JD.com Releases Details On Hong Kong Listing as Stocks Climb The Wall of Worry, Week In Review

6 Min. Read Time

Week In Review

- Asian equities were largely higher on Monday after President Trump's speech lacked actionable items resulting from increasing political tensions between the US and China. China released its official PMI figures for May. Both China's manufacturing and non-manufacturing PMIs were in growth territory. However, employment was in contraction territory.

- Baozun, which assists Western companies in selling into China's market, released Q1 earnings on Tuesday. While the company reported top line growth, ballooning expenses for the quarter weighed on the bottom line. NetEase, JD.com, Pinduoduo, Trip.com, and Baidu have all applied to list in Hong Kong in search of a better valuation.

- The May Caixin Services PMI, which, unlike the official metric, mostly covers smaller, private companies, was released on Wednesday. The metric, which came in at 55, chronicled the largest monthly expansion since 2010 as China's economy recovers with a vengeance.

- In a sign of goodwill, China loosened inbound flight restrictions on US airlines on Thursday. It was also announced that FTSE will be adding Alibaba HK and Alibaba Healthcare to its China 50 Index, which will cause passive managers who replicate the index to trade those stocks on June 18th.

Friday's Key News

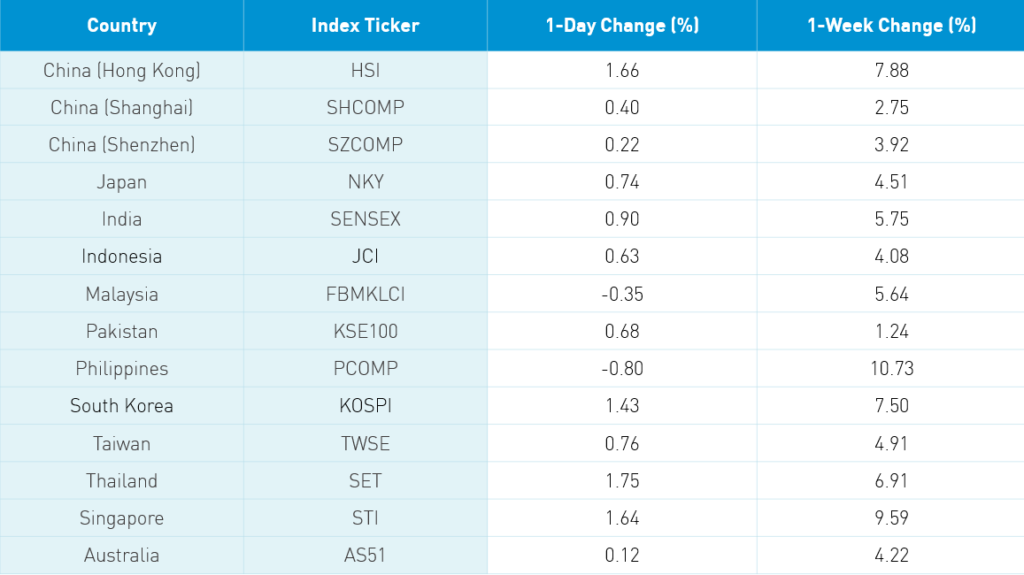

Asian equities finished a strong week on a high note as US-China political rhetoric made a positive turn, European stimulus was extended, and global quarantines continue to ease. US Trade Representative Lighthizer negated the WSJ article stating that China has slowed agriculture purchases by announcing significant soybean purchases this week. We also saw a thaw in the US-China travel spat yesterday as both countries decided to ease flight restrictions.

Hong Kong had a strong day driven by news of China’s support of Hong Kong as a financial center and the rebalancing of Hang Seng indexes. Growth names were soft. The most heavily traded stocks were Tencent -0.18%, HSBC +4.25%, Meituan Dianping, which finally took a breather, was down -3.17%, and Alibaba HK +0.57%. Why the weakness in growth stocks? One explanation could be the coming Hong Kong listings of NetEase and JD.com as growth investors will need cash to participate. There has been so much money flowing into Hong Kong to participate in IPOs that Hong Kong had to sell HKD in order to keep the currency from appreciating versus the USD and maintain its peg. Hong Kong financials and real estate had a good day as beaten up value stocks have rallied of late. The value rebound, which has become a global phenomenon, is simply a catch up to growth names. A reversion is taking place. However, I prefer growth to value in the long run.

The Mainland managed a late-day rally led by travel and airline stocks within the discretionary sector. The Mainland has been has seen a modest rally as recent policy on supporting private companies has led investors to believe policies will be incremental. It is worth noting that bond yields have increased a touch over the last week. Foreign investors bought over $3.3B worth of Mainland stocks this week.

