Tencent Earnings Beat Estimates, MSCI To Increase China Weight in EM Index By 1%

3 Min. Read Time

We will be hosting a webinar on the reopening of China's economy and investing after COVID-19 tomorrow at 8:30 am EST.

Please click here to sign up!

Key News

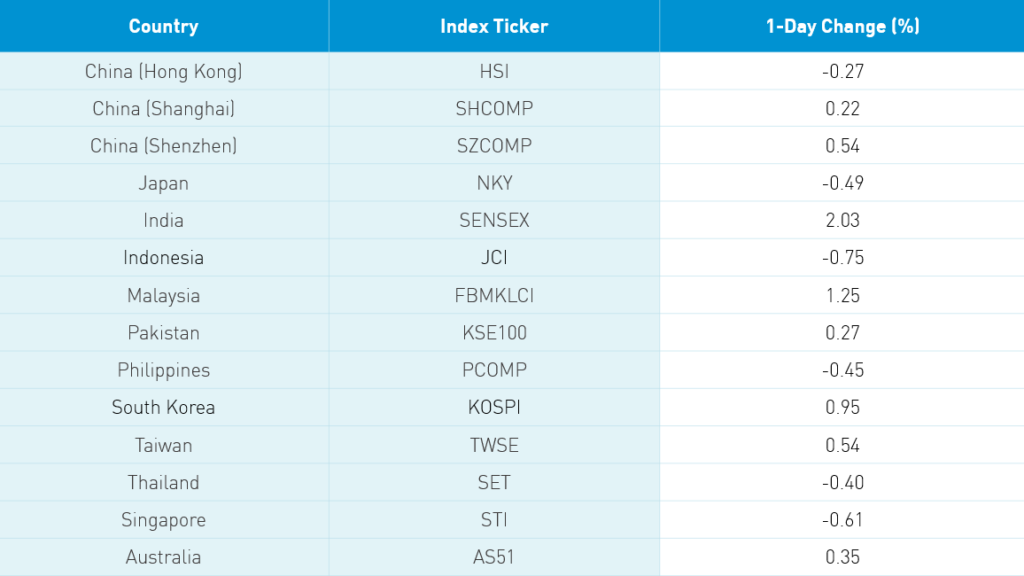

Asian equities had a mixed session last night as Hong Kong slipped while the Mainland market overcame morning losses to post a small gain. Healthcare had a strong day in both markets as coronavirus fears persist. Jilin Province will reimpose a quarantine. Hong Kong volume leader Tencent (700 HK) eased -0.32% ahead of its earnings release while Meituan Dianping jumped +5.45% on news that MSCI would increase its index weight. Alibaba HK followed its US share class -1.7%. Next Monday we will find out whether Meituan and Alibaba HK will be added to the Hang Seng index. Staples had a strong day in the Mainland market led by liquor stocks.

According to the South China Morning Post, China may focus on the unemployment rate before addressing growth targets. With so many jobs having recently moved to a services sector populated by smaller, private firms, ensuring they can return to their jobs via state mandates might be difficult. Fortunately, tech companies can help keep unemployment low through work from home productivity platforms. A study performed by Trip.com showed that companies may see productivity increases by offering work from home as a permanent option to employees. In the US, Twitter has announced that employees will now have the option to work from home permanently.

Tokyo laid out details on new laws restricting foreign investment in national darlings through amending Japan's Foreign Exchange and Foreign Trade Acts. This comes just as Beijing is lifting restrictions such as limits on capital repatriation. Japan, which used to be an "open market", is now closing off somewhat to foreign investment while China is opening.

After the close, MSCI released its pro forma for the end of the month Semi-Annual Index Rebalance which requires MSCI benchmarked ETFs and index funds to rebalance. I went out on a limb to predict that China’s percent weight in MSCI Emerging Markets would rise due to China’s strong relative outperformance. MSCI announced that China’s weight would indeed rise from 40.6% to 41.6% as 56 additions and 45 deletions brings China’s total number of stocks to 715 out of EM’s 1,391 holdings. The second largest country in the Emerging Markets Index is now Taiwan at 12.3%/88 stocks as South Korea slips to 1.5%/107 stocks. China’s % weight is more than 3X all of EM Europe/Middle East/Africa’s 12.5% and 5X EM Latin America’s 7.9%. Among China additions is BILI while Meituan Dianping will see a weight increase.

Tencent (700 HK) reported Q1 results after the close in Hong Kong. The results look strong to me! Remember that this company’s market cap is $529 billion. It is very difficult to find a company this large growing this fast. Tencent is the largest holding in the MSCI ACWI ex-US. What a shame this great company will likely be excluded from the Federal Thrift Savings Plan. So be it! I am going to coin the term PESG as a variant of ESG with the P standing for Political.

- Revenues +26% YoY to RMB 108.065B versus estimate RMB 101.071B

- VAS (online gaming segment) +27% YoY to RMB 28.9B versus estimate RMB 23.64B

- Online Advertising Revenue +32%

- WeChat Monthly Users 1.202 billion

- Operating Profit +25% YoY to $5.201B (RMB 37.26B) versus estimate RMB 23.64

- Operating Margin 34%

- Net Income RMB 28.896B

- Cash $31B

H-Share Update

The Hang Seng had a choppy day closing -0.27%/-65 index points at 24,180 on volumes +6.6% higher than yesterday. Breadth was mixed with 22 decliners and 26 advancers as AIA was off -1.44%/-34 index points, HSBC -1.02%/-19 index points, and Hong Kong Exchanges +1.19%/+11 index points. Sino Biopharma was the day’s best performer +2.74%/+7.5 index points while China Unicom was the worst performer -2.24%/-2 index points. China-domiciled companies outperformed Hong Kong-domiciled companies +0.04% versus -0.12% using the HS China Enterprise and HS Hong Kong 35 indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.19% led higher by staples +2.53%, health care +1.71%, real estate +0.47%, materials +0.4%, tech +0.27% and industrials +0.07%. Energy -0.07%, utilities -0.21%, financials -0.24% and communication services -0.3%. Southbound Connect volumes were light/moderate though Mainland investors were buyers of Hong Kong-listed stocks. Volume leaders Tencent and Metiuan Diangping were bought while Semiconductor Manufacturing was sold. Mainland investors bought $437mm worth of Hong Kong stocks today as Southbound Connect turnover accounted for just over 8% of HK turnover.

A-Share Update

Shanghai and Shenzhen opened lower but traveled from lower left to upper right closing +0.22% and +0.67% on volumes off -3% from yesterday. Breadth was mixed with 1,794 advancers and 1,776 decliners. Mid and small caps outperformed large caps by ~50bps. The Mainland stocks within the MSCI China All Shares Index gained +0.29% led higher by healthcare +1.54%, staples +1.1%, communication +0.25%, tech +0.17%, materials +0.16% and utilities +0.07%. Real estate -0.07%, financials -0.11%, industrials -0.17%, energy -0.24% and discretionary -0.61%. Northbound Connect volumes were moderate in mixed trading. Volume leader Kweichow Moutai had net buyers by a slim 5 to 4 ratio while Gree Electric Appliances had sellers outpace buyers 5 to 4. Foreign investors sold -$28mm worth of Mainland stocks today as Northbound Connect accounted for just 5% of Mainland turnover.

Last Night's Prices & Yields

- CNY/USD 7.09 versus 7.08 yesterday

- CNY/EUR 7.70 versus 7.70 yesterday

- Yield on 1-Day Government Bond 0.68% versus 0.83% yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.01% yesterday