Didi’s Future of Electric Vehicles

3 Min. Read Time

Key News

North Asia was off while South Asia posted gains in a quiet night marked by light volumes and little news flow other than increasing concerns of the Delta variant. Hong Kong and China were hit with profit-taking, though solar and EV plays outperformed. Internet plays were largely off on profit-taking, though JD.com Hong Kong and NetEase bucked the trend, gaining +0.6% and +3.65% respectively.

Didi’s NYSE listing tomorrow is apt at the top of the range at $14/share. There is speculation that the listing will be heavily subscribed as the IPO priced is determined tonight. Yes, Didi is like Uber as a taxi cab/car-hailing service, though I firmly believe this misses the future that Didi envisions. Owning a car in China can be expensive, and the terrible traffic in China limits the number of people who can get a license plate. Once you have a car you need to park it, which can also be problematic. China’s vast high-speed rail network makes long car trips unnecessary. Didi plans to convert its fleet to EV over the next few years. In the long run, it envisions a fleet of EV autonomous cars driving into cities from garages outside of the city each morning and returning that same night. The company has grown revenue by nearly 100% each of the last three years. Finding a company at this size growing that quickly is hard, which is why investors are clamoring for shares.

I am still making my way through a research piece from a Mainland institutional broker recommending investors buy Chinese growth stocks due to compelling valuations. I find this interesting as the commentary from a top active China manager had a similar view using the latest correction to increase their growth stock positions. The market does what is least expected to do, just as when investors load up on commodity/value/cyclical plays at the expense of growth stocks, guess what outperforms? If rates stay lower for longer, growth stocks have an advantage though China's growth stocks have corrected significantly.

Foreign investors sold Mainland stocks yesterday and today, though Northbound Connect is closed tomorrow and Thursday for Hong Kong’s holiday. Year-to-date foreign investors have bought $34.325B of Mainland stocks, bringing the total to $65.33B since 12/31/2019. Tencent has been sold the last two days in Southbound Connect, bringing the percentage of market cap held by Mainland investors to 6.68% off of its June high of 6.93%. Mainland investors own twice as many Tencent than the #2 most widely held stock, China Construction Bank, and three times as much as Meituan by market cap value. Meituan’s 6.74% Mainland ownership has been stable. Just an observation that I’ll be watching.

