Good Economic News Takes Backseat to Growth Sell-Off

4 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th from 9:00am to 1:00 pm EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

Key News

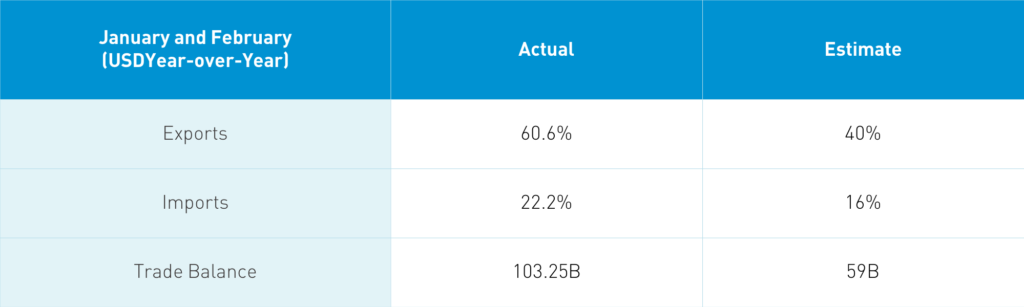

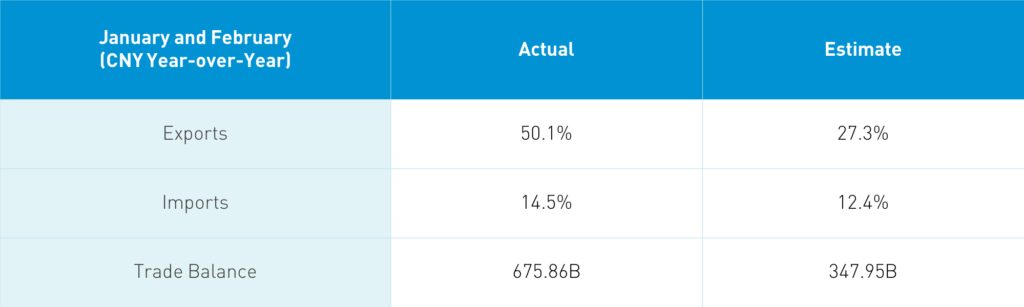

Takeaway: As the middle person in global trade, every investor should watch China for a temperature check on the global economy. The weekend release was a great sign that the global economy is rebounding as China accounts for ~28% of the world’s manufacturing. Yes, the year-over-year comparison was an easy bar to exceed due to China’s quarantine almost exactly one year ago. Imports from the US and India were up 66.4% and 50.1%, respectively, growing faster than the EU’s share, which increased by 32.5%. Exports were up across the board. It was a very strong release not only for China but also for the global economy.

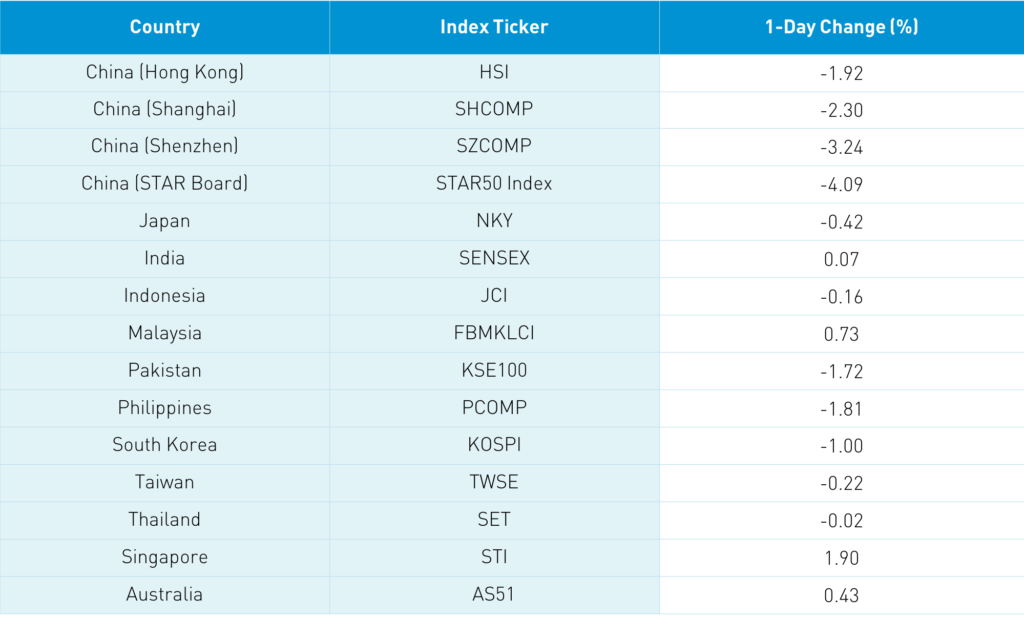

Asian markets initially rose on China’s strong export/import data and the Senate passing the coronavirus stimulus package. However, they turned south as Nasdaq futures fell nearly -2% in Asian trading hours on concerns of rising US Treasury yields. News that Xiaomi will be removed from FTSE indexes due to the Executive Order did not help sentiment as growth stocks were hit hard overnight. Stocks and sectors that outperformed were hit with profit-taking while cyclical/value sectors held up better. The PBOC replaced all maturing short-term debt as short-term repo rates rose slightly. The market appears concerned about tighter monetary conditions.

