Irrational Pessimism As Trivial Antitrust Fines Announced

3 Min. Read Time

Key News

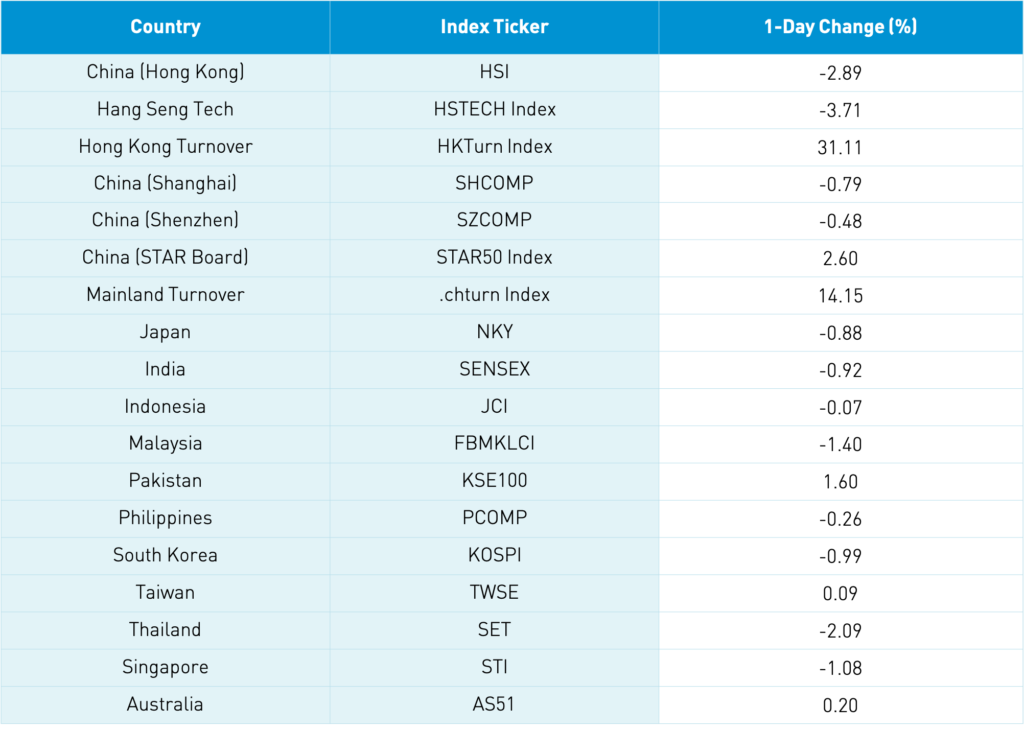

Asian equities followed S&P 500 futures lower overnight as the specter of US tapering weighed on investor sentiment. Mainland Chinese indexes were pulled lower by banks’ underperformance, though tech outperformed, led by semiconductors, electric vehicle ecosystem stocks, and clean technology stocks as the STAR Board gained +2.6%. Yesterday's talk of lowering bank reserve requirement ratios is a positive sign, though might have investors worried about upcoming economic data releases. Mainland bonds’ rallied as the yield on the 10-year China treasury bond fell to 2.98% from yesterday’s 3.06%.

