Growth Names Gallop Back, Week in Review

4 Min. Read Time

Upcoming Events

Sign up for KraneShares Model Portfolios to view our next webinar: Insights in Action – Asset Class Specialization in Emerging Markets and China is the Key to Differentiated Returns on Tuesday, December 1st, 11:00 am – 12:00 pm EST.

Click here to register!Week in Review

- Over the weekend, the Regional Comprehensive Economic Partnership (RCEP) was signed by ten East Asian countries. The RCEP is the first time China, Japan, and South Korea have ever entered into a free trade agreement and will seek to eliminate tariffs and reduce trade frictions between its members.

- Earnings season for US-listed Chinese companies was in full swing on Monday as search engine Baidu (BIDU US) and online housing platform KE Holdings (BEKE US) reported that their revenues grew by +1% YoY and +71% YoY, respectively, in Q3. iQiyi (IQ US) also reported Q3 revenues, but its report was not as positive. The company's revenues fell -3% YoY.

- Asian equities mostly shrugged off the global value rotation on Wednesday as growth names such as Tencent led gains in Hong Kong.

- Online streamer and entertainment platform Bilibili (BILI US) reported that its Q3 revenues rose +74% YoY to RMB 3.23 billion compared to an estimated RMB 3.06 billion on Wednesday.

Friday's Key News

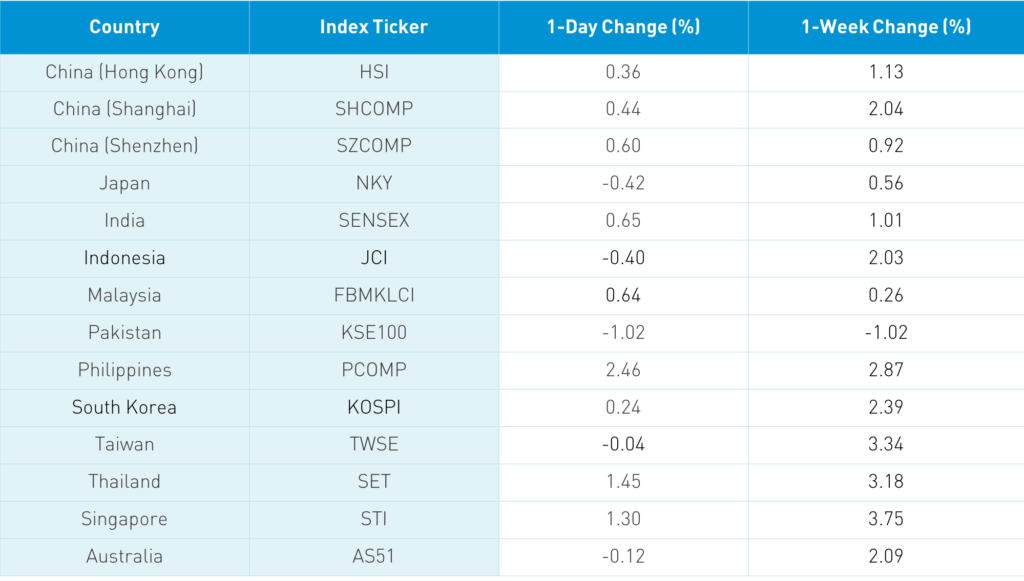

Asian equities ended a positive performance week on a mostly positive note. However, Japan was off a touch in advance of their market holiday Monday and against the backdrop of increased global coronavirus cases. If you closed your eyes and tried to guess the performance of China stocks this week, I doubt your guess would match the weekly returns listed below given the choppiness in US stocks this past week. As investors in public stocks, we are constantly bombarded by headlines and have daily prices available. This is in stark contrast with private equity, in which an investor receives little transparency on the returns and capital is tied up for some time. We need to have discipline as public stock investors to ride out some of the noise.

