Services PMI Shows Strongest Expansion Since 2010, NetEase CFO Comments on Hong Kong Listing

4 Min. Read Time

Key News

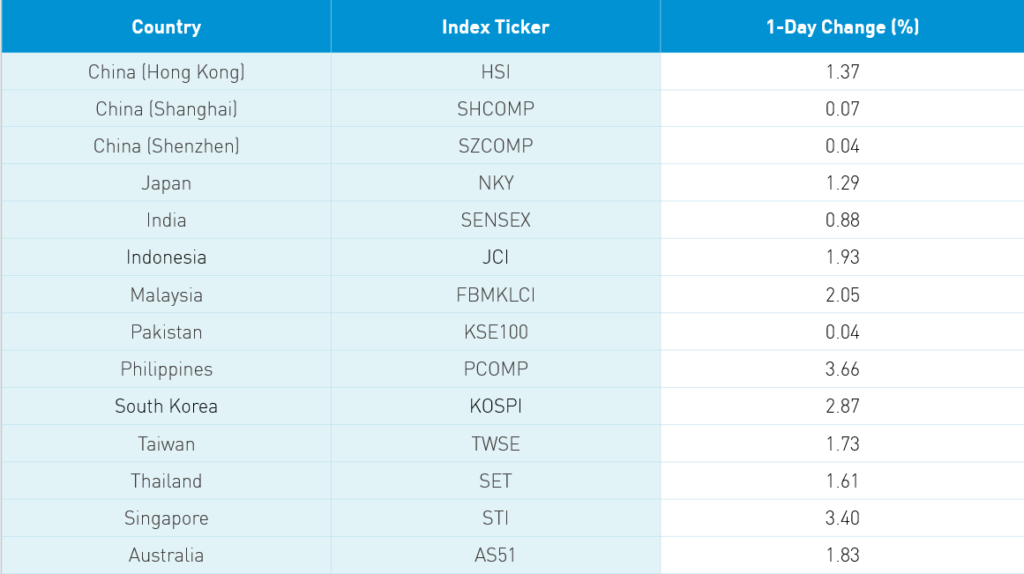

Asian equities had another strong day as markets enjoyed the lack of US-China political rhetoric. Hopefully, both sides recognize this phenomenon. It is worth noting that the Philippines has been on a tear, gaining over 10% in the last week. Hong Kong’s most heavily-traded stocks by value were the growth companies led by Tencent +0.51%, Alibaba HK +4.8%, and Meituan Dianping +5.57% though it was a strong and broad rally today. It is worth noting that Mainland investors took some profits in Tencent and Meituan via Southbound Stock Connect as both stocks have been on a tear of late.

Takeaway: The Caixin release is compiled by IHS Markit (NYSE ticker INFO), which surveys private companies. The rebound in May was the strongest expansion since September 2010 according to the release and best reading since January. The media only likes bad news so this is likely the only place you’ll read this! Export data continues to lag as the economic consequence of the global quarantine dampens external demand. Employment has also been slower to rebound as companies cut costs. Nonetheless, business activity reached the highest level in ten years while new orders were stronger as China’s first-in-first-out rebound continues. The business outlook was also strong as companies believe in an economic rebound.

CNBC had a good article on Tencent’s latest potential blockbuster game called Valorant via its investment in Riot Games. You can gain some street cred by mentioning it to the younger generation. In other gaming news, NetEase’s Hong Kong listing is scheduled for June 11th as one broker noted it is oversubscribed 44 times! Meanwhile, preparations for Alibaba’s 6/18 sales festival appear to be going very well according to chatter as Apple is participating in what I’m told is a first.

Hong Kong-domiciled companies outperformed China-domiciled companies in Hong Kong as the lack of bite to the US bark on the new security law is giving the Hong Kong economy some hope. Mainland China sold off into the close managing small gains despite the strong Services PMI though autos continue to show strength as auto sales may have troughed. Traditional Chinese medicine stocks did well after positive policy comments following the Two Sessions.

