Tencent’s $77,000 Fine Leads to $41 Billion Loss in Market Cap (Not a Typo), Week in Review

4 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th at 9:00 am EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

Week in Review

- The selloff in growth stocks from last week continued to some extent on Monday, overshadowing a positive economic release In China. China’s exports have grown by over 60% so far in 2021, versus an expected 40%, in a good sign for the global economy.

- February EV sales increased by a whopping 700% year-over-year in February, data released Tuesday shows.

- Wednesday saw the release of more positive China economic data. Meanwhile, news that representatives from the US and China will meet in April and then again to co-chair the G20 climate summit in October improved the outlook for improved relations between the two superpowers in 2021.

- JD.com released stellar Q4 2020 earnings as growth stocks rebounded across Asia on Thursday. The company grew revenues by 31.4% year-over-year, beating analyst estimates.

Friday’s Key News

Tencent’s fine of $77,000 led to a $41 billion loss in market cap as the stock fell -4.41% in Hong Kong. As we have previously stated, the Alibaba and Tencent ecosystems do not play nice in the sandbox after having created barriers for customers and vendors to utilize both. Like Ant Group’s attempt to call itself a fintech to avoid being regulated a bank, Tencent’s fintech arm, which accounted for 26% of Q3 revenue, has done the same. It is feasible that Tencent will spin off the fintech unit as its core gaming business (33% of Q3 revenue), WeChat (social networks were 23% of revenue) and WeChat advertising (17% of Q3 revenue) are key pillars for the company though adhering to the regulator’s new rules makes more sense. While we do not know exactly how this will play out, my expectation is that these anti-competitive practices will end and the fintech units that facilitate consumer loans will face increased regulation.

Like yesterday’s news that Alibaba will pay a fine, the upside is that the company is likely out of the regulatory woods. The market appeared to agree with me as Alibaba’s US-listing went up yesterday. Feels counterintuitive, doesn’t it? Another counter-intuitive sign is that Ant Group’s CEO Simon Hsu will resign as he plays Lee Majors (a reference to the 1980s TV show The Fall Guy, which I loved as a child).

The reality is that these companies are needed by policymakers domestic consumption is critical to China’s economy. Furthermore, the services sector makes up over 50% of GDP. This will be reiterated next week when February retail sales are reported.

Though minor, another potential contributor to Tencent’ fall was today’s Hang Seng Index rebalance. We have pointed out to investors that Tencent proxies such as Naspers and Prosus are used as an attempt by some asset managers to double down on Tencent. Today is a very unfortunate example of why ETF due diligence is important.

Tencent, along with the Japan Post and Walmart, will buy a small piece of Japanese E-Commerce behemoth Rakuten. Tencent saw net buying via Southbound Connect, though by a small amount.

Asian equities were largely higher as Japan and South Korea both outperformed. Meanwhile, Hong Kong and India were both closed for holidays.

There was a great deal of discussion around Baidu’s Hong Kong listing yesterday.

JD.com is apt to see analyst upgrade after yesterday’s strong results.

H-Share Update

AIA contributed more to the Hang Seng Index’s fall today than Tencent as the insurance giant fell -5.33% after announcing that the profitability of new insurance policies sold declined. The Hang Seng Index was off -2.2% as the Tencent news weighed on growth stocks within the communication and discretionary sectors.