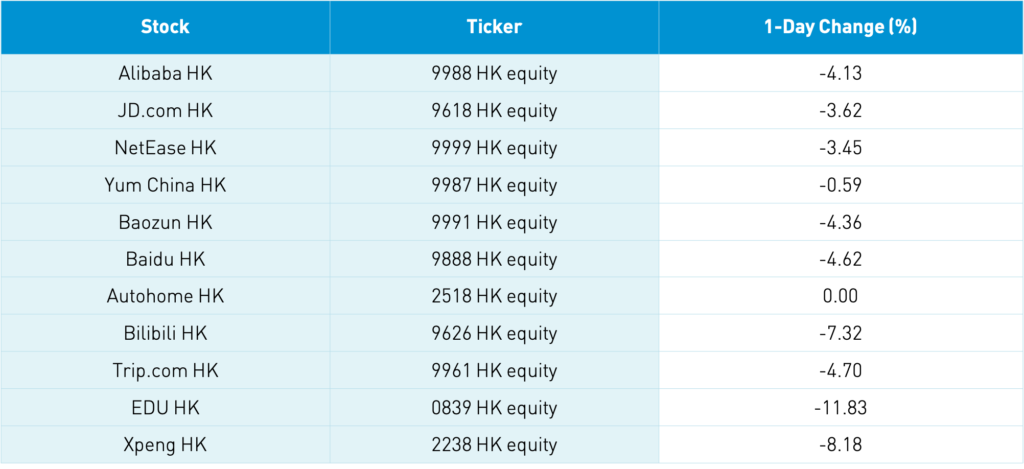

Hong Kong was dragged lower by internet stocks, especially by tutoring/education stocks. Tutoring is one area where regulation may affect the financials of the companies due to limits on how much time kids can spend on tutoring. However, the regulation will not affect the behavior of parents who want their kids to study for China’s rigorous school exams. The two big players in the space, TAL Education and New Oriental Education, were off -72% and -62%, respectively, year-to-date.

Overnight, several internet companies were fined $77,000 each for past mergers and acquisitions. The fine is hardly a death sentence! Investors appear to be stringing several events into one narrative though they are not directly related. Yes, regulation is occurring, but it has had no effect on Q4 2020 or Q1 2021 earnings. The companies adhere to the rules and move on. Yes, Didi’s IPO was a huge disappointment as its regulatory review was announced only two days following its IPO, which required suspending new users from signing on. Didi’s IPO prospectus included sixty pages of risk factors. Sixty! At the same time, it is still operating in China. Regulators will scrutinize offshore listings going forward, but I don’t see it as the end of US listings as US private equity firms, which back a whole host of private Chinese startups, will want to cash out in dollars.

Finally, we have the Holding Foreign Companies Accountable Act that addresses the long-standing issue of PCAOB auditing the audit books, which is a resolvable issue if there is dialogue/communication. US-listed Chinese companies are audited by the Big Four accounting firms who do the audits of the US companies’ China operations. Attached is a chart of the shares outstanding in a Mainland-listed Chinese ETF that invests in US and Hong Kong-listed Chinese internet stocks.

Despite the ETF losing -18% year to date, investors in China are investing heavily as indicated by the shares outstanding increasing from 2mm shares to 10mm year-to-date. Why? Because these companies are great companies and critical to China’s domestic consumption economy. I wish I could predict when this slide will end. At the same time, this move looks like investors are banking on the worst of every conceivable outcome.

