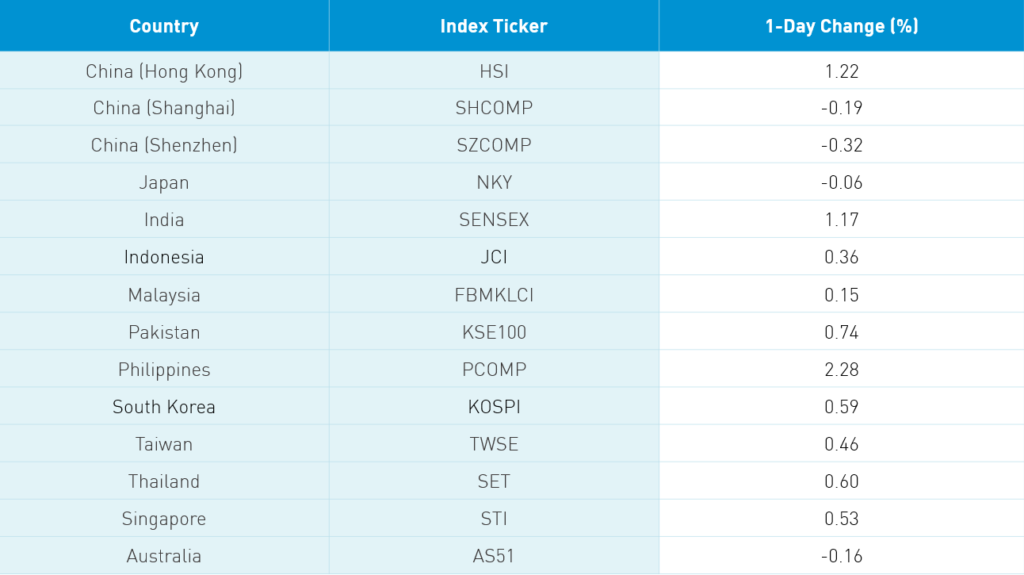

Asian equities posted modest gains with holidays on the horizon. Mainland China had a roller-coaster day as the Shenzhen Stock Exchange announced new, relaxed IPO rules that sent indices plunging in the morning. More IPOs mean more supply and competition for investors’ cash from existing holdings to potential IPOs. Nonetheless, the mainland markets recovered to end the session only slightly lower.

Strong earnings results from liquor companies Kweichow Moutai (600519 CH) +0.25% and Wuliangye Yibin (0000858 CH) +4.75% helped Mainland markets. There was some chatter that investors may sell stocks in advance of the coming holiday though that is anyone’s guess. Hong Kong saw a similar morning swoon but rebounded strongly to close near the day’s high. HSBC’s (5HK) noon cautious/mixed earnings release initially sent the stock falling to -1.14%. But, as we saw with US bank stocks following the announcement of their need to beef up cash for loan losses, the stock rebounded +1.14%. The rebound, in turn, lifted Hong Kong-listed financials on the day. Online publisher China Literature (772 HK) gained +14.4% after announcing it had replaced its CEO with an executive from Tencent. The company was formed out of a partnership between Tencent and private equity firm Caryle Group’s online publishing businesses. Rumor has it that Tencent will now do more to support the company. Hong Kong’s most heavily traded stocks Tencent (700 HK) and Alibaba (9988 HK) diverged, ending the session +1.02% and -0.8%, respectively.

The largest oil ETF in the US has garnered attention as it vaporizes its NAV/share price by rolling out of expiring futures contracts into futures contracts several months out, which cost more. The oil futures will cost more in the future than they do today (June $11.14, July $18.35, August $21.83, and September $25.67). When we “roll” into later contracts we can’t buy as much exposure due to the future price costing more than the price today. US investors aren’t the only ones to get vaporized as a Hong Kong-listed oil ETF also pursued self-destruction in the same manner. There were also reports that the Bank of China sold over $1.4 billion of oil exposure investment products to retail investors. Extreme moves such as these absolutely crush investors, who use leverage in a lesson that is seldom learned.

There are multiple reports that China’s SEC, the CSRC, is investigating Luckin Coffee after having raided their headquarters due to a change in law that allows the regulator to prosecute frauds despite the company being listed in the US. I hope they throw the company executives involved in jail, which appears likely. There is talk that the CSRC is involving the SEC, which is a welcome sign as increased communication is exceedingly important. Mainland investors are suing the company in China in a suit which will likely be expanded to include US investors. The company’s coffee shops are still open as the company has a real business though clearly the results were inflated.

TAL Education (TAL US) reported mixed Q4 and fiscal year results before the US market open. Expectations were low going into the release, which should making for an interesting day of trading. The online education space has performed well long-term, but, in the short-term, the announcement that Chinese schools would start on time in the fall quelled fears of a shortened summer break. An early school year start would have potentially limited time for online school time over the summer. I should threaten my own kids with this….

- Revenue +18% to $857mm from $726mm

- Loss from operations -$43mm from $114mm

- Student Enrollment +56.6% to 4,646,040

- EPS -$0.15

- Q1 Revenue Forecast $875mm to $895mm

- $500mm stock repurchase to implemented over the next 12 months

H-Share Update

The Hang Seng overcame a morning swoon to gain +1.22%/+295 index points to close at 24,575 on light volume off -1.3% from yesterday and below the 1-year average. Breadth was strong with 44 advancers and 5 decliners as index heavyweights AIA +1.2%/+30 index points, Tencent +1.02%/+28 index points and China Construction Bank +1.3%/+26 index points. Today’s best performer was China Overseas Land & Investment +3.53%/+11 index points while China Unicom was the worst performer -1.74%/-1 index point. Hong Kong-domiciled companies outperformed Mainland-domiciled companies gaining +1.36% versus +1.09% using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.1% led higher by tech +2.11%, staples +1.73%, financials +1.4%, energy +1.3%, industrials +1.23%, real estate +1.19%, communication +0.98%, materials +0.7%, discretionary +0.59% and health care +0.51%. Utilities was off -0.32%. Southbound Connect trading was closed with the upcoming holidays.

A-Share Update

Shanghai and Shenzhen plunged shortly after the open -2.03% and -3.25%, respectively, but managed to rebound into the green before slipping slightly to close -0.19% and -0.32%. Volume surged +20% from yesterday and above the 1-year average. However, breadth was bad with 840 advancers and 2,879 decliners. Large and mid-caps outperformed small caps as mega-caps actually ended the day positive. The Mainland stocks within the MSCI China All Shares Index gained +0.66% led higher by tech +1.73%, staples +1.55%, real estate +1.04%, financials +0.84%, communication +0.5%, health care +0.43%, discretionary +0.05% and utilities +0.02%. Industrials, materials, and energy lost -0.06%, -1.11% and -1.24%, respectively. Northbound Connect volumes were moderate. Foreign investors were active buyers of Mainland stocks. Volume leader and MSCI inclusion stock Kweichow Moutai saw sellers outpace buyers by a small margin while Ping An Insurance saw buyers outpace sellers. Foreign investors bought $146mm worth of Mainland stocks as Northbound Connect trading accounted for 5.4% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.08 versus 7.09 yesterday

- EUR/CNY 7.67 versus 7.68 yesterday

- Yield on 1-Day Government Bond 0.62% versus 0.57% yesterday

- Yield on 10-Year Government Bond 2.53% versus 2.53% yesterday

- Yield on 10-Year China Development Bank Bond 2.81% versus 2.82%

- Commodities on the Shanghai & Dalian Exchanges were lower with Dr. Copper -0.61%