Bargain Hunters Buy The Dip, Week in Review

5 Min. Read Time

Upcoming Event

Join us on Tuesday, May 25th at 8:20 am for our virtual mid-year conference:

Innovation: The Next Phase of China’s Secular Growth

Featuring the CFO of NIO Steven Feng, CFO of Lufax James Zheng, and Former US Ambassador to China Max Baucus.

Click here to register.

Week in Review

- Commodities, especially metals, began the week sharply higher on Monday, to the benefit of the firms that deal in them. Meanwhile, growth stocks continued declines seen last week in both China and the US.

- China’s April CPI was released Tuesday at -0.3%, assuaging inflation fears somewhat, along with China’s census, which showed that the second most populous nation in the world is not growing its population at nearly as fast a rate as it has historically.

- Xiaomi won its legal challenge against the Department of Defense on Wednesday, successfully disputing its inclusion in an investment ban issued by a Trump administration executive order.

- MSCI announced Wednesday that China’s weight in its widely tracked Emerging Markets Index will rise from 37.7% to 38.4% and the global index provider will now track Alibaba’s Hong Kong listing as opposed to its US listing.

- Alibaba reported strong top-line growth that beat analyst expectations for the first quarter of 2021 and that an impressive 70% of its users now hail from under-developed regions, a major growth area for the company. However, the company reported a loss for the quarter due to the payment of its one-time fine.

Alibaba Earnings Notes

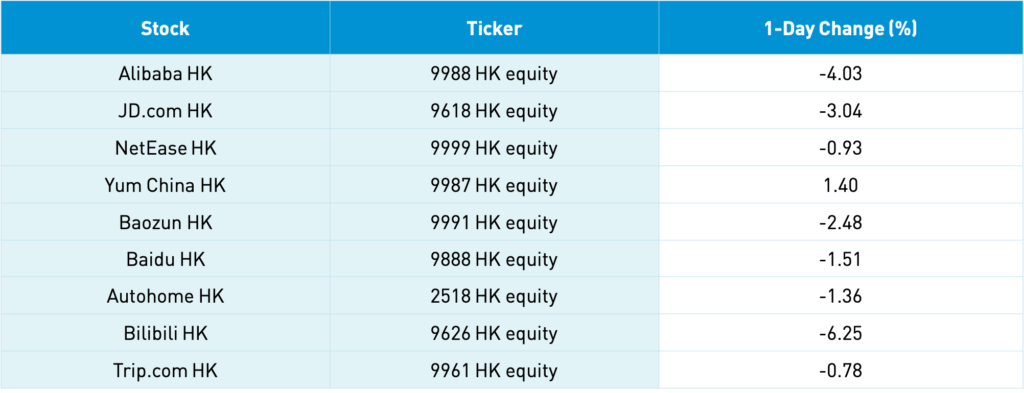

The disconnect between Alibaba’s financial results and the price action yesterday is a head-scratcher. Overnight, Alibaba’s Hong Kong listing was down -4.03% versus the US shares, which cratered -6.28%, after digesting the same financial results for the first quarter. Evidently, Asian investors were less pessimistic than their US counterparts. Over the last year, the company sold $1.2 trillion worth of goods, which would make Alibaba the 17th largest country if you were to substitute GMV for GDP (hat tip to Michael Morris for this comparison). Alibaba sold more than twice as many goods as Amazon over the past year!

The weakness appears to be centered around regulatory concerns in China even though the company has already paid the fine. Jack Ma was recently spotted at the company’s headquarters, which some are taking as a sign that he is out of the regulatory doghouse.

On the other hand, there is also US regulatory risk as the SEC and PCAOB ascertain how to enforce the Holding Foreign Companies Accountable Act. On this issue, I believe China will acquiescence to the US though the previous administration was unwilling to discuss the issue with their Chinese counterparts. There is simply too much money at stake for both the US and China on this issue.

At year-end, of the $1.381 trillion of MSCI emerging market benchmarked assets, $282 billion was passive and $1.663 was active. I suspect active EM managers have lightened their stakes in Alibaba due to the optics of having to defend the company. It is easier just to kick it to the curb than defend owning it to clients.

We also have the value, cyclical rally at the expense of growth stocks which is a factor. Throw in the US-China political rhetoric, and you are left with a US market that is focused domestically rather than overseas. I am not alone in my opinion as analysts continue to bang the table on Chinese internet stocks as the fundamentals are disconnected from the price action.

There has been a lack of media coverage of MSCI’s decision to migrate to Alibaba’s Hong Kong share class over the US share class, which FTSE Russell indexes already have done. Why is this important? Stock Connect. Once Alibaba’s Hong Kong share class is more than 55% of the US share class in terms of volumes, it will be added to Southbound Stock Connect, thereby allowing Mainland investors to buy its shares in Hong Kong.

