Xiaomi, China Health Care, and Mainland Equities Sing Bob Seger’s “Night Moves”, Week In Review

4 Min. Read Time

Please fill out this quick survey to help us improve China Last Night.

We are pleased to announce the launch of our latest model portfolio: the Krane All China Growth Strategy.

Click the link to learn more.

Week In Review

- Tencent’s strong performance on Monday was driven by President Trump’s clarification that US multinationals can continue to use WeChat. A loss of the use of WeChat would present a major difficulty to US companies conducting business in China as alternatives to the messenger are often unavailable on the Mainland.

- Ant Group filed the prospectus for its Hong Kong IPO on Tuesday. Formerly Ant Financial, Ant Group has become a fintech giant after expanding from being Alibaba’s official payment processor. At a valuation of $200 billion, the offering is likely to be the largest this year globally.

- WuXi Biologics CEO Chris Chen expressed confidence on Wednesday that his company would have a Covid-19 vaccine available by year-end.

- Bilibili, a US-listed Chinese online entertainment platform for “young generations in China”, reported Q2 results after the US close on Wednesday. The company grew revenues by +70% to RMB 2.62 billion compared to an estimated RMB 2.55 billion.

Key News

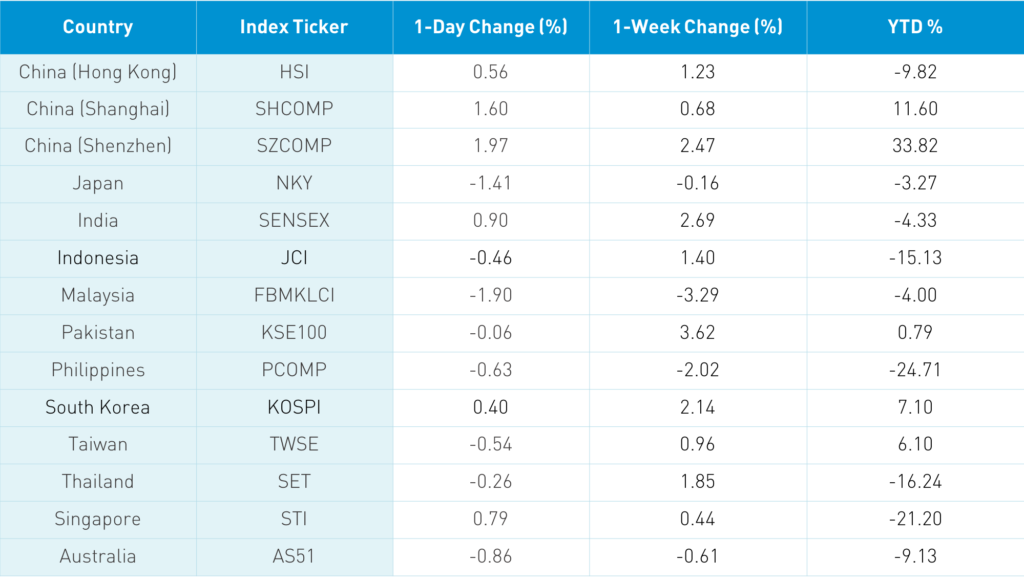

Asian equities ended a positive week on a high note except for Japan, which declined following Prime Minister Abe’s resignation. Take a look at the weekly return numbers for Hong Kong and China below. Surprisingly good, right? At the very least, they are certainly not what you might think based on recent headlines. Hong Kong volume leader Xiaomi gained +5.39% on the day following great earnings earlier in the week and in advance of its inclusion in the prestigious Hang Seng Index on Sept 7th. However, other galloping growth names took a breather. Tencent fell -3.14%, Allibaba HK fell -1.28%, Meituan Dianping fell -2.14%, ZhongAn Online P&C Insurance fell -2.88%, and JD.com HK fell -2.59%.

The first-ever ETF benchmarked to the Hang Seng Tech Index launched in Hong Kong overnight. The Mainland markets gained on a slow news day. However, there was talk that the influx of IPOs (supply) had capped gains in the mainland for the short term. The DND trade (drinks and drugs, or pharmaceuticals and alcohol companies) did very well as investors appear to be recognizing that China’s health care industry will benefit from a vaccine. The Wall Street Journal had a good article on the CanSino Biologics (6185 HK) vaccine that is worth reading. Alcohol stocks Kweichow Moutai and Wuliangye Yibin rose +1.5% and +1.02%, respectively, on talk that baiju prices may increase. It is worth noting that China’s currency, the renminbi, continues to appreciate against the US dollar, picking up 0.4% overnight and 0.75% for the week. Foreign investors bought $1.16 billion worth of Mainland stocks this week, which brings the YTD total to $19 billion.