H-Share Update

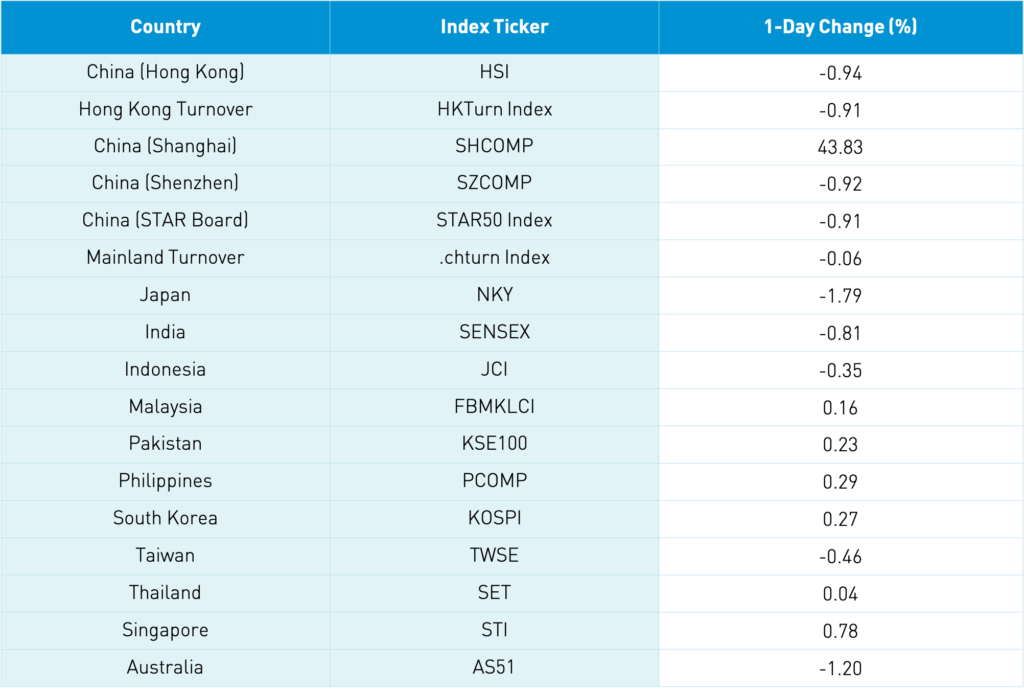

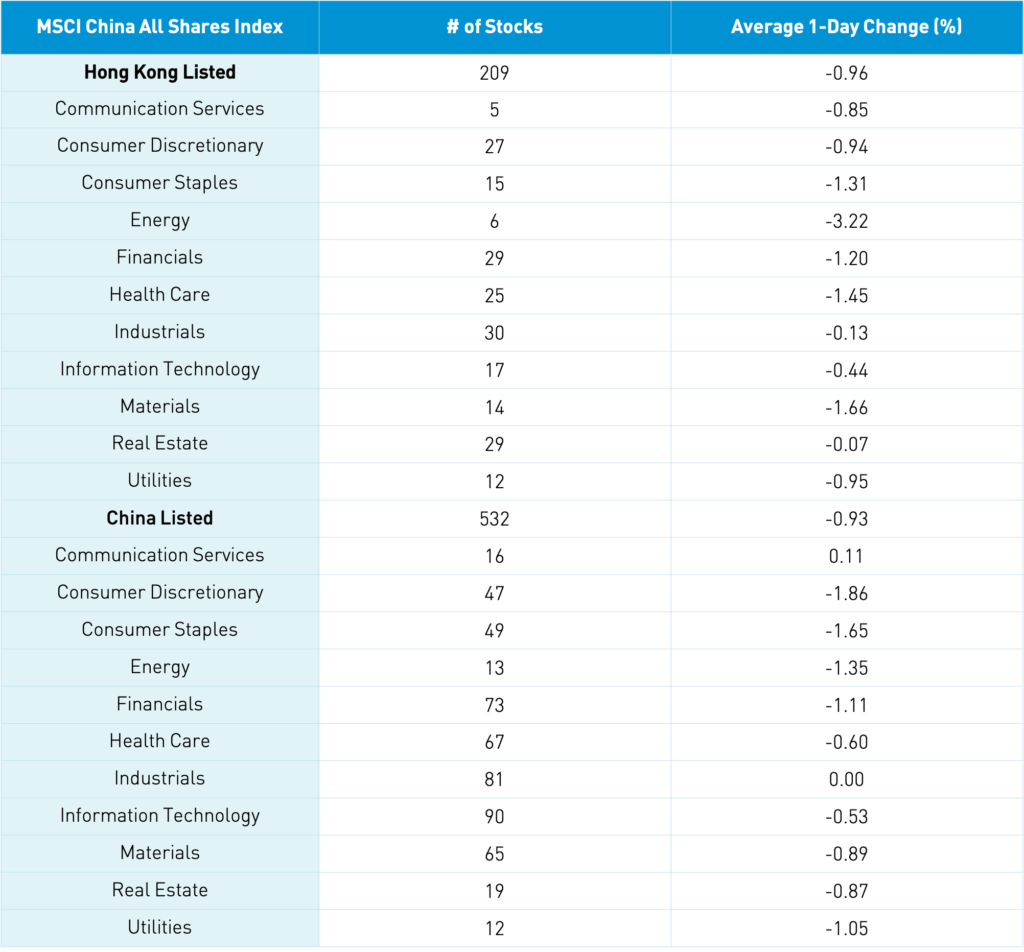

Hang Seng Index and Hang Seng TECH Index were in the green for about 10 seconds at the open before taking the down escalator off -0.94% and -0.91% respectively on volumes +43% higher than yesterday’s half-day session, though only 89% of the 1-year average. The 209 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.96%, led by energy -3.22%, materials -1.66% healthcare -1.45%, staples -1.31%, financials -1.2%, and utilities -0.95%. Hong Kong’s most heavily traded by value were Tencent, which fell -0.84%, Meituan, which fell -1.46%, Alibaba HK, which fell -1.17%, Ping An, which fell -1.61%, Xiaomi, which fell -0.9%, BYD, which rose +0.77%, Geely Auto, which fell -0.78%, JD.com HK, which rose +0.6%, Li Ning, which rose +1.44%, and China Construction Bank, which fell -0.81%. Southbound Stock Connect volumes were moderate/high as Mainland investors sold -$128mm of Hong Kong stocks as Southbound trading accounted for 13.6% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board also declined in the morning session before bottoming -0.92%, -0.91%, and -0.06% respectively on volume -1.79% from yesterday, which is still 106% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index fell -0.95%, led by discretionary -1.88%, staples -1.67%, energy -1.37%, financials -1.13%, utilities -1.07%, and materials -0.9%, with only communication in the green +0.09%. The Mainland’s most heavily traded were Three Gorges Renewables, which rose +5.2%, Longi Green Energy, which rose +3.62%, battery giant CATL, which rose +2.96%, BYD, which fell -0.13%, broker East Money, which fell -3.14%, Jiangsu Hoperun Software, which fell -7.23%, COSCO Shipping, which fell -1.46%, Kweichow Moutai, which fell -1.95%, Tongwei, which rose +4.44%, and Chongqing Changan Auto, which fell -3.03%. Northbound Stock Connect volumes were moderate as foreign investors sold -$485mm of mainland stocks as Northbound trading accounted for 5.7% of mainland turnover. Bonds rallied, copper fell, and CNY was flat.