Alibaba, along with the China internet space generally, has had everything but the kitchen sink thrown at it. Peak pessimism might be a good entry point.

Friday’s Key News

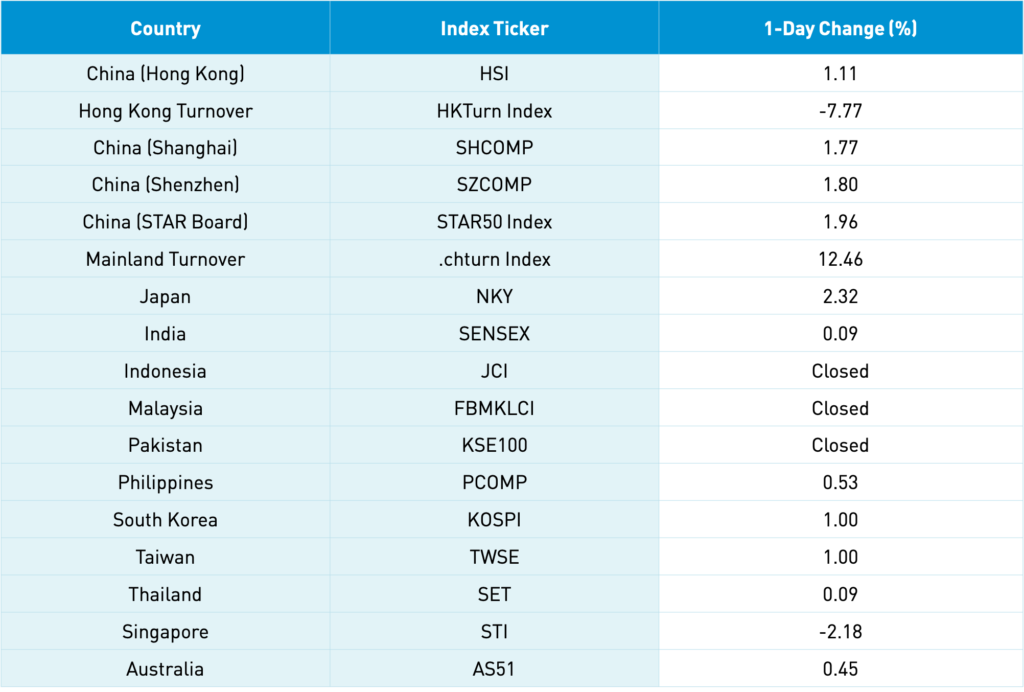

Asian equities ripped higher overnight following the US market’s price action on Thursday as bargain hunters were out in force. However, Singapore was off more than -2% as one of the only markets that were not up, likely due to new virus restrictions in the country, which has been hailed as one of the best managers of the pandemic. Meanwhile, Pakistan, Indonesia, and Malaysia were closed. Candidly, it was a very quiet news day.

US-listed Chinese education names were off yesterday on a Reuters article noting further limitations on tutoring hours. The root of the issue is China’s rigorous school testing. Thus, no matter what regulations say, it is not going to change the behavior of Chinese parents as they try to give their kids a better life.

Metals and mining names were off as policymakers in China look to rein in high commodity prices. The strong move in Mainland Chinese equities was accompanied by an above-average volume boost.

It was reported that April Foreign Direct Investment increased +38.6% year-over-year, bringing the year-to-date versus year-over-year comparison to +31.5%. Once again, there were zero headlines on this data release as it does not fit the narrative.

