Asian Equities Cheer Vaccine Rollout

3 Min. Read Time

Key News

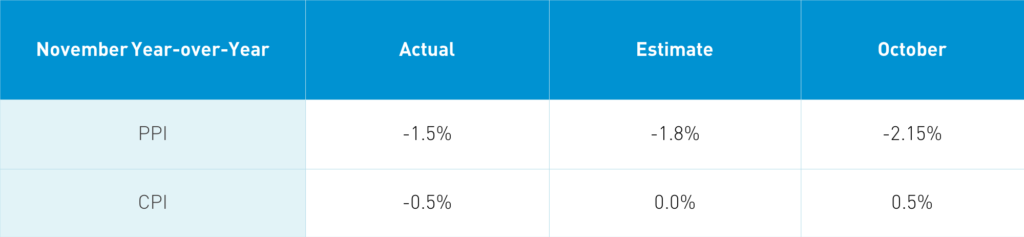

China released November inflation and credit data last night.

Takeaway: The release was cited as a potential headwind for the Mainland market after occurring at the market open. However, Hong Kong did not see it as a market moving event. The African swine flu has officially been put to bed in China as food prices have fallen -2% YoY, dragging the CPI negative for the first time since 2009 as pork fell -12.5% YoY. In general, it is never a good thing to be a pig in China due to the country’s voracious appetite for pork, but 2018/2019 was an especially bad time to be a Chinese pig as an outbreak of African swing flu led to the elimination of over 300 million pigs. The lack of pigs obviously drove up pork, pork substitutes such as beef and mutton, and food prices. China has since built back its pig population and prices for the staple have adjusted. PPI’s negative November was due to a high YoY comparison. It is important to note that the gauge increased month-over-month.

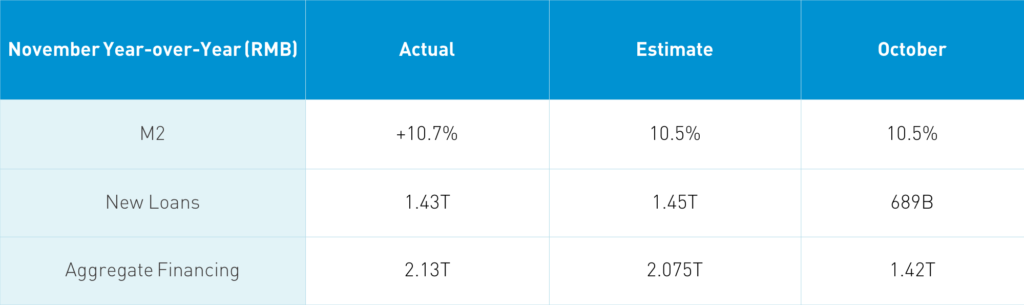

Takeaway: This release occurred after the Mainland market had closed so did not play a factor in today’s market action. November’s credit/loan growth was at/close to economists’ expectations as China’s economy rebounds and policy support provides a tailwind. The consensus is that the rate of credit growth is likely to have peaked. There will still be credit/loan growth but likely not at the same pace as 2020.

Asian equities had a strong day driven by the UK’s vaccine roll out and US’ being not far behind. However, Mainland China missed out on the fun after a selloff into the close. The Hang Seng Index gained +0.75%/198 index points as the 50-stock index was pulled higher by AIA, which gained +2.24%/+58 index points, while the broader Hang Seng Composite Index rose +0.33% and the Hong Kong stocks within the MSCI China All Shares Index rose +0.16%.

After yesterday’s rant on how European and Asian investors are buying Chinese bonds in size while US investors avoid the opportunity completely, Bloomberg rubbed the salt in the wound by reporting yesterday that foreign investors allocated $9 billion to Chinese bonds in November.

An MSCI representative spoke with a Mainland media source on its China A Share inclusion. While reiterating the settlement issue (Chinese stocks settle on trade date versus most markets that trade T+2, i.e. trade date plus two days) and Hong Kong/China holiday alignment, particular emphasis was placed on having MSCI China A Index futures approved in Hong Kong. That could be difficult! Listing MSCI futures on the Mainland would be a smarter strategy I believe. We saw how bond investors were allowed to hedge their currency in the Mainland market. This is because doing so allows for oversight by the Mainland regulator, which is less feasible in Hong Kong. If I were MSCI, I would ask to list in the Mainland over Hong Kong. I still believe we could see China A-Share inclusion start again next year as political rhetoric and the trade war have been impediments.

Hong Kong volume leaders were Xiaomi, which gained +4.36% and Tencent, which gained +0.34% on strong buying from Mainland investors via Southbound Stock Connect, Meituan, which fell -0.42% after being sold via Southbound Stock Connect, property management company China Resource’s IPO, which popped +25%, Alibaba HK, which gained +1.09%, JD.com HK, which fell -1.41%, Pig An Insurance, which gained +1.29%, JD Heath, which gained +2%, energy giant/US-sanctioned company CNOOC, which fell -2.61%, Alibaba Health, which gained +4.6%, and Geely Auto, which gained +2.24%.

The Mainland market was up at the start of the trading day but sold off into the close as agriculture stocks were off on the CPI release. It was an off day. I wish I had a better explanation. Apple’s air pod supplier had a great day as it gained +7.72% but that’s about it. Foreign investors bought the dip via Northbound Connect through the purchase of nearly $600 million worth of Mainland stocks. CNY was flat/off a touch versus the USD.

H-Share Update

The Hang Seng was off its intra-day high gaining +0.75%/+198 index points at 26,502. Volume was up a touch at +0.8% which is still 109% of the 1-year average while breadth was positive with 31 advancers and 21 decliners. The 203 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index +0.16% with tech +1.1%, staples +0.7% and financials +0.63%. Meanwhile, energy -1.15%, health care -0.66% and real estate -0.3%. Southbound Connect trading volume was light as mainland investors bought $56mm of HK stocks today as Southbound trading accounted for 9.5% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen sold off into the close -1.12% and -1.88% at 3,371 and 2,250. Volume increased +12%, which is 94% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares Index fell -1.34% with discretionary -2.55%, communication -1.93%, industrials -1.57%, tech -1.5%, financials -1.32%, health care -1.21% etc. Northbound Stock Connect volumes were moderate/light as foreign investors bought $594mm of mainland stocks as Northbound trading accounted for 6.3% of mainland turnover.