SEC Chairman Jay Clayton was interviewed yesterday on Bloomberg TV on the topic of delisting US listed Chinese companies. Headlines screamed he endorsed a delisting as “sensible” though the full interview exhibits a more balanced view and gave some optimism that a resolution could be found. He voiced some angst that this issue has dragged on for almost a decade, with which I sympathize. He made an interesting point that smaller companies were different from large companies and private companies were different from state-owned, implying a different set of disclosure standards. Applying a “monolithic” approach doesn’t make sense. It is too bad the interviewer didn’t ask him what happens to shareholders! Is it sensible for US investors to punished? If a delisting threat were to materialize, institutional investors will covert their US holdings to Hong Kong shares. Individual investors, unaware of a delisting or convertibility, would be completely left out! It is worth noting that Mainland-listed China Pacific Insurance will list a GDR, the UK’s version of an ADR, on the London Stock Exchange. I don’t know how the UK regulator handles the audit issue. Capital flows to where it is treated best. Unfortunately, jobs consequently flow to where to capital is located. There is still no word on when the House will vote on the Equitable Act nor if it will go to committee.

Staying with the topic du jour, I participated in an institutional broker’s conference call with NetEase’s CFO and head of investor relations yesterday. NetEase’s Hong Kong filing begins with a break up letter from its CEO as it notes the 20th anniversary of their Nasdaq listing. However, the CEO notes that the rationale for relisting in Hong Kong is the fact that US investors have failed to understand the company. The CFO noted that NetEase has provided a 26% annualized return in the last 20 years while providing a nice dividend. I calculated the return from the 6/29/2000 IPO to yesterday’s close as a +12,034%, which equals a 27% annualized return. The company had grown from 200 employees when it listed to over 20,000 today. He communicated that he felt a cooperative solution to the PCAOB issue was possible. He also stated that adding relisted stocks to Southbound Connect was likely to occur. I asked him for further details on the PCAOB issue and he gave some candid feedback. He agreed China should amend the rules but noted that the issue has become too political. Nonetheless, he believed it would be solved. Let’s hope so!

H-Share Update

The Hang Seng opened higher and stayed there, gaining +1.37%/+329 index points to close at 24,325 on volume that jumped 22% from yesterday and was well-above the 1-year average. Breadth was strong with 40 advancers and 6 decliners as AIA jumped +3.89%/+96, HSBC +2.55%/+48 index points and Ping An Insurance +2.04%/+29 index points. Energy giant CNOOC was the best performer +4.6%/+23 index points while CSPC Pharma was the worst -1.95%/-4 index points. Hong Kong-domiciled stocks outperformed China-domiciled stocks +1.48% versus +0.92% using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.18% led higher by discretionary +3.82%, energy +3.48%, tech +1.44%, health care +1.25%, financials +1.02%, utilities +0.97%, materials +0.73%, industrials +0.72%, communication +0.51%, real estate +0.34%, and staples +0.12%.

Southbound Stock Connect volume was light/moderate in mixed trading as several stocks were net sold today by Mainland investors. Volume leader Meituan Dianping was sold 2 to 1, while Tencent and Seminconductor Manufacturing were sold by small amounts. Mainland investors still bought $146mm worth of Hong Kong stocks today as Southbound Connect trading accounted for nearly 7% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gave up gains into the close though ended the day +0.07% and +0.04%. Volumes were up very slightly though remained above the 1 year average. Breadth was mixed with 1,835 advancers and 1,768 decliners as large, mid and small caps were inline with one another. The Mainland stocks within the MSCI China All Shares Index were off -0.06% led higher by healthcare +0.66%, discretionary +0.48%, energy +0.45%, utilities +0.13%, tech +0.06%, materials +0.00%, industrials -0.13%, financials -0.15%, communication -0.38%, real estate -0.52%, and staples -0.65%. Northbound Stock Connect volumes were moderate/high as foreign investors were net buyers of Mainland stocks. It is interesting to note that the top volume names were net sold by small amounts: Wuliangye Yibin, Kweichow Moutai and Ping An Insurance. Foreign investors bought a total of $620mm worth of Mainland stocks today while Northbound Connect trading accounted for 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.12 versus 7.10 yesterday

- CNY/EUR 8.00 versus 7.94 yesterday

- Yield on 1-Day Government Bond 1.02% versus 0.85% yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.10% yesterday