H-Share Update

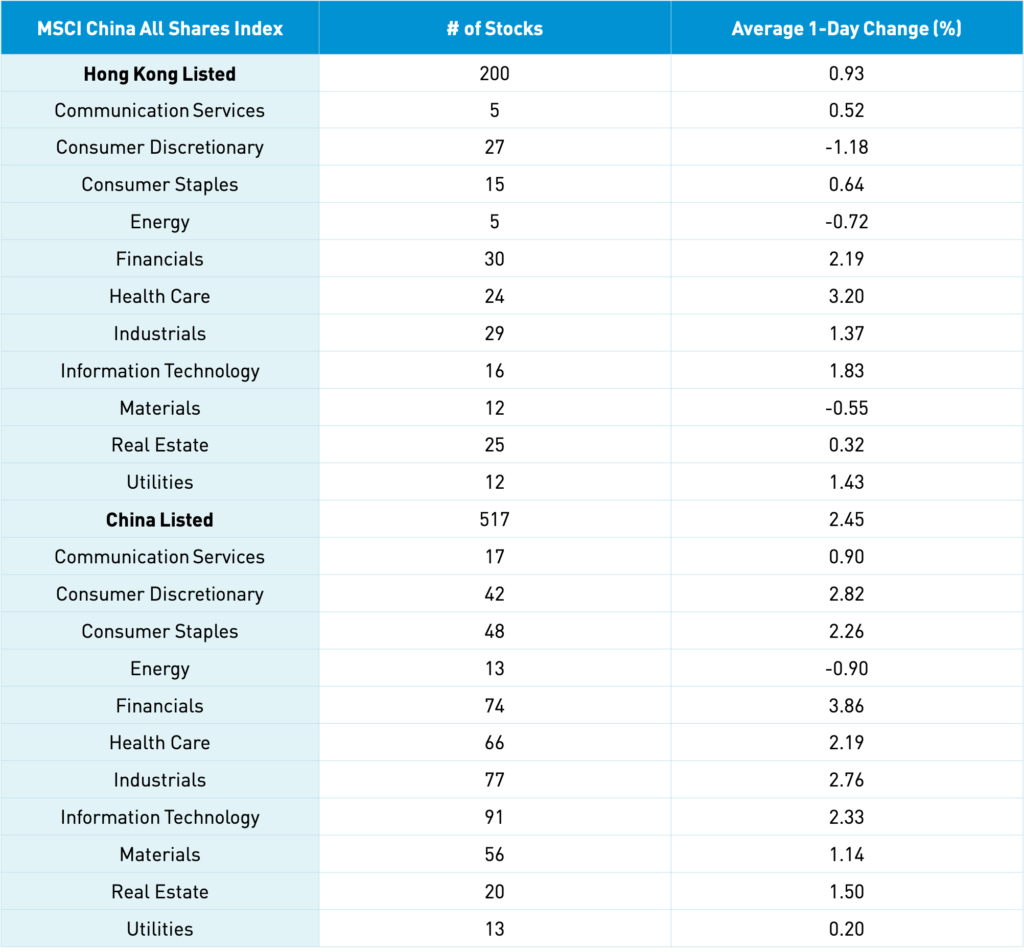

The Hang Seng dipped briefly into negative territory before grinding higher to back above the 28k level at 28,027 following today’s +1.11% move. Volumes were off -7.74% from yesterday, which is just below the 1-year average. I would like to have seen a big volume up day as a sign of conviction, but that did not happen. However, the market got hit with 2X4 this week off -2.04%. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.94% led by healthcare +3.2%, financials +2.19%, tech +1.84%, utilities +1.43% and industrials +1.37%. Discretionary was off -1.17% while energy -0.71% and materials -0.55%. Hong Kong’s most heavily traded stocks by value were Alibaba HK, which fell -4.03%, Tencent, which gained +0.52%, Meituan, which fell -3.02%, Xiaomi, which gained +1.97%, AIA, which gained +6.29% on Q1 new business, Ping An, which gained +2.53%, JD.com, which fell -3.04%, CSPC Pharma, which gained +10.44%, SMIC, which fell -0.21%, and Mengniu Dairy, which fell -0.93%. Southbound Stock Connect volumes were light as Mainland investors bought $604 million worth of Hong Kong shares as Southbound trading accounted for 11.3% of Hong Kong turnover. Tencent, Meituan, and Xiaomi led net inflows.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +1.77%, +1.8%, and +1.96%, respectively, as volume expanded +12.46% from yesterday, which is just above the 1-year average. There were 2,928 advancing stocks and 936 declining stocks today. The 517 Mainland stocks within the MSCI China All Shares Index gained +2.46% led by financials +3.86%, discretionary +2.83%, industrials +2.76%, tech +2.33%, staples +2.27%, healthcare +2.2% and real estate +1.51% while energy was off -0.9%. Software and insurance sub-sectors outperformed today while coal, industrials metals and iron ore were off. The Mainland’s most heavily traded stocks by value were broker East Money, which gained +12.79%, Fosun Pharma, which gained +5.7%, CITIC Securities, which gained +7.66%, Changan Auto, which gained +9.99%, Kweichow Moutai, which gained +1.95%, Walvax Biotech, which gained +6.83%, CATL, which gained +2.25%, liquor stock Wuliangye Yibin, which gained +3.99%, Sany Heavy Industry, which gained +5.17%, and Ping An, which gained +2.95%. Northbound Stock Connect volumes were moderate as foreign investors bought $1.4 billion worth of Mainland stocks today as Northbound trading accounted for 6.4% of Mainland turnover. Wuliangye Yibin and East Money saw large net buying. CNY appreciated versus the US dollar to 6.44, bonds were flat, and copper was off -1.6%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.44 versus 6.45 yesterday

- CNY/EUR 7.81 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.56% versus 1.53% yesterday

- Yield on 10-Year Government Bond 3.14% versus 3.14% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price -1.60%