How many companies have grown revenue more than 25% in the last year with a market capitalization over $500 billion? Only four: Amazon, Berkshire Hathaway, Alibaba and Tencent.

Some of our clients believe that they have missed the boat regarding China stocks as China’s performance has been great year-to-date. Despite this outperformance, US-listed Chinese equity ETFs are not seeing significant inflows. Year-to-date, Chinese equity ETFs have lost $352mm/-1.81% worth of AUM. It’s not a China thing it’s a non-US thing. Year-to-date, Emerging Market ETFs have lost $10 billion/-5.69% worth of AUM. The three biggest EM ETFs have lost $5.4B, $4.9B, and $3.9B year-to-date. Another EM ETF has lost $1B. Ouch. The problem for broad EM and many China ETFs is that many are overweight to value in a global growth market. Growth China and Growth Emerging Markets are both doing well.

The South China Morning Post is reporting that Yum China will relist in Hong Kong.

The Wall Street Journal published a great article on ByteDane/TickTok founder Zhang Yiming.

MSCI’s Quarterly Index Review and China’s “official” PMIs release are both scheduled for Monday.

Social media companies Sina and Weibo report next Wednesday.

H-Share Update

The Hang Seng was having a great day until a late afternoon tumble clipped gains to +0.56%/+140 index points at 25,422. Volume was nearly 2X the 1-year average while breadth was positive with 33 advancers and 13 decliners. Volume leaders included AIA, which rose +4.06%/115 index points, Tencent, which fell -3.14%/-94 index points, and HSBC, which rose +2.1%/+44 index points. Hong Kong-domiciled companies had a strong day +1.56% versus -0.19% for China-domiciled companies using the HS HK 35 and China Enterprise Indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.6% with staples +3.52%, tech +2.92%, health care +1.51%, real estate +0.86%, utilities +0.18%, industrials -0.04%, financials -0.22%, energy-0.36%, materials -0.46%, discretionary -1%, and communication -2.74%.

Southbound Stock Connect volumes were moderate to light as Mainland investors were net buyers of Hong Kong stocks. Shanghai Connect volume leader was Xiaomi, which was bought 9 to 7, Tencent, which was bought 7 to 4, and Meituan Dianping, which was sold 2 to 1. Mainland investors bought $550mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 9.6% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened lower but went from the lower left to the upper right to close +1.6% and +1.97% at 3,403 and 2,305, respectively. Volume rose +13%, which is just above the 1-year average while breadth was positive with 2,437 advancers and 1,225 decliners. Large, mid, and small caps moved uniformly higher. The 510 Mainland stocks within the MSCI China All Shares Index rose +2.44% with health care +3.54%, discretionary +3.09%, financials +2.76%, staples +2.71%, materials +2.24%, real estate +2.04%, communication +1.95%, industrials +1.93%, tech +1.58%, utilities +1.28%, and energy +0.79%.

Northbound Stock Connect volumes were moderate as foreign investors were net buyers of Mainland stocks. Shanghai Connect volume leaders were Kweichow Moutai, which was bought by a small margin, Ping An, which was bought slightly, and China Tourism, which was sold 7 to 6. Shenzhen Connect volume leaders were Wuliangye Yibin, which was sold 11 to 8, BOE Technology, which was bought by nearly 4 to 1, and Gree Electric Appliances, which was bought nearly 4 to 1. Foreign investors bought $938mm worth of Mainland stocks today as Northbound Stock Connect trading accounted for 7.1% of Mainland turnover. For the week, foreign investors bought $1.16 billion worth of Mainland stocks, bringing the YTD total to $19 billion.

Last Week’s Exchange Rates & Yields

- CNY/USD 6.87 versus 6.89 yesterday

- CNY/EUR 8.16 versus 8.13 yesterday

- Yield on 1-Day Government Bond 1.02% versus 1.15% yesterday

- Yield on 10-Year Government Bond 3.07% versus 3.06% yesterday

- Yield on 10-Year China Development Bank Bond 3.63% versus 3.61% yesterday