Growth Stocks Lead Markets Higher Headed into the Weekend

3 Min. Read Time

PMI Release Overview

Takeaway: Yesterday we had the “official” PMIs while today we had Caixin’s survey of purchasing managers, which is done by IHS Markit. The Caixin survey is focused on smaller companies while the “official” survey is focused on predominantly larger companies. The other difference is that the “official” survey includes a few thousand companies while the Caixin survey includes five hundred companies, which makes the latter more volatile. Manufacturing increased for the 11th month, though the pace of growth slowed from February's. PMIs are a diffusion index with readings above 50 indicating month-over-month growth and below 50 indicating a contraction. Export demand outpaced domestic demand as the global economy comes back online. Similar to our comments yesterday on the rising input and outputs in the “official” PMI, Caixin’s economist noted, “The gauges for input and output prices both rose at a faster pace, indicating added inflationary pressures.” More demand for commodities has led to higher prices. China is famous for exporting deflation but what if it exports inflation? This provides for deep thought that necessitates further thinking and not a short-term concern.

Key News

Asian markets headed into the three-day weekend in good spirits as equity markets rose though on light volumes. Investors cheered the US infrastructure plan, positive semiconductor earnings, and increased production efforts from global goliath Taiwan Semiconductor. Specific to China, we mentioned that China will cut taxes, which should benefit consumers. The long-awaited and speculated upon merger of Sinochem and China National Chemical was made official as SOE reforms from a few years ago might be making a comeback.

Reuters reported on Boeing CEO Dave Calhoun’s speech at the US Chamber of Commerce Aviation Summit. According to the article, 25% of Boeing’s sales are from China today, which has become “the world’s largest domestic travel market.” Mr. Calhoun appeared to be calling on better US-China diplomatic relations as for the company “We cannot afford to be locked out of that market. Our competitor will jump right in.”

The South China Morning Post reported that ByteDance might spin off its China TikTok arm called Douyin in an IPO.

There is talk that the Shanghai Stock Exchanges will merge its small-medium board into its main board.