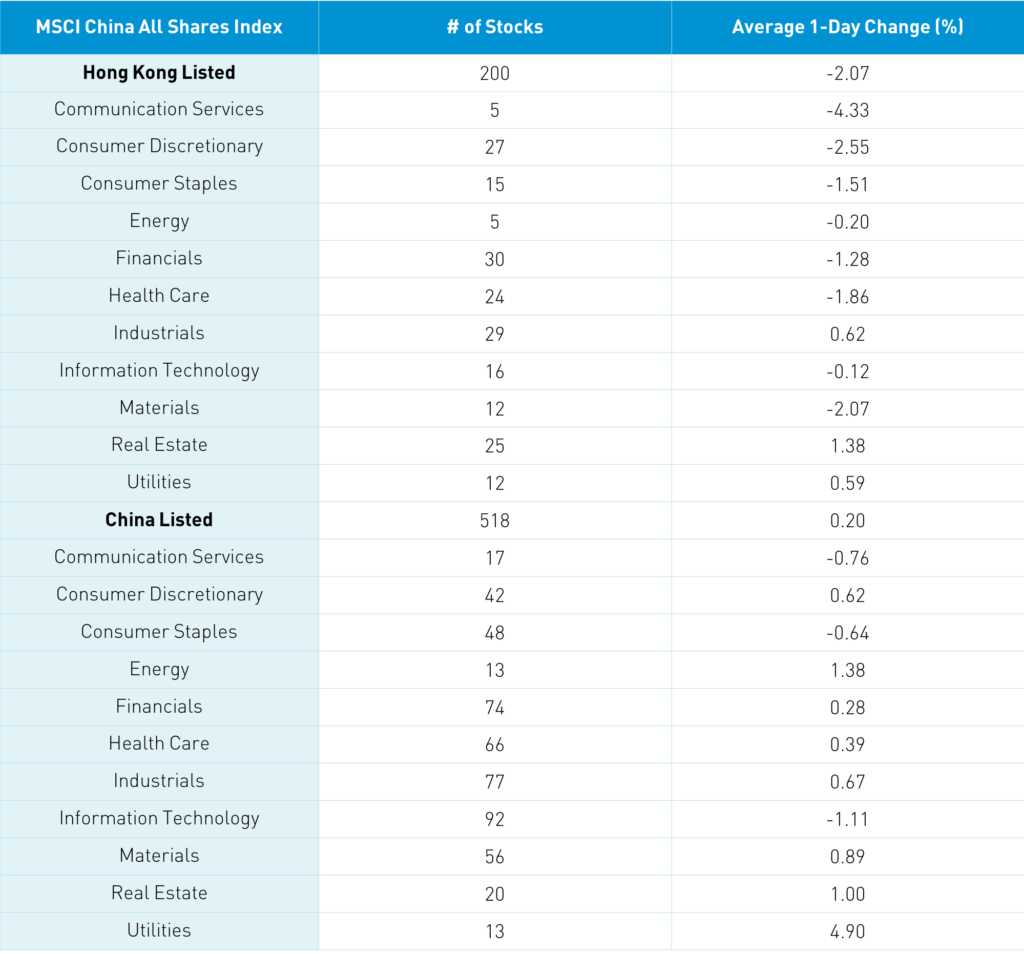

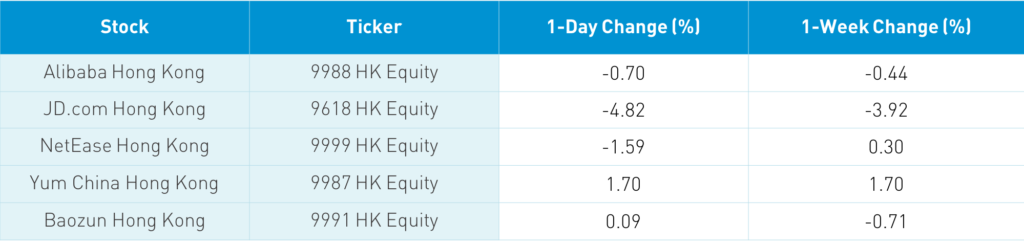

Meanwhile, the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell by -2.07%. Turnover increased by nearly 5% from yesterday to nearly 150% of the 1-year average. The rise in trading volumes overnight was largely driven by the Hang Seng Index rebalance today. Hong Kong volume leaders by value traded were Tencent, which fell -4.41%, Xiaomi, which gained +4.12% after announcing a buyback, Meituan, which fell -3.37%, Alibaba HK, which fell -0.7%, JD.com, which fell -4.82% despite great earnings, Kuaishou Tech, which fell -1.23%, China Mobile, which fell -2.53%, Ping An, which fell -2.02%, AIA, which fell -5.33%, and HK Exchanges, which fell -1.65%. Real estate developer Suanc gained +7.11% after announcing strong earnings and increasing their dividend. This led to a rally in real estate names in one of the sole bright spots today. Southbound Connect volumes were moderate to light as Mainland investors bought $412 million worth of Hong Kong stocks today as Southbound trading accounted for 12.2% of Hong Kong turnover. Xiaomi was a significant buy today.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were mixed gaining +0.47%, +0.17%, and -0.47%, respectively, as Mainland turnover increased +1.78% from yesterday. Mainland volume leaders by value traded were Kweichow Moutai, which fell -1.07%, Longyi Green Energy, which gained +2.35%, liquor name Wuliangye Yibin, which fell -0.22%, CATL, which gained +3.07%, Sungrow Power, which gained +7.09%, TCL Tech, which gained +4.59% after a strong earnings release, BOE Tech, which gained +3.23%, broker East Money, which gained 1.54%, Ping An Insurance, which fell -0.94%, and BYD, which fell -0.71%. Sinolink Securities gained +8.53% on chatter JD.com is buying a stake, though the company denied it. Cleatech had a strong day while semiconductors were off. It was a fairly quiet day in the Mainland candidly as the market stabilizes on reports that mutual funds are pushing for new investors so the firms can put money to work. Northbound Stock Connect volumes were elevated as foreign investors bought $127 million worth of Mainland stocks today as Northbound trading accounted for 7.3% of Mainland turnover. CNY eased a touch versus the dollar, bonds were basically flat, and copper gained +0.95%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.51 versus 6.49 yesterday

- CNY/EUR 7.76 versus 7.75 yesterday

- Yield on 1-Day Government Bond 1.50% 1.50% yesterday

- Yield on 10-Year Government Bond 3.26% versus 3.25% yesterday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.66% yesterday

- China’s Copper Price +0.95% overnight