Apple Electric Vehicle Rumors Drive China Battery Makers Higher

3 Min. Read Time

Upcoming Webinar:

Join us on Thursday, June 10th at 11:00 am EDT for:

Hope For The Best, Plan For The Worst

Click here to register.

Key News

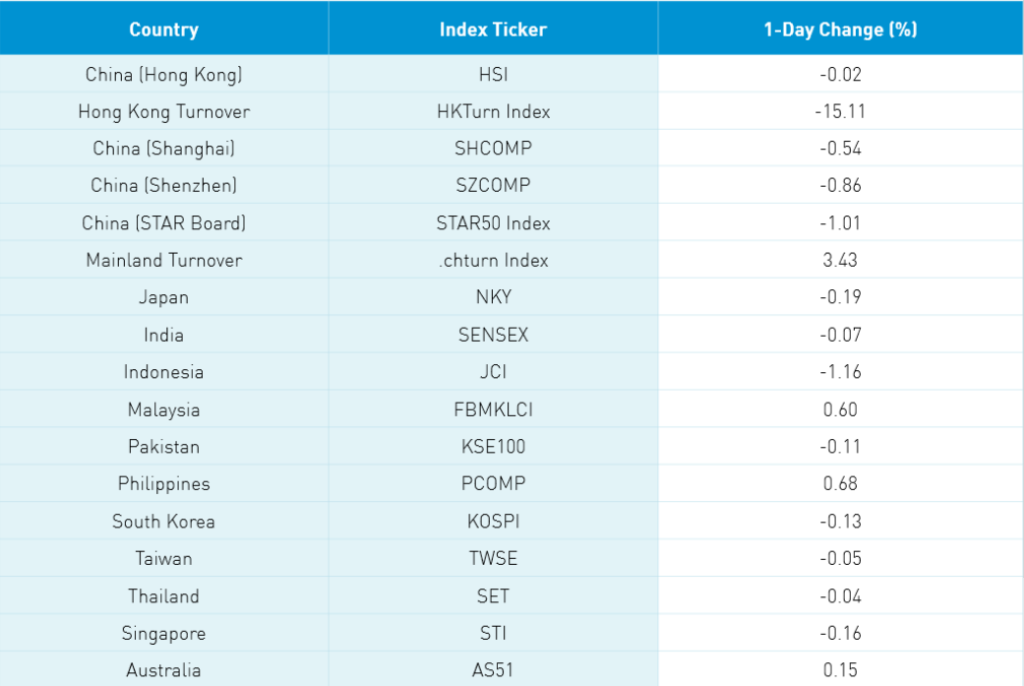

Asian equities were mostly lower on light volumes ahead of Thursday’s US economic data release and following yesterday’s mixed US equity session. Meanwhile, US-China political rhetoric continues to weigh on sentiment.

The China and Hong Kong-listed electric vehicle (EV) space had a strong day led by electric bus maker BYD and battery maker CATL. Reuters reported that Apple will hire both companies to supply batteries for its EV efforts. Reuters also reported strong Chinese EV sales in May by Tesla, BYD, and Geely. Lithium stocks were universally off on the news as Apple’s EV might use a lower lithium input battery. There has been a great deal of speculation on this report though minimal confirmation from the companies.

Mainland liquor company Kweichow Moutai and its rival Wuliangbye Yibin were off as Bloomberg reported that local governments may tax the fiery liquor. Mainland media did not mention the tax, but rather simple profit taking as the liquor and spirits sector has performed very well with a year-to-date return of nearly +18% even after today’s loss of -8.55% as 2nd and 3rd tier names were off significantly. Kweichow and Wuliangbye are very widely held both domestically and internationally, so we will see whether the dip will be bought. Today, Kweichow was a net buy in Connect trading while Wuliangbye was a net sell.

There was some chatter about the PBOC injecting liquidity into the financial system in advance of tax payments, which are due in a week. The PBOC is not going to flood the market with liquidity in advance. Rather, they will inject liquidity as they see fit following careful consideration of all factors.

Real estate giant Evergrande announced a share buyback, which led to a rebound in real estate, giving today a slight feel of value over growth though it was a decidedly quiet night.

Education stocks were lower again on concerns surrounding new afterschool tutoring rules as a global investment bank downgraded TAL Education and New Orient, which lead to further weakness overnight. Mainland investors were sellers of Hong Kong stocks for the third day in a row. Tencent and Meituan were sold somewhat. Foreign investors were net buyers of Shenzhen stocks and sellers of Shanghai stocks.