H-Share Update

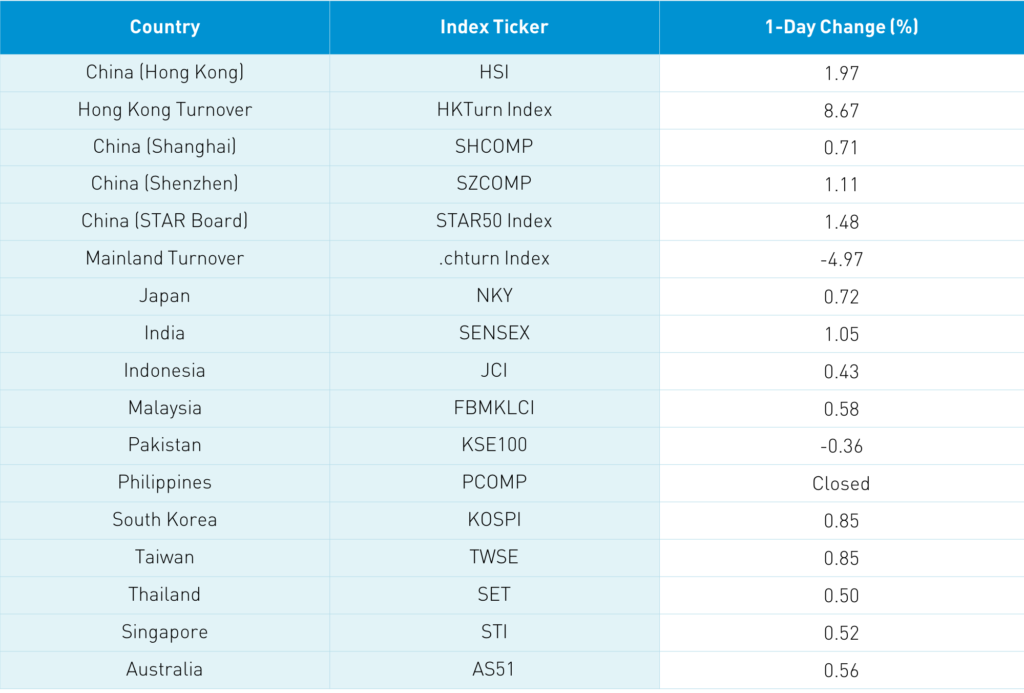

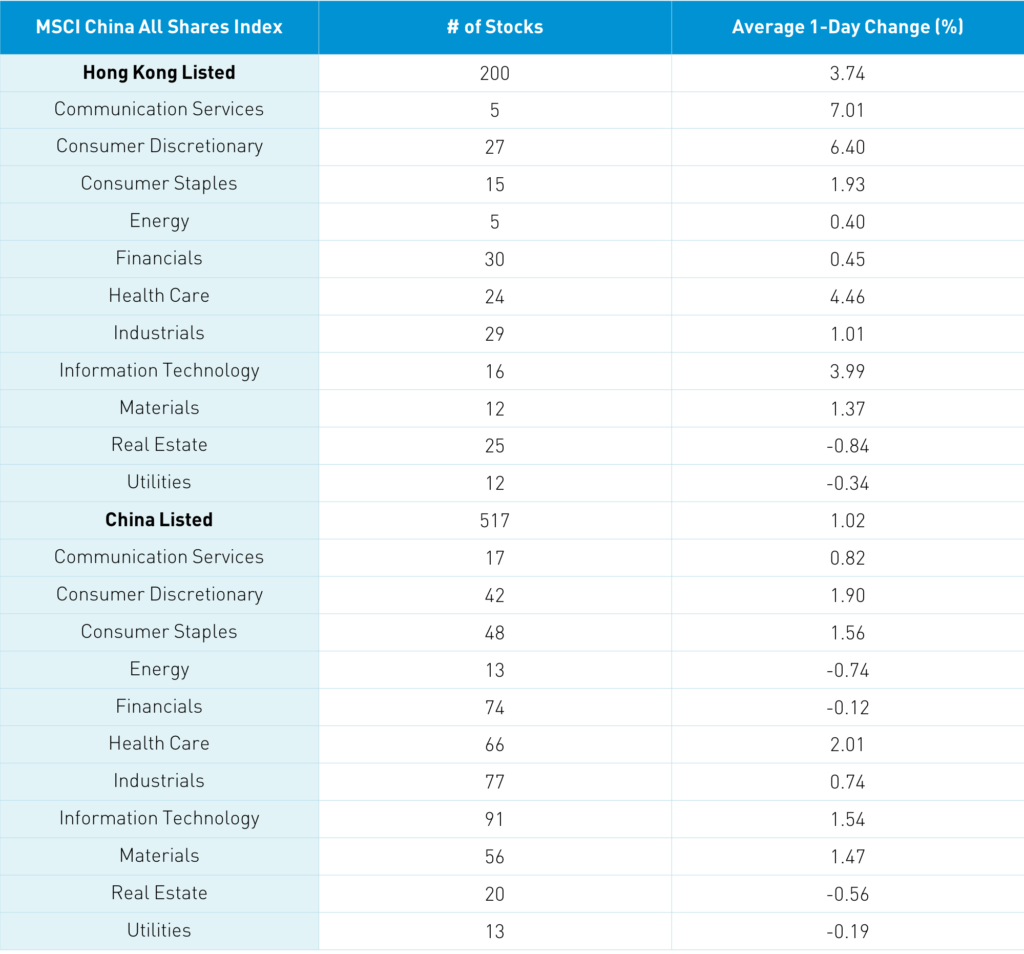

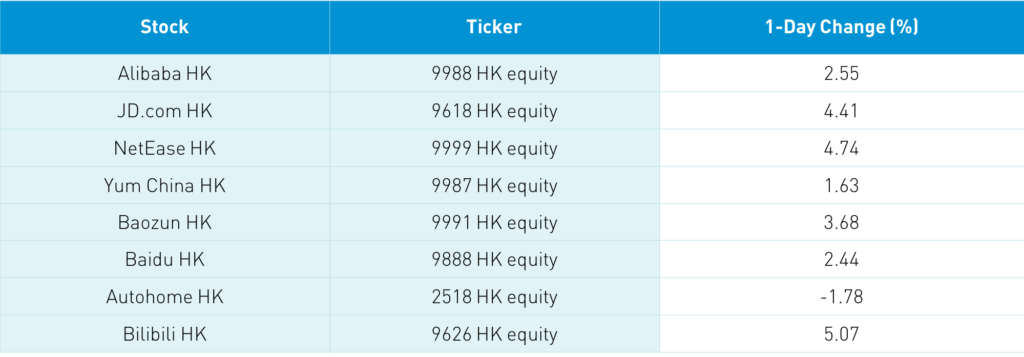

The Hang Seng gained +1.97% while the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +3.74%. Growth sectors and stocks rebounded strongly as communication +7.01%, discretionary +6.4%, healthcare +4.45%, and tech +3.99%, while utilities and real estate posted small losses. Hong Kong volume leaders by value traded were Tencent, which gained +7.21%, Meituan, which gained +9.26%, Xiaomi, which gained +2.72%, Alibaba Hong Kong, which gained +2.55%, Hong Kong Exchanges, which gained +2.45%, BYD, which gained +7.64%, Baidu, which rose +2.44%, AIA, which rose +0.64%, Ping An, which rose +1.24%, and XD Inc, which was up +22% after Alibaba and Bilibili bought into the online gaming company. Volume was up +8% from yesterday though just above the 1-year average. Southbound Connect volumes were light as Mainland investors bought $520 million worth of Hong Kong stocks as Southbound Connect trading accounted for 12.3% of Hong Kong turnover. Tencent saw massive buying while Xiaomi and Meituan had net buying.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +0.71%, +1.11%, and +1.48%, respectively, on a mixed breadth of 1,795 advancers and 2,022 decliners. Volume was off -0.97% from yesterday, which is only 75% of the 1-year average. Contributing to the light volumes was the fact that Northbound Stock Connect was closed today and will remain closed until Wednesday due to Hong Kong’s market holidays on Friday, Monday, and Tuesday. China is open tomorrow though will take a break on Monday. Growth stocks and sectors gained as Mainland volume leaders by value traded were Longi Green Energy, which was up +1.84%, Kweichow Moutai, which rose +1.77%, broker East Money, which rose +3.45%, BYD, which gained +2.77%, and Sungrow Power, which was up +2.77%. The MSCI China All Shares Index's Mainland stocks gained +1.02% led by growth sectors such as healthcare +2.1%, discretionary +2%, staples +1.66%, and tech +1.63%. Meanwhile, energy and real estate posted small losses. Bonds, CNY, and copper were all off a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.57 versus 6.55 yesterday

- CNY/EUR 7.73 versus 7.69 yesterday

- Yield on 1-Day Government Bond 1.65% versus 1.81% yesterday

- Yield on 10-Year Government Bond 3.20% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.58% versus 3.57% yesterday

- China’s Copper Price -1.09%