Mainland Moves Higher, Didi Lists on NYSE

3 Min. Read Time

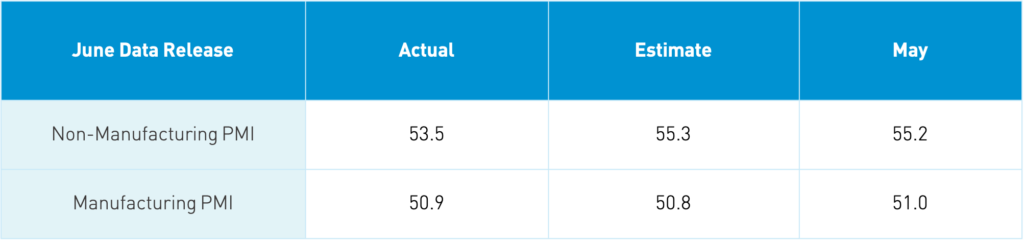

June PMI Data Release

Takeaway: Our Hong Kong institutional brokers did not speak to the PMIs, indicating they weren’t a factor in trading today. The numbers indicate that the policymakers' goal of lowering commodity prices is showing success as input prices grew at a slower pace.

The PBOC is concerned about inflation driven by higher commodity prices. They are trying to get prices down as the global economic reopening is causing demand to outstrip supply. The “official” PMI survey is conducted by the National Bureau of Statistics as opposed to the Caixin PMI survey, which is conducted by IHS Markit. The “official” PMI survey is composed of mostly large companies versus Caixin’s focus on medium and small companies. PMIs are a diffusion index comparing the rate of growth month over month with readings over 50 indicating expansion and readings below 50 indicating a decline. Business expectations are still strong in both while export orders did decline.

Key News

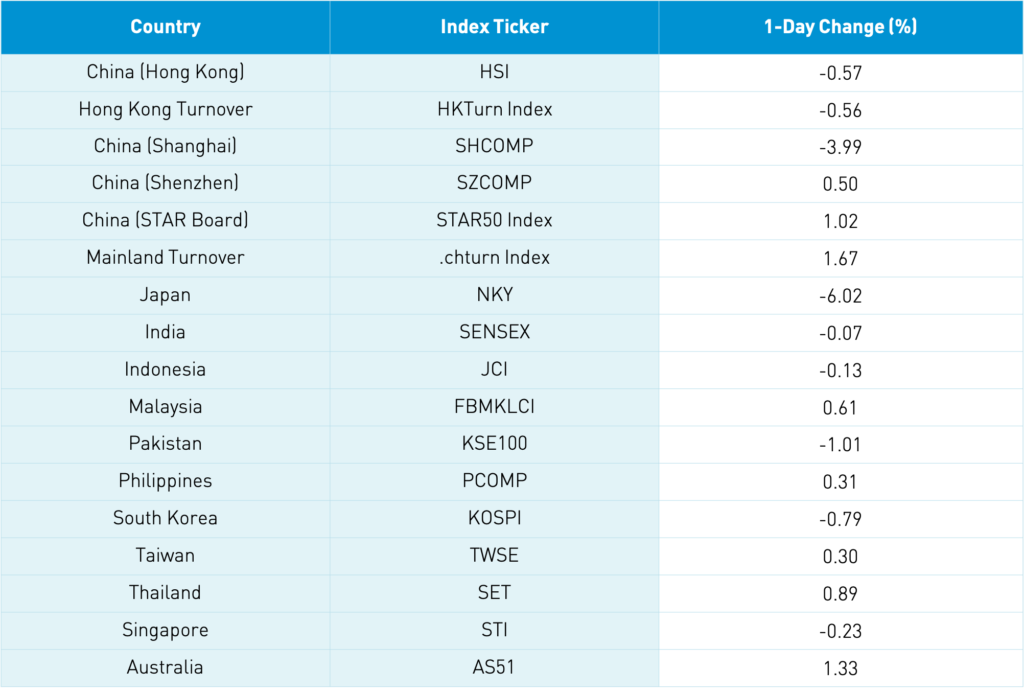

Asian equities ended the month largely higher with Japan and Hong Kong off while Singapore and China outperformed.

It was a quiet night with IPOs garnering attention as tea chain Nayuki Holding’s Hong Kong IPO declined -13.54% while biotech Hutchmed China gained +50.37%. Xpeng’s Hong Kong IPO is also coming and Bloomberg reporting they have already raised $1.8B.

Didi’s NYSE listing today could raise the company as much as $4.4B. The company is selling 317mm shares at $14 a piece, the top of their price range.

Hong Kong had an off day in advance of tomorrow’s holiday as value outperformed growth, though dual-listed Chinese internet stocks including Alibaba, JD.com, NetEase, and Baidu did well while internet stocks solely listed in Hong Kong including Tencent, Meituan, and Kuaishou were off.

Mainland markets did well as growth outperformed value and smaller companies outperformed large companies. The STAR Board returned +1.67% versus Shanghai’s +0.5% gain. The electric vehicles (EV) and semiconductor sectors were top performers on the Mainland today. Healthcare did well on the Mainland as reports of a highly regarded portfolio manager buying Guangyuyuan Chinese Herbal Medicine (600771 CH) sent the stock up +6.86% and lifted the sector. The Shenzhen Composite has almost cleared its February high post-correction though remains 22% away from its all-time high in 2015.

I came across a statistic from Bloomberg New Energy Finance that floored me. The market capitalization of Tesla is greater than that of the six largest global automakers combined. This is despite Tesla selling 500,000 cars in 2020 versus the six automakers selling 50mm cars! I’m a huge fan of Tesla though it will face stiff competition as traditional automakers get into the EV game.