H-Share Update

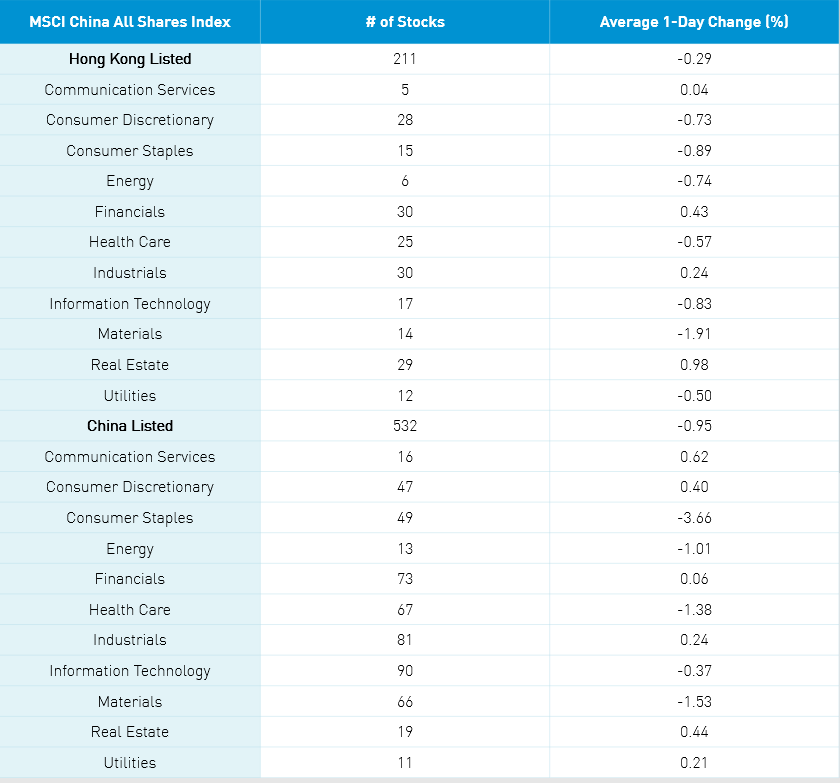

The Hang Seng opened higher but faded to close -0.02% at 28,781 as volume fell -15% from yesterday, which is only 75% of the 1-year average. The 211 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index eased -0.29% with real estate +0.98%, financials +0.43%, industrials +0.25%. Meanwhile, materials -1.91%, staples -0.89%, tech -0.83%, energy -0.74%, discretionary -0.57% and utilities -0.5%. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.08%, Meituan, which fell -1%, BYD, which gained +6.27%, Xiaomi, which was flat, Alibaba HK, which fell -0.86, AIA, which fell -0.36%, Geely Auto, which gained +1.42%, Ping An Insurance, which fell -0.18%, COSCO Shipping, which gained +2.16%, and Sunny Optical, which fell -3.8%. Southbound Stock Connect flows were moderate as Mainland investors sold $227 million worth of Hong Kong stocks as Southbound Connect trading accounted for 13.9% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board also opened higher but faded to close -0.54%, -0.86%, and -1.01%, respectively, on volumes that were +3% higher than yesterday, which is 107% of the 1-year average. There were 1,695 advancing stocks and 2,178 declining stocks. The 531 Mainland stocks within the MSCI China All Shares Index lost -0.98% as communication +0.59%, real estate +0.42%, discretionary +0.38% and industrials +0.21%. Meanwhile, staples -3.68%, materials -1.56%, healthcare -1.41%, and energy -1.04%. The most heavily traded Mainland stocks by value were BYD, which gained +6.55%, Kweichow Moutai, which fell -3.52%, Wuliangye Yibin, which fell -4.78%, CATL, which gained +0.51%, East Money, which fell -1.06%, Luzhou Laojiao co., which fell -7.49%, Jiangsu Hoperun Software, which gained +10.79%, Ganfeng Lithium, which fell -5.78%, Luxshare, which gained +2.11%, and Tianqi Lithium, which fell -6.63%. Northbound Stock Connect flows were moderate as foreign investors bought $47 million worth of Mainland stocks as Northbound Stock Connect trading accounted for 6% of Mainland turnover. CNY was off a touch, bonds were flat, and copper was off -0.4%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.40 yesterday

- CNY/EUR 7.79 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.68% versus 1.72% yesterday

- Yield on 10-Year Government Bond 3.11% versus 3.11% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.54% yesterday

- Copper Price -0.4% overnight