The White House issued a memorandum on “Protecting US Investors from Significant Risks from Chinese Companies”. The good news is that the Secretary of the Treasury and others will form a working group to evaluate US-listed Chinese companies’ lack of PCAOB auditing. It will provide its findings in sixty days. I will try to find out if this raises the feasibility that the House sends the Senate bill to committee. In reading the release, it shows the frustration from the PCAOB and SEC in trying to find an outcome on this issue that has dragged on for years. The memorandum’s language is fairly pessimistic as it fails to acknowledge the significant gains US investors have enjoyed in these companies. Our friend Henry pointed out that NetEase’s gains since its IPO on 6/29/2000 to yesterday are 11,926% versus Amazon’s 6,323% and the Nasdaq Composite’s +203%! It fails to recognize the significant number of US jobs supported by these companies listing in the US, which span investment banking, trading, law and accounting. It also fails to acknowledge the $1 trillion in US savings invested in these stocks. Ultimately China should allow the PCAOB to audit the auditors though punishing US investors is not the answer. I believe the small number of State Owned Enterprises are the issue as allowing private companies to hand over their paperwork shouldn’t be an issue, whereas requiring SOEs to do so may be seen as encroaching on sovereignty. Ultimately, institutional investors will simply convert US shares to Hong Kong shares though we are several years from this becoming a necessary.

Despite all the commotion, Dada Nexus (DADA US) is preparing its US IPO selling 20mm shares at a price of $16, which would raise $320mm. Dada Nexus is an “on-demand retail platform” providing local merchant delivery. The company has strong partnerships with both JD.com and Walmart. A big heads up to our friend Evelyn of CNBC.com in Beijing on the DADA heads up.

Also important is the fact that US-listed Chinese companies continue to buy back their US shares. If you thought the stocks would be delisted, why would you spend hundreds of millions buying the stock back? NetEase’s CFO said he has confidence that the issue can be resolved. It is difficult to ascertain, but it feels like the China side believes a it is just a matter of time before a resolution is reached. However, exactly how long it will take remains to be seen.

JD.com’s Hong Kong listing details indicate the company will sell 133mm shares at HKD 219/$56.52 under the ticker 9618 HK. Next week, NetEase will list in Hong Kong following Alibaba’s successful Hong Kong listing in November 2019. The Hong Kong listings have nothing to do with the PCAOB/political rhetoric but everything to do with valuation. US investors don’t properly value the stocks so they are going to relist in Asia where investors know that these are great companies. The upside for Americans is that the US and Hong Kong stocks are completely convertible so the US shares should follow the Hong Kong shares in price. JD would raise $3.759B though, if there is demand, it can sell another 19.5mm shares and raise up to $4.322B. The over-allotment shares are called the green shoe. You can try to impress your family by saying something like “Demand for JD’s HK listing is strong so the green shoe is going to get filled.” However, my attempts to build credibility with my family this way have been unsuccessful.

H-Share Update

The Hang Seng overcame weakness in the morning to post a strong rally and close at the day’s high +1.66%/404 index points at 24,770. Volumes were +7% from yesterday and 50% higher than the 1-year average. Breadth was strong with 47 advancers and 3 decliners. The index was led higher by HSBC +4.25%/+84 index points. Today’s best performers were Hang Seng Bank +8.45%/+26 index points and AIA Group +0.85%/+21 index points. Today’s worst performer was China Mengniu Dairy -1.33%/-3 index points. Hong Kong-domiciled stocks +2.41% versus China-domiciled stocks +0.56% using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.45% with tech +2.91%, energy +1.8%, real estate +1.52%, financials +1.35%, industrials +1.23%, communication -0.06%, materials -0.21%, health care -0.22%, utilities -0.86%, and staples -1.01%.

Southbound Connect volumes were light in mixed trading as Mainland investors sold Hong Kong stocks. We’ve seen a few net selling days though they are quite rare. Tencent and Semiconductor Manufacturing were both sold by small amounts. Mainland investors sold $62mm worth of Hong Kong stocks today while Southbound Connect trading account for just over 6% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen had a choppy day but moved higher by the end of the session to close +0.4% and +0.22%, respectively. Volumes were down -2% from yesterday though remained above the 1-year average. Breadth tilted negative with 1,527 advancers and 2,096 decliners as large, mid and small caps traded in line. The Mainland stocks within the MSCI China All Shares Index gained +0.98% with communication +2.03%, discretionary +1.77%, tech +1.43%, healthcare +1.29%, industrials +1.05%, financials +0.9%, staples +0.77%, energy +0.55%, utilities +0.49%, real estate +0.13%, materials +0.07%.

Northbound Connect volumes were moderate to light though buying activity was strong. Volumes leaders Kweichow Moutai and Ping An saw moderate buying while Gree Electric Appliances saw buyers outpace sellers bu 2 to 1. Foreign investors bought $611mm worth of Mainland stocks today while Northbound Connect accounted for just under 5% of Mainland trading. For the week, foreign investors bought $3.378B worth of Mainland stocks!

Last Night’s Prices & Yields

- CNY/USD 7.09 versus 7.15 yesterday

- CNY/EUR 8.01 versus 7.89 yesterday

- Yield on 1-Day Government Bond 1.13% versus 1.07% yesterday

- Yield on 10-Year Government Bond 2.85% versus 2.75% yesterday

- Yield on 10-Year China Development Bank Bond 3.17% versus 3.00% yesterday