EVs have been luxury cars but that will change dramatically in the years to come. My colleague Anthony found another amazing statistic: there are only 10mm EVs in the world today! Last year, there were 63mm cars sold, showing that there is a significant upside though automakers, miners, charging stations, and auto technology companies are all likely to benefit. EV is so much more than one company.

H-Share Update

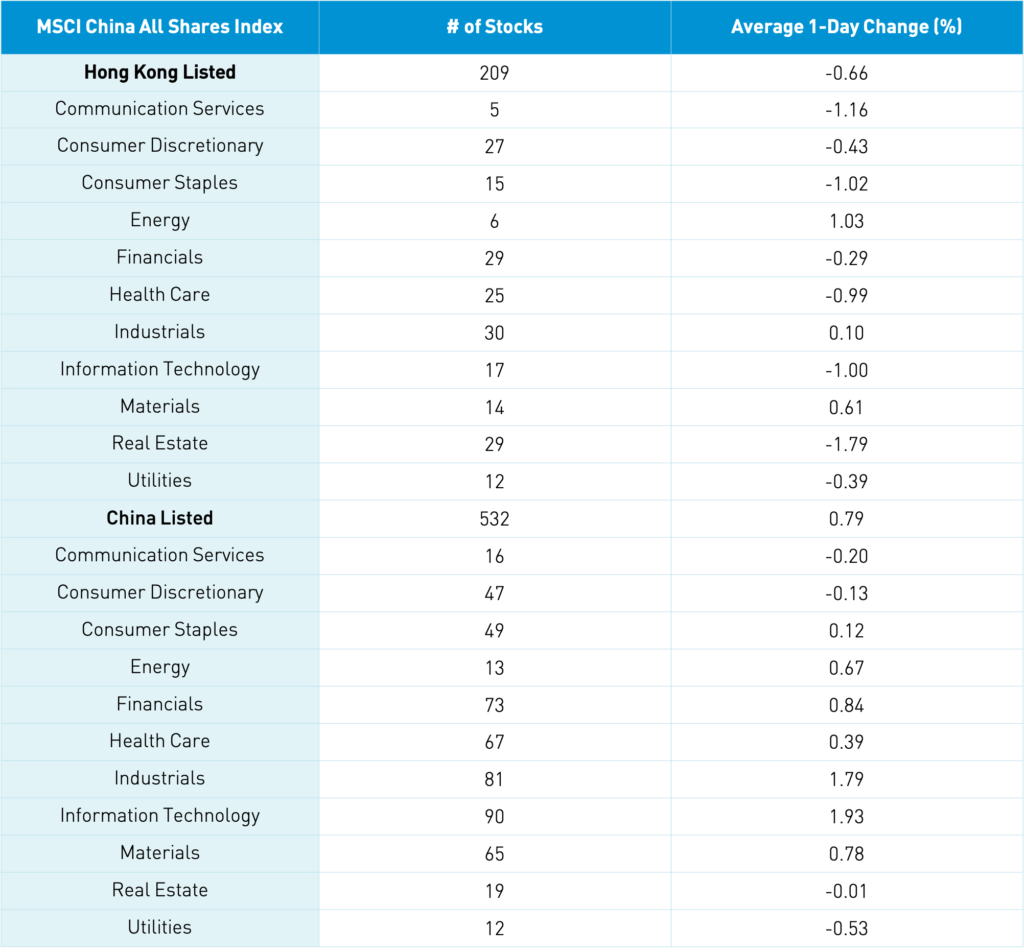

The Hang Seng Index and Hang Seng TECH Index opened higher but like yesterday took the elevator down -0.57% and -0.56% as volume declined -3.99% from yesterday which is just 85% of the 1-year average. The 209 Chinese companies listed in HK within the MSCI China All Shares declined -0.66% led by energy +1.03%, materials +0.61% and industrials +0.09% while real estate -1.79%, communication -1.16%, staples -1.02%, tech -1.% and healthcare -0.99%. HK’s most heavily traded stocks by value were Tencent -1.1%, Meituan -1.05%, Alibaba HK +0.27%, Geely Auto -3.36%, tea restaurant Nayuki Holding’s IPO -13.54%, AIA +0.84%, drugmaker Hutchmed China’s IPO +50.37%, SMIC +2.36%, Xiaomi -1.64% and BYD -1.86%. Southbound Stock Connect volumes were light as mainland investors $69mm of HK stocks as Southbound trading accounted for 12.1% of HK turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board opened higher and kept going gaining +0.5%, +1.02% and +1.67% as turnover declined -6% from yesterday which is 99% of the 1-year average. The 532 mainland stocks within the MSCI China All Shares gained +0.79% led by tech +1.93%, industrials +1.8%, financials +0..84%, materials +0..78%, energy +0.67% and healthcare +0.39% while utilities -0.52% and communication -0.2%. The mainland’s most heavily traded stocks by value were broker East Money +3.28%, COSCO Shipping +4.95%, China Three Gorges Renewables -4.79%, CATL +5.17%, BYD -0.91%, Longi Green Energy +0.05%, Jiangsu Hoperun Software +5.37%, Sany Heavy Industry +4.31%, SMIC 4.34% and metals wholesaler Wuchan Zhongda Group -7.41%. Southbound Stock Connect was closed in advance of tomorrow’s HK holiday. CNY was basically flat, bonds rallied slightly and copper was off -0.01%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.66 versus 7.70 yesterday

- Yield on 1-Day Government Bond 1.95% versus 1.86% yesterday

- Yield on 10-Year Government Bond 3.08% versus 3.09% yesterday

- Yield on 10-Year China Development Bank Bond 3.48% versus 3.49% yesterday