Bargain Hunters Lift Hong Kong

3 Min. Read Time

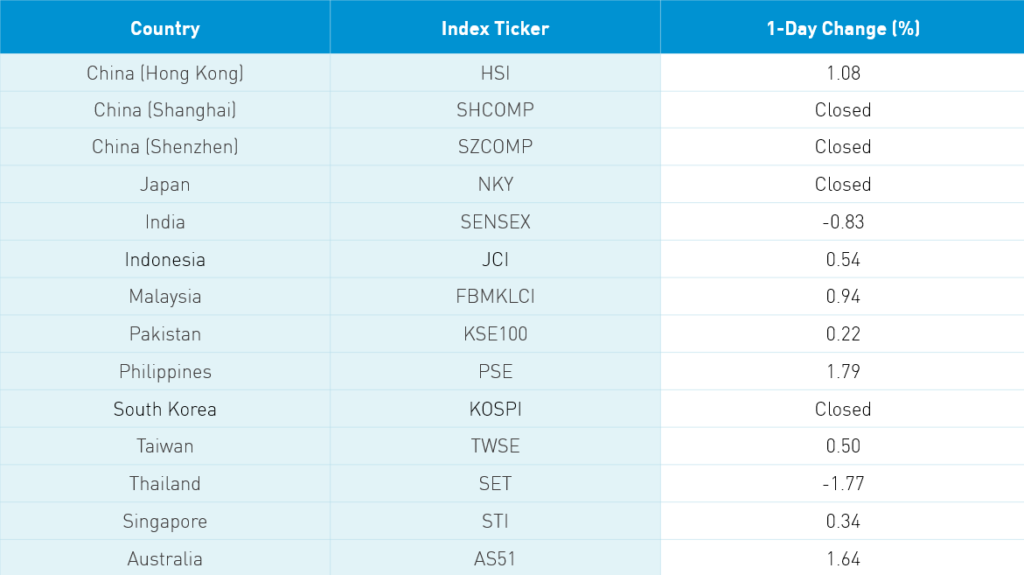

Key News

Bargain hunters were active across Asian equities following yesterday’s carnage though volumes were weak as Mainland China, Japan, and South Korea remain on holiday. Hong Kong rebounded today despite rather grim Q1 GDP (-8.9% YoY) and March retail sales (-40% YoY) releases. The local government has begun lifting its social distancing measures with gyms and bars being allowed to reopen. Autos had a strong day, which lifted the discretionary sector. Investors are positioning themselves for a rebound in car sales. Analyst comments on Geely (175 HK) lifted the stock +4.68%. Alibaba HK (9988 HK) was the most heavily traded stock today off -0.63% as short selling increased on speculation that US-listed shares were being converted to Hong Kong shares to be sold. Tencent (700 HK) was up +1.5% following an analyst’s positive comments while Meituan Dianping (3690 HK) was up +3.57%.

Mainland markets will reopen tomorrow with US-listed Chinese A-shares ETFs trading at nearly a -6% discount. The US market is predicting a fall in the Mainland market though it is worth noting that Hong Kong-listed Chinese A Share ETFs are “predicting” a -3% fall. I suspect the Mainland market could do better than expected despite rising US political rhetoric as Mainland investors will be focused on the coming “Two Sessions” economic meetings. The meetings are likely to see further stimulus measures announced. I suspect infrastructure and real estate development could be beneficiaries given yesterday’s move to list real estate and infrastructure REITs.

Multiple sources claim that Netease (NTSE US) has filed to re-list in Hong Kong following last week’s report that JD.com will do so and Alibaba’s listing in Hong Kong late last year. The development is positive as Asian investors are apt to recognize the company’s potential. If the companies are added to local indices such as the Hang Seng they will also benefit from passive investment flows. Furthermore, they could be added to Southbound Connect, which would lead to significant buying from Mainland investors who previously would have found it difficult to own the stock. There are rumors that Alibaba’s inclusion in Southbound Connect may occur in June. The move to re-list is disconcerting in that US capital markets may be losing some of their prestige with foreign companies.

Online gaming and software company Kingsoft (3888 HK) was up +0.96% as the coming IPO of its Kingsoft Cloud (ticker KC), its cloud computing business, is expected to list Friday on Nasdaq. The company will issue 25 million shares with pricing later this week of between $16 to $18 a share. Book runners include JP Morgan, UBS, Credit Suisse, and CICC. Cloud is obviously a hot spot in our new Work From Home (WFH) world. Considering present market conditions, it will be interesting to see investors’ reception of the IPO.

Reuters reported that the Federal Thrift Savings Plan will have three new board members appointed from the administration who are expected to negate a move from MSCI EAFE (developed market) to MSCI All Country World ex US (developed and emerging markets). ACWI ex US has China as the second-largest country at 11.25%, behind Japan’s 17.38% and ahead of the UK’s 9.96%. Choosing an ACWI ex US and ex China benchmark shouldn’t be a problem for the plan. However, lost from the plan will be the #1 holding Alibaba and #3 holding Tencent.

Emerging Market underperformance has been driven by the benchmark’s value bias due to its heavier weighting of financials, energy, industrials, and materials. While broad EM ETFs have lost AUM, investors have pivoted to EM ESG and Ex SOE strategies. While it appears these strategies outperform, this is mainly due to their heavier weighting of growth sectors rather than their headline methodologies. This begs the question as to why investors wouldn’t just own the growth sectors?

H-Share Update

The Hang Seng gained +1.08%/254 index points after yesterday’s debacle though volumes were light -35% from yesterday and below the 1-year average. Breadth was strong with 44 advancers and 5 decliners led by Tencent +1.5%/+40 index points, HK Stock Exchange +2.92%/+26 index points, and the day’s best performer Techtronic Industries +8.86%/+24 index points. Hang Lung Properties was the day’s worst performer -2.48%/-2 index points. Hong Kong-domiciled companies outperformed Chinese companies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index +1.07% led higher by autos in discretionary +2.61%, energy +1.97%, tech +1.37%, communication +1.31%, staples +1.29%, health care +0.88%, materials _0.66%, financials +0.56%, industrials +0.24% and utilities +0.18%. Southbound Connect remains closed.

A-Share Update

Mainland Markets Closed