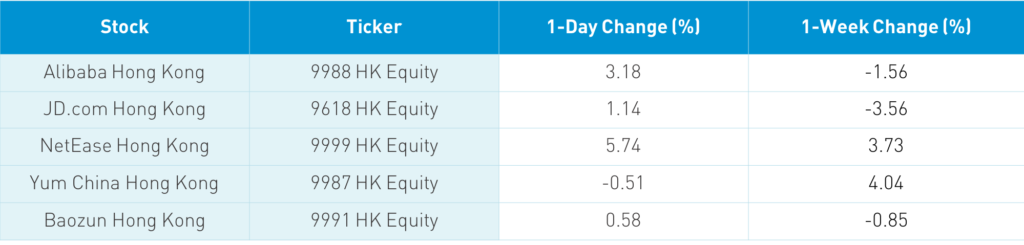

The Hang Seng Index gained +0.36% overnight though the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index (a total China index that includes Hong Kong, Shanghai, Shenzhen, and US stocks) gained +0.93%. Growth names led the market higher as evidenced by Hong Kong volume leader Tencent's +2.62% gain on another large Southbound Connect inflow as Mainland investors were significant buyers of the stock. Meanwhile, Alibaba HK gained +3.18%, Xiaomi gained +1.39%, Meituan gained +3.47% (the company dropped Dianping from its name), BYD gained +5.92% and Ping An fell -0.84%.

Health care rebounded as Hong Kong is seeing a potential 4th coronavirus surge while autos ride the expected tailwind from the 14th Five Year Plan, which is likely to highlight the sector.

Mainland China had a good day as Shanghai and Shenzhen rose +0.44% and +0.6%, respectively. Growth sectors were positive while liquor, health care, and autos outperformed. As China's economy rebounds, it is worth noting that the recovery is broadening, which is leading to a cyclical rebound.

Overnight, the 1 and 5-year Loan Primate Rates (LPR) were left unchanged at 3.85% and 4.65%, respectively. There has been chatter the LPR might be raised soon. China might be the only country in the world that is currently contemplating raising rates.

Financials were weak as recent bond defaults continue to weigh on the sector. However, analysts do not view the recent defaults as major issue given that they represent a small portion of the market. The bond market rallied overnight as the tasty yields in China are too good to pass up on.

CNY appreciated 0.3% versus the US dollar as the exchange rate between the two currencies now sits at 6.56. Foreign investors bought $372 million worth of Mainland stocks via Northbound Connect today, bringing the week's total to $837 million. I suspect these flows may increase as the overhang of US-China political rhetoric improves under a Biden administration, thus removing a key impediment to ownership for many.

Unfortunately, we still have yet to see a challenge to last week's Executive Order. FTSE Russell put out a statement yesterday acknowledging the order and noting that its index methodology suggests removing sanctioned securities from its indices if the directive comes from the US, UK or EU. They are seeking client feedback by next Friday to determine what to do. The actual impact is small though the potential ramifications are wide as the order is effectively a form of capital control. Operationally, it is a disaster due to China Mobile's public listing in the US. I hope someone steps up to challenge it, thereby allowing a court to weigh in.

JOYY (YY US) continued its defense against a short seller's fraud accusation that we detailed yesterday. The company announced it will begin to pay a dividend this morning. Why is this a big deal? It proves that the company has cash. It also inflicts some pain on short sellers, who will owe the dividend by shorting the stock.

H-Share Update

The Hang Seng bounced around the room to close +0.36%/+94 index points at 26,451. Volume rose +0.5% from yesterday, placing it at 110% of the 1-year average while breadth was off with 13 advancers and 36 decliners. The 204 Chinese companies listed in Hong Kong gained +0.93%, led higher by discretionary +2.46%, communication +2.27%, health care +2.03%, staples +1.35%, and materials +1.28%. Meanwhile, utilities -2.08%, real estate -1.7%, financials -1.04% and energy -0.91%. Southbound Connect volumes were light as Mainland investors bought a net $649 million worth of Hong Kong stocks and Southbound trading accounted for 9.4% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened higher and grinded higher to close +0.44% and +0.6% to close at 3,377 and 2,289, respectively. Volume was off -2.76% from yesterday, which is 109% of the 1-year average while breadth was positive with 2,073 advancers and 1,587 decliners. The 518 Mainland stocks within the MSCI China All Shares Index gained +0.8%, led higher by discretionary +2.29%, materials +2.01%, energy +1.89%, industrials +1.62%, and staples +0.95%. Meanwhile, real estate -0.36% and financials -0.23%. Northbound Stock Connect volumes were moderate as foreign investors bought $372 million worth of Mainland stocks and Northbound trading accounted for 5.5% of Mainland turnover.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.56 versus 6.58 yesterday

- CNY/EUR 7.79 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.40% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.31% versus 3.35% yesterday

- Yield on 10-Year China Development Bank Bond 3.77% versus 3.79% yesterday

- China's Copper Price +0.53% overnight