Meanwhile, the “Two Sessions” policy meetings continue this week. Ironically, policymakers are likely to reiterate China’s needs for the types of stocks that saw selling overnight such as cleantech, electric vehicles, 5G, and semiconductors. The continued recovery in domestic consumption was also noted by investors.

On Thursday, JD.com and Pinduoduo will report their Q4 financial results.

The Hang Seng Index opened higher but quickly turned tail to close-1.92%. Hong Kong volume leaders by value traded included Tencent, which fell -5.28%, Meituan, which fell -8.37%, Xiaomi, which fell -8.59%, HK Exchanges, which fell -5.09%, China Mobile, which fell -1.06%, GCL-Poly energy, which cratered -25.69%, Alibaba HK, which fell -2.82%, Wuxi Biologics, which fell -9.66%, BYD, which fell -10.21%, energy giant CNOOC, which gained +2.04%, Ping An Insurance, which gained +1.29%, China Construction Bank, which gained +1.08%, and ICBC, which gained +1.65%. Southbound Stock Connect had a rare net sell day as Mainland investors sold $1.697 billion worth of Hong Kong stocks. Growth stocks such as Tencent, Meituan, Xiaomi, and HK Exchanges all sold.

Shanghai, Shenzhen, and STAR Board also opened higher before descending hard -2.3%, -3.24% and -3.24%, respectively, in a similar trend of growth/outperformers/favored stocks and sectors sold in favor of cyclical/value plays. Nuclear energy plays were up on chatter of increased usage to bring down coal’s weight in energy generation. Mainland volume leaders by value traded were a who’s who of previous winners as Kweichow Moutai, which fell -4.86%, LONGi Green Energy, which dropped -10%, BYD, which dropped -10%, liquor stock Wuliangye Yibin, which dropped -8.26%, Ping An, which gained +0.53%, broker East Money, which fell -6.13%, Tongwei, which fell -9.29%, BOE Tech, which gained +0.64%, Baotuo Steel, which fell -6.73%, and EV battery maker CATL, which fell -4.69%. Foreign investors sold $1.316 billion worth of Mainland stocks today. CNY fell slightly as the US dollar strengthened overnight, bonds were flat, and copper rallied.

The weekend is a great opportunity to catch up on research pieces. I started Saturday morning with Barron’s, which had a China article amounting to a long list of risks. All risk but no examination of the potential reward or the strong performance in 2020. I then read a piece from a research firm on Warren Buffet’s annual letter. Did anyone notice in Warren’s top ten list a little company called BYD? His investment of $232 million in 2009 is now worth $5,897B! Not bad! To earn that return took some patience of over a decade but also resiliency as the stock gave back nearly all its gains at one point. As long-term investors, we need to exhibit Mr. Buffet’s resiliency and patience, especially in light of current market action.

I do not use Twitter though on Friday I retweeted the stat that 3X times the number of packages were delivered in 2020 versus five years ago. Overnight, it was reported that February package deliveries were up 73% year over year to 4.8B packages in the month. Obviously, courier companies are beneficiaries though it begs the question: who is generating those packages? I’d take a guess: e-commerce companies! Again, I do not tweet often, though if you are interested my Twitter handle is @ahern_brendan. As a firm, we also have @chinalastnight and @kraneshares.

H-Share Update

The Hang Seng opened higher but quickly turned south to close -1.92% at 28,540. Volume increased +15% from Friday, which is 183% of the 1-year average while breadth was mediocre with 27 advancers and 25 decliners. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -4.06% with energy +1.43%, utilities +0.51% and financials +0.36% while discretionary -7.85%, tech -6.75%, healthcare -6.56%, communication -5.37%, staples -3.2%, industrials -3.16%, materials -1.53% and real estate -1.24%. Southbound Connect volumes were moderate as Mainland investors sold $1.697 billion worth of Hong Kong stocks. Southbound Connect trading accounted for 15.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen also opened higher before falling -2.3% and -3.24% to close at 3,421 and 2,224, respectively. Volumes increased +11% from Friday, which is 113% of the 1-year average while breadth had 957 advancers and 2,902 decliners. The 519 Mainland stocks within the MSCI China All Shares Index fell -4.36% with utilities +0.75% while healthcare -6.54%, staples -6.29%, discretionary -5.43%, industrials -5.06%, tech -4.7%, materials -3.15%, communication -2.51%, financials -2.23%, real estate -2.23% and energy -0.6%. Northbound Stock Connect volumes were moderate/high as foreign investors sold $1.316 billion worth of Mainland stocks. Northbound Stock Connect accounted for 7.5% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.52 versus 6.50 yesterday

- CNY/EUR 7.75 versus 7.75 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.36% yesterday

- Yield on 10-Year Government Bond 3.24% versus 3.25% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.69% yesterday

- China's Copper Price +1.50% overnight