Powell Press Conference Leaves Doves Crying

2 Min. Read Time

Key News

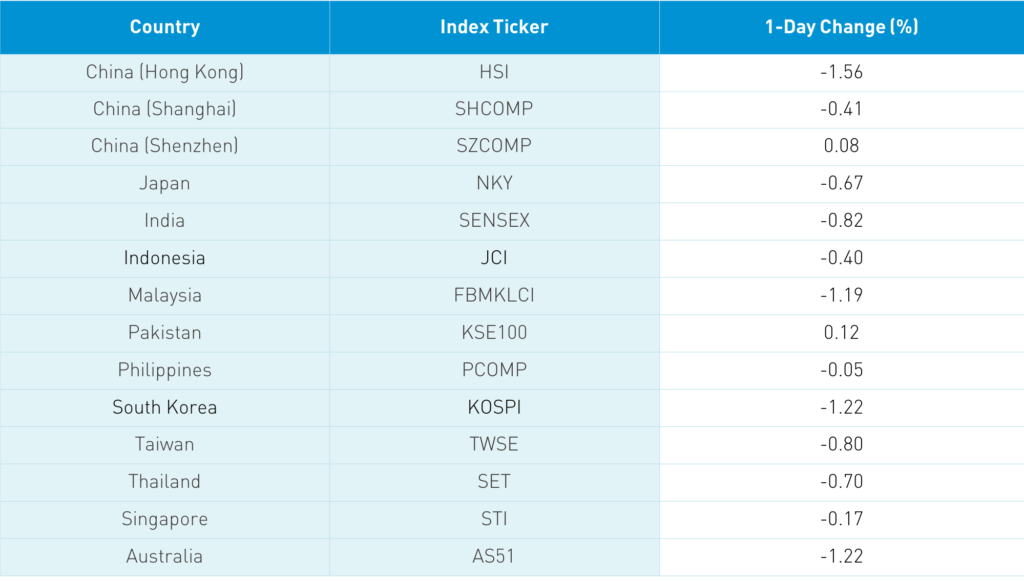

Asian equities echoed the sentiment of US investors by giving Fed Chair Powell’s press conference a thumbs down as his emphasis on more fiscal stimulus led to a good old fashioned risk-off day. Hong Kong, which again is predominantly foreign investors' definition of China, reflected a risk-off sentiment as market leaders were clipped. Tencent was off -1.4%, despite WeChat not being banned in the US, Alibaba Hong Kong was off -1.9%, Xiaomi was off -6.37%, Meituan Dianping was off -2.98%, while JD.com Hong Kong was off -3.82%, NetEase Hong Kong was down -2.4%, and Yum China gained +0.05%.

It is important to note that today’s downdraft was on below-average volume. Shanghai declined on large caps underperformance -0.41%, while Shenzhen gained +0.08% as mid and small caps outperformed. Discretionary stocks were lead by automaker BYD, which was up +10% as mainland auto sales are picking up. Tech held up well as tech war saber-rattling is apt to lead to increased emphasis on homegrown talent. DnD stocks (drugs i.e. pharma and drinks i.e. alcohol stocks), which were recent winners, were off today.

China’s Golden Week holiday begins Thursday, October 1st running until Friday, October 9th.

Last week, I mentioned that HSBC lowered their target for the offshore RMB (CNH), China’s currency that trades during US market hours, to 6.75. It didn’t take long for the target to be breached as CNH closed at 6.74 to the dollar on Wednesday, though backed up overnight to 6.76. The Fed states that rates will stay near zero until 2023, though I believe that CNH over USD could go lower as long as the global economy rebounds in the months and quarters to come.

China’s holdings in US Treasuries declined according to broker chatter. However, I don’t believe China is alone in selling US Treasuries, considering the state of US monetary policy. Increased budget deficits in the US has led the Fed to tolerate higher inflation and become a sizeable buyer of US bonds.

In an ancillary confirmation of investors’ home biases, MSCI updated the amount of active and passive assets benchmarked to their indexes at the end of 2019. Emerging markets benchmarked assets are now $1.3 trillion, which is down from $2 trillion several years ago. That is a very large drawdown! Makes you think, right?

H-Share Update

The Hang Seng was off -1.56%/-384 index points to 24,340 as volume increased +14% from yesterday, though still just above the 1-year average. Breadth was off with 7 advancers and 40 decliners as the broad Hang Composite was off -1.36%, with 128 advancers and 316 decliners. The 204 Chinese companies listed within the MSCI China All Shares Index were off -1.17%, with energy and utilities up +1.22% and +1.07% respectively, while health care was off -2.4%, tech -2.21%, and discretionary -1.58%. Southbound Connect volumes were light as mainland investors purchased $213mm, while Southbound Connect trading accounted for 9.2% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen diverged -0.41% and +0.08% to close at 3,270 and 2,186 respectively as volume increased +8.5% from yesterday, though still below the 1-year average. Breadth was positive with 2,248 advancers and 1,379 decliners as mid and small caps outperformed large caps. The 517 mainland stocks within the MSCI China All Shares Index were all off -0.54%, led by discretionary +1.23%, industrials +0.88%, and tech +0.63% while staples -2.35%, healthcare -1.96%, and communication -1%. Northbound Connect volumes were light as Shanghai had small outflows and Shenzhen had inflows. In total, foreign investors bought $64mm of mainland stocks as Northbound Stock Connect trading accounted for 6.7% of mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 6.79 versus 6.75 yesterday

- CNY/EUR 8.00 versus 8.00 yesterday

- Yield on 1-Day Government Bond 1.06% versus 0.81% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.13% yesterday

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.68% yesterday