H-Share Update

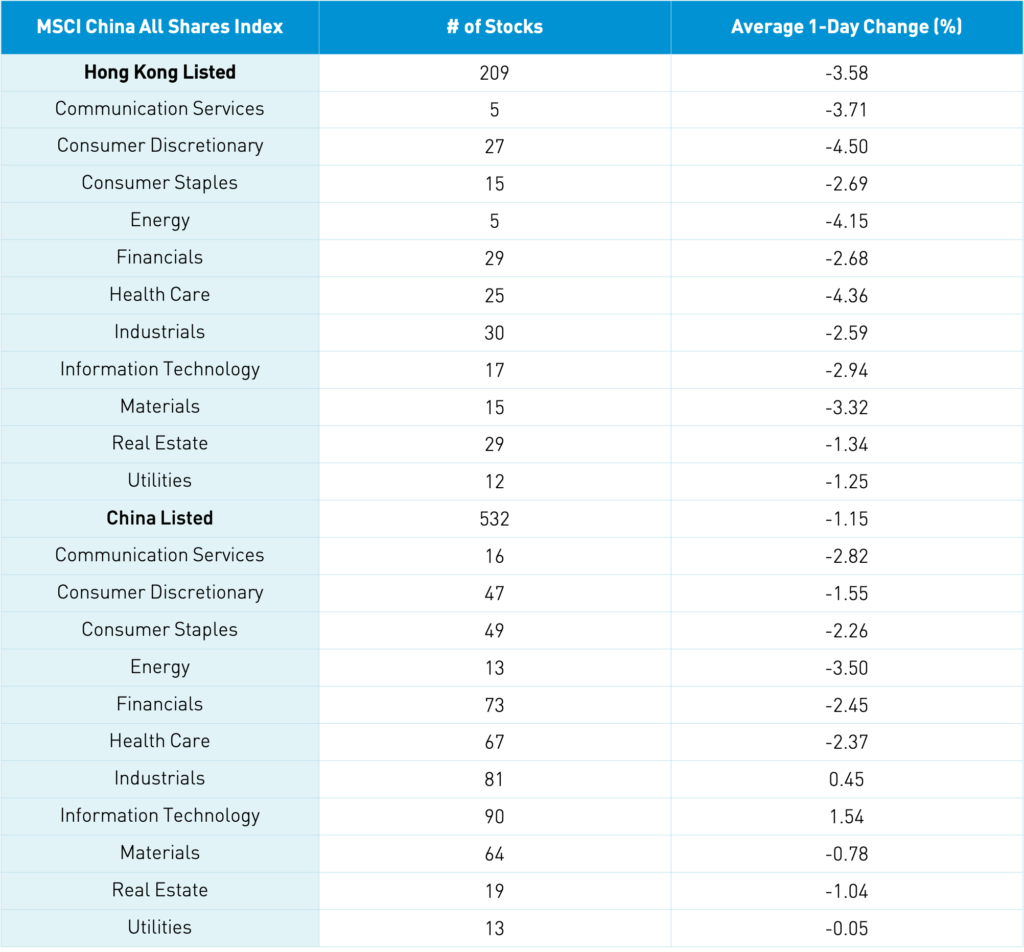

The Hang Seng Index and Hang Seng TECH Index declined -2.89% and -3.71% respectively as volume spiked +31% from yesterday, which is 125% of the 1-year average. The 209 Chinese companies listed in Hong Kong within the MSCI China All Shares declined -3.58%, led lower by discretionary -4.5%, health care -4.36%, energy -4.15%, communication -3.71%, materials -3.32%, tech -2.94%, and staples -2.69%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -3.74%, Meituan, which fell -6.43%, Alibaba HK, which fell -4.13%, HK Exchanges, which fell -0.2%, Xiaomi, which fell -1.17%, Ping An, which fell -4.34%, Keymed Biosciences’ IPO, which rose +27.58%, BYD, which fell -2.4%, Geely Auto, which rose +0.42%, and Wuxi Biologics, which fell -4.83%. Southbound Stock Connect volumes were elevated at nearly 2X the average as Mainland investors sold a healthy $521mm of Hong Kong stocks as Southbound trading accounted for 15.8% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +0.66%, +1.68%, and +2.43% respectively as turnover declined -6% from yesterday, though still 112% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares gained +1.31%, led by industrials +3.24%, healthcare +2.63%, tech +2.18%, materials +1.83%, and discretionary +1.08%, while energy fell -1.63% and real estate -1.02%. The Mainland’s most heavily traded were Long Green Energy, which rose +8.59%, BYD, which rose +1.83%, China Three Gorges Renewables, which fell -0.62%, CATL, which rose +5.29%, COSCO Shipping, which rose +5.37%, China Northern Rare Earth, which rose +7.67%, Eve Energy, which rose +13.3%, Tianqi Lithium, which rose +1.02%, broker East Money, which rose +1.43%, and Ganfeng Lithium, which rose +4.65%. Northbound Stock Connect volumes moderate as foreign investors bought +$676mm of Mainland stocks as Northbound Connect trading accounted for 5.7% of Mainland turnover. CNY and bonds rallied while copper was off.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.49 versus 6.47 yesterday

- CNY/EUR 7.70 versus 7.64 yesterday

- Yield on 1-Day Government Bond 1.63% versus 1.71% yesterday

- Yield on 10-Year Government Bond 2.98% versus 3.06% yesterday

- Yield on 10-Year China Development Bank Bond 3.39% versus 3.46% yesterday

- Copper Price +0.48% overnight