Powell’s Punt Leaves Investors Wanting

3 Min. Read Time

Key News

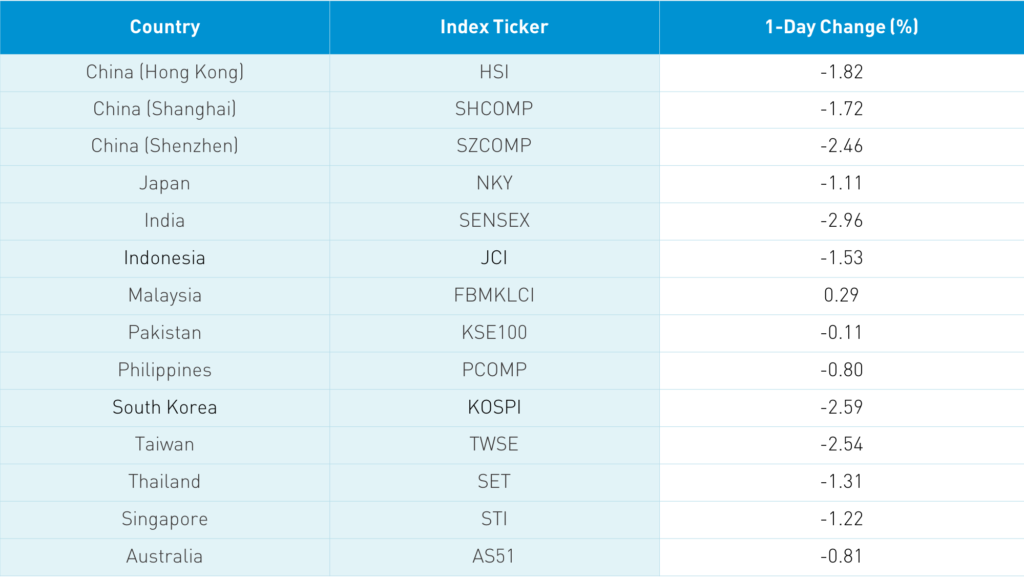

Asian equities followed US equities south with Taiwan, India, and South Korea hit especially hard. Growth outperformers were hit especially hard across the region as investors de-risk by taking profits in their best performers. Chatter was the lack of US fiscal stimulus that could jeopardize the US’ economic rebound, which would have a negative consequence globally.

Fed Chair Powell implied that he's done everything he can in his testimony yesterday, punting to Congress to get a fiscal deal done against the backdrop of bipartisan bickering over the Supreme Court seat, left by the passing of Justice Ginsburg (RIP). The lack of a fiscal plan makes both parties look bad, so hopefully they can get something done soon.

The Hang Seng Index was off nearly 2%, led by Tencent, which was off -1.75%, Meituan Dianping, which was off -4.56%, Alibaba Hong Kong, which was off -2.25%, Xiaomi, which was off -4.84%, Ping An Insurance, which was off -1.29%, and Hong Kong Exchanges, which was off -2.88%. JD.com Hong Kong was off -1.37%, Yum China was off -0.77%, and NetEase Hong Kong was off -1.67%. Breadth was simply awful as the Hang Seng Index had only 6 advancers and 44 decliners, while the broader Hang Seng Composite had just 70 advancers and 399 decliners. One broker noted that growth names might be seeing some profit-taking with the upcoming Ant Group IPO, though candidly, that isn’t likely until late October.

Mainland markets were off on global equity weakness as foreign investors sold Mainland stocks, while small and micro-cap stocks were especially weak as regulators focused on insider trading. Breadth was awful with only 342 advancers and 3,440 decliners. Momma said there would be days like this – one Mainland broker’s market review didn’t have a winners column. We had other chatter, such as TikTok going to court to stop its forced sale and President Xi’s comments on China being carbon neutral by 2060.

We’ve spoken to the quarantine playbook implemented in Asian countries based on their unfortunate experiences dealing with pandemics over the last twenty years. I ran across a piece about two British nationals working in Singapore who were found to have violated their quarantine in June by meeting outside of a restaurant. Initially, they were fined nearly $6,000, but today they had their work visas revoked. Basically, they got kicked out of the country.

Today we find out if FTSE Russell will add Chinese government bonds to the World Government Bond Index (WGBI). A Mainland FI broker estimated that over $100B would flow into Mainland CGBs if approved based on full inclusion.

Trip.com (the old C-trip.com) reports today after the close.

My highlighting of the renminbi’s rise last week has been quickly followed by a dollar rally fueled by global de-risking. If a stimulus deal gets done, I would expect the dollar’s decline to resume.

H-Share Update

The Hang Seng opened lower and stayed there down -1.82%/-431 index points at 23,311 as volume picked up +18.9%, which is back above the 1-year average. Breadth was awful with 6 advancers and 44 decliners. The 204 Chinese companies listed in Hong Kong were off -2.19%. The hardest-hit sectors were discretionary -3.45%, health care -3.43%, tech -3.42%, and materials and energy -2.88%. Ugly day. Southbound Connect volumes were light in mixed trading as Mainland investors sold $17 million of Hong Kong stocks as Southbound Stock Connect trading accounted for 9.2% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen also opened lower and stayed there down -1.72% and -2.46% to close at 3,223 and 2,148 respectively as volume picked up 2.9%, which is below the 1-year average. Breadth was terrible with just 342 advancers and 3,440 decliners. The 517 Mainland stocks within the MSCI China All Shares Index were off -2.4%, led lower by tech -3.2%, materials -3.04%, discretionary -2.91%, utilities -2.82%, and industrials -2.66%. Northbound Stock Connect volumes were light as foreign investors were sellers of Mainland stocks by $1.783 billion as Northbound Stock Connect trading accounted for 6.6% turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.83 versus 6.81 yesterday

- CNY/EUR 7.95 versus 7.95 yesterday

- Yield on 1-Day Government Bond 0.76% versus 0.95% yesterday

- Yield on 10-Year Government Bond 3.08% versus 3.09